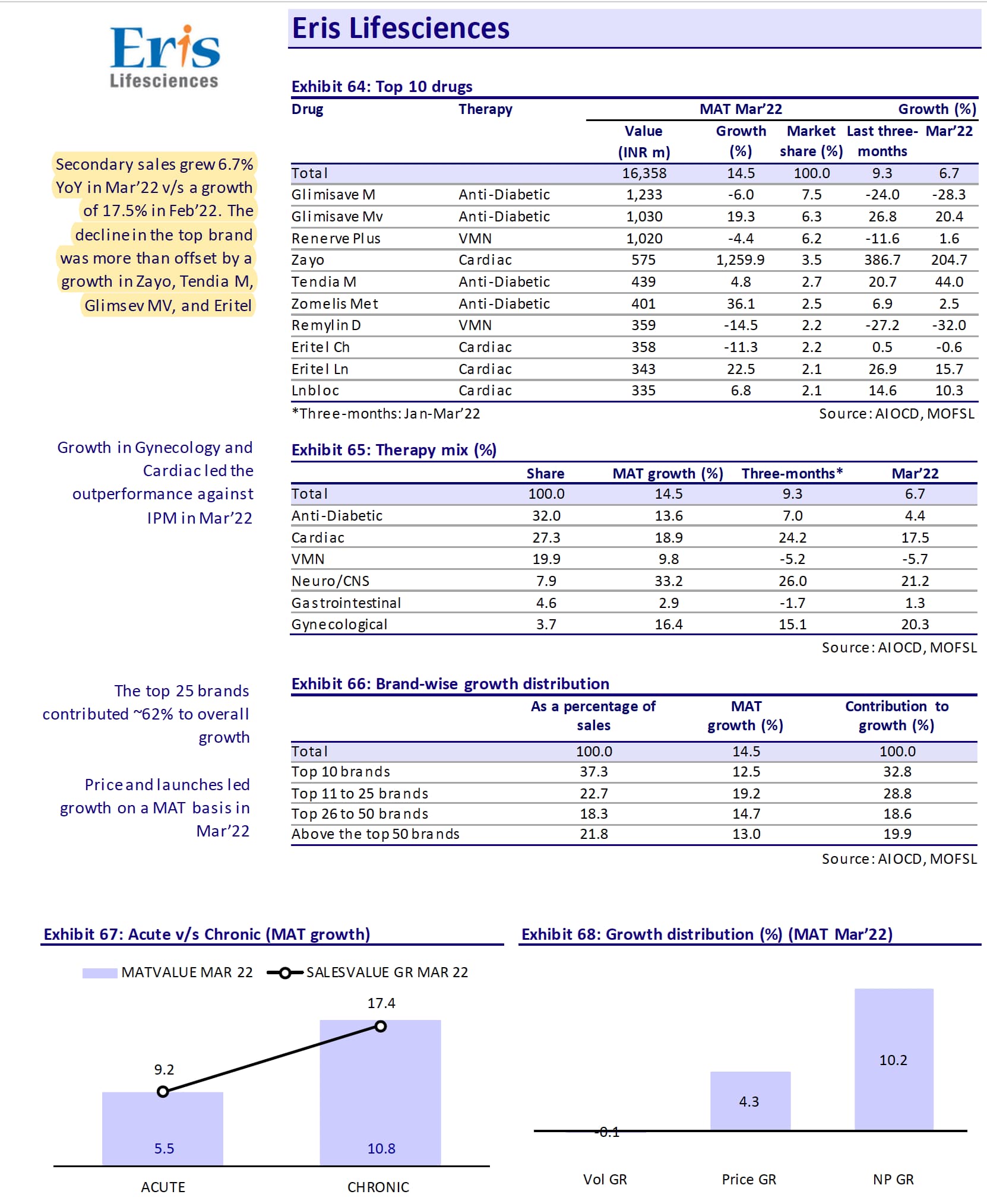

I think results were reasonable, Q4 is always a low base quarter so QoQ comparison will give an incorrect picture. On a YoY basis, company grew around 9-10% which is higher than IPM growth. If we look at IPM data, there has been volume de-growth at an industry level whereas Eris has managed to maintain its volumes. The recent insulin launch will reflect in FY23 numbers, lets see how it goes.

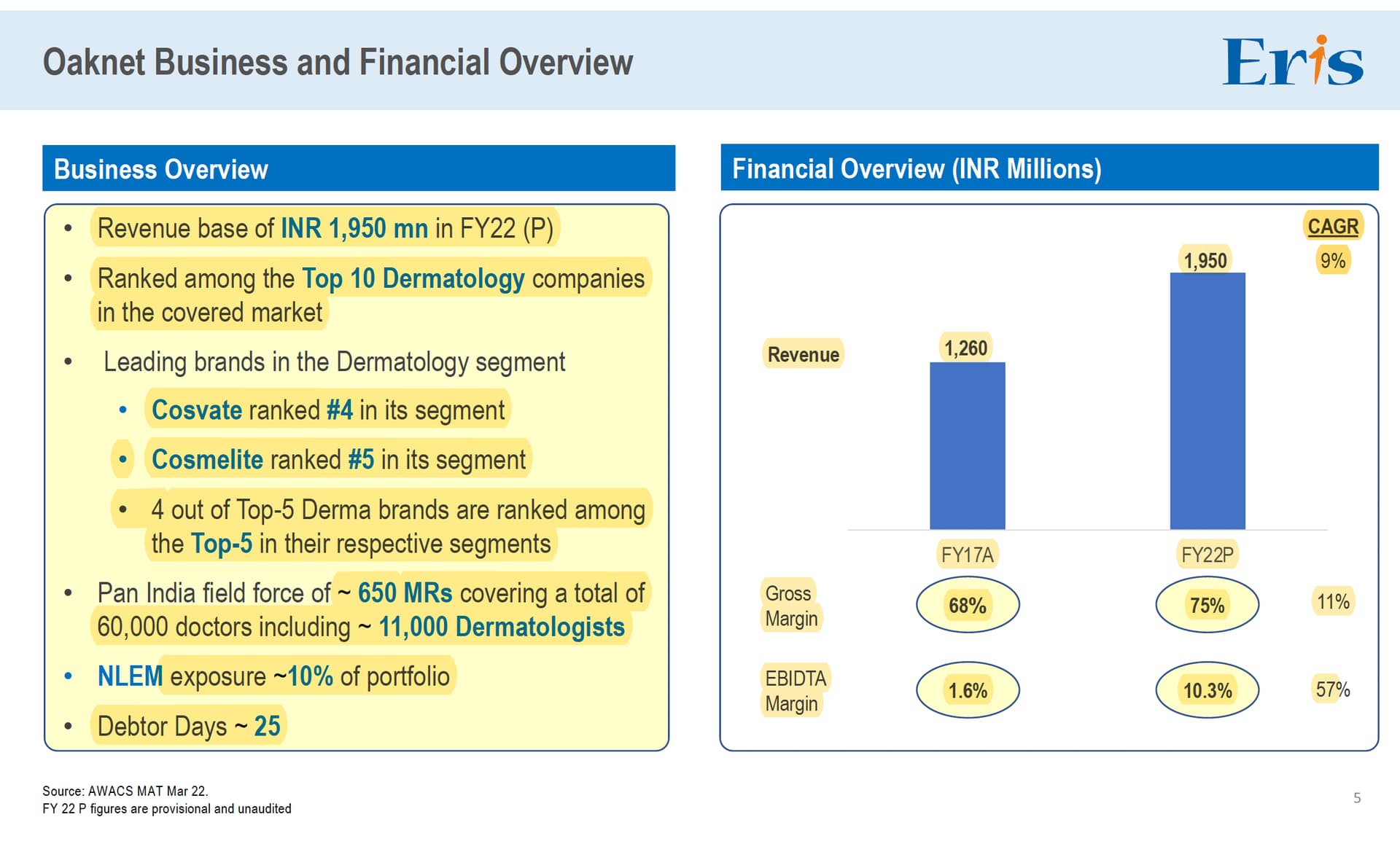

Today’s acquisition of Oaknet is also very interesting, it gives Eris an entry in Dermatology segment. Oaknet is supposed to do sales of 195 cr. in FY22 with gross margins of 75% and Eris paid 650 cr. for this (~3.33x sales). This is probably close to a fair price (or maybe a bit undervalued), specialty brands generally sell at 4-6x sales in private markets. I think Eris will rationalize the MR strength (or make them sell more products), you generally don’t need 650 MRs for maintaining sales of 200 cr.

Disclosure: Invested (position size here, bought few shares in last-30 days)