Data from the investor presentation. Good stuff:

- Cost of funds further down to 6.20%.

- Casa at 52%. Also retail % of term desposit

- CRAR at 25.16%. So much room to grow and increase the RoE which is at 12.2%.

- Slight reduction in GNPA to 4.06%. Net provisioning remains almost the same.

- High disbursement rate. Increase of 15% QoQ, 29% YoY. This results in 4.6% increase in QoQ gross advances.

- Opex isn’t increasing. Note that the decline from 240 to 209 cr is due to reversal of excess grauity and leave salary in this quarter.

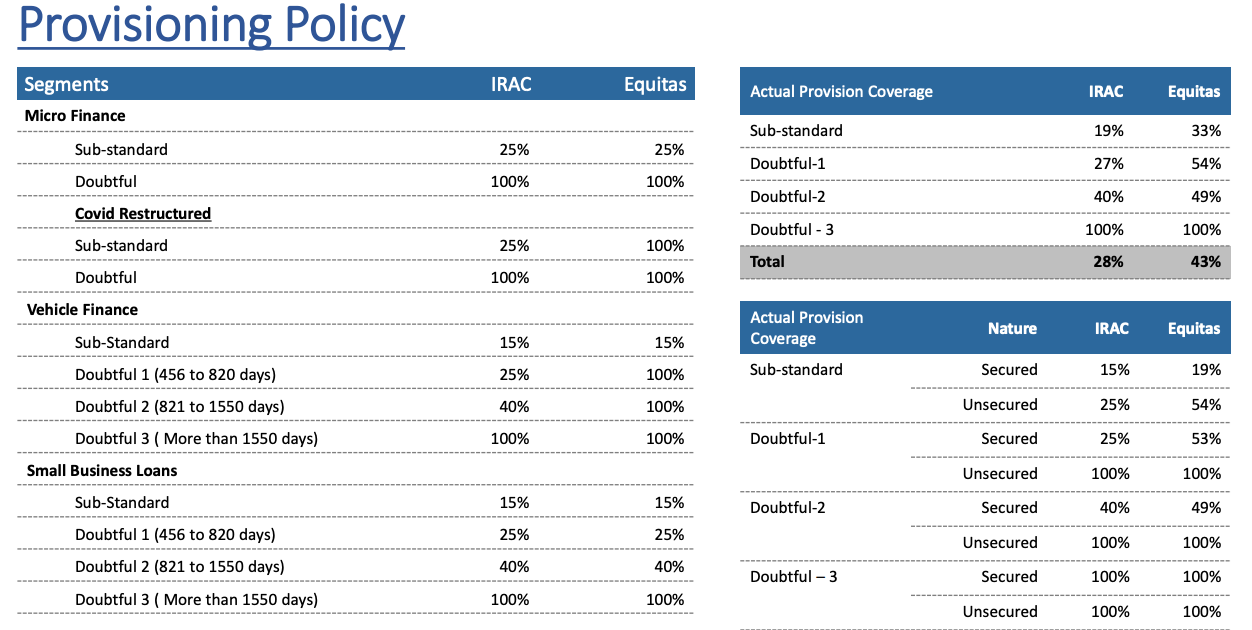

Bad stuff: Provisioning and writeoffs are worrysome:

- Writeoff of 191 cr in this quarter which is ~1 % of gross loans.

- Addition of 408cr NPA, highest for FY22. Although this was expected due to the restructuring 2.0

- Continuously declining PCR at 42.73% now (46.81% last quarter.

Though a lower PCR can be somewhat justified by the fact that Equitas has > 80% of assets secured. And Their provisioning against unsecured loan is higher than what this lone number represents.

Sub standard unsecured loans are 54% provisioned.

I do have questions on how much writeoff is actually a loss to the bank, since we have secured loans. How much is the bank able to recover as a % of the advance?

disc: invested