Engineers India Ltd.: Please find below my research on EIL. I don't have answers for some of the questions that I am jotting down in the end. It will be great if people can help me answer them:

Engineers India Limited provides engineering and related technical services for petroleum refineries and other industrial projects primarily in India. Its fields of activities include petroleum refineries, pipeline, oil and gas processing, petrochemicals, offshore structures and platforms, ports and terminals, metallurgy, fertilizers, power, highways and bridges, airports, non conventional/renewable energy sources, and intelligent buildings and urban development. The company offers various services to conceptualize, design, engineer, and construct projects to meet the specific requirements of its clients. It has strategic alliances with VAI Industries UK Limited; Deutsche Montan Technologies GmbH; Curtin University of Technology; IOCL; Petron Scientech, Inc.; Stroytransgaz; GAIL India Limited; and Jacobs Engg Co. The company was founded in 1965 and is headquartered in New Delhi, India with additional offices in London, the United Kingdom; Abu Dhabi, the United Arab Emirates; and Kuwait, Qatar, Malaysia, and Australia.

EIL executes projects either on a Lump Sum Turn Key (LSTK) or consultancy basis. Petroleum refining sector plays a dominant role in the company's business. EIL, with a strength of more than 3,000 qualified engineers, is regarded to be the best such company in Asia, besides those in Japan. It has developed indigenous capability in all aspects of the oil industry.EIL has to its credit, over 400 major projects successfully completed and has grown over the years to become a unique organization, the likes of which has not been created in any other developing country.Firm has no debt and generates copious amounts of cash flow. Company has solid, clean balance sheet. Cash makes up for Rs. 2000 Cr. approximately on a total assets size of approx. Rs. 3000 Cr. It is looking to grow internationally (mostly in middle east countries) and enter into new sectors like Nuclear, Water, Solar Power and Coal To Liquid. Government of India has 90% stake in the business. Management has lot of depth with long tenure in the company. Company has diversified customer base and next to nothing capital expenditure requirements.

I am not a big fan of government run organizations but EIL is a special case. EIL, in my opinion truly reflects capabilities of Indian engineers. The company has been profitable consistently and it will be difficult for other engineering consulting competitors to duplicate it's cost structure and capabilities. EIL is involved in all kinds of infrastructure projects being commissioned in India. Government of India is also planning to divest another 10-15% of its shares in the company. This action would increase the float of the company and make it easier for bigger players to buy a stake in the company.

Valuation: Free Cash Flow/Total Enterprise Value yield works out to a juicy 15%.

Here is other financial info:

Price

1,146.50

Market Cap (mm)

64,387.40

Shares Out. (mm)

56.2

Float %

9.20%

Dividend Yield %

1.60%

EPS

62.53

P/E

18.63x

Total Revenue (mm)

15,514.50

TEV/Total Revenue

2.9x

Price/Tang BV

4.7x

Net Income(mm)

3,511.50

Cash & ST Invst.(mm)

20,614.70

Market Capitalization(mm)

65,440.40

Total Debt

0

Total Enterprise Value(mm)

44,825.80

Total Assets

30,255.50

Capital Expenditure(mm)

-219.6

P/Diluted EPS Before Extra

18.6x

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Revenue (mm)

6,947.1

8,594.7

5,467.4

8,592.8

12,871.6

9,252.9

8,060.0

5,818.4

7,376.8

15,514.5

Net Income (mm)

1,252.5

1,271.7

247.1

641.6

822.5

1,180.2

1,428.2

1,451.3

1,980.2

3,511.5

Margin %

18.0%

14.8%

4.5%

7.5%

6.4%

12.8%

17.7%

24.9%

26.8%

22.6%

EPS

4.4

11.43

14.646

21.017

25.433

25.844

35.263

62.53

12 months Mar-31-2003

12 months Mar-31-2004

12 months Mar-31-2005

12 months Mar-31-2006

12 months Mar-31-2007

12 months Mar-31-2008

12 months Mar-31-2009

Return on Assets %

8.4%

5.2%

7.8%

6.3%

5.8%

5.8%

9.2%

Return on Equity %

8.8%

10.6%

14.0%

15.4%

14.3%

17.7%

27.1%

Question:

What is EIL going to do with all the cash sitting on the Balance Sheet?

Where do I find out how much order backlog the company has?

Company doubled its revenue base between 2008 and 2009 fiscal year. Is it sustainable? Also, the increase in revenue base came from LSTK projects which happen to have lower margins. Is that trend going to continue in the future? Right now LSTK projects make up about 46% of the revenue and the rest comes from Consultancy. Consultancy assignments carry higher proft margins of about 30% while LSTK profit margins are much lower. LSTK profit margins range anywhere from 1% to 12%

Who are EIL's competitors? I don't see any publicly listed company at least in mid-cap space.

What is it that EIL does better than its competitors?

EIL recently bagged last month 2 huge orders from BPCL Kochin & Mumbai which will keep them busy for next 2-3 years.This means the biggest concern of EIL has been taken care.

now is the company ripe for picking at this level?

I have started buying EIL for the first time earlier this week. I have known the company for more than 3 decades. I attempt to answer some of the questions you raised:

What is EIL going to do with all the cash sitting on the Balance Sheet?

It is a government enterprise. I all likely hood it would end up there.

Who are EIL’s competitors?

L&T is the single biggest competition I could imagine for LSTK project as well as consulting. There other niche players in consulting like Lurgi, Bechtel, Doosan, Punj lloydamong others.( But most of them are probably not being traded publicly in India. )

What is it that EIL does better than its competitors?

EIL benefits from being a government enterprise in my view. They get projects from every refinery projects by the state-run companies, they also do consulting for other India friendly goverments in developing world. I know they had projects executed in Iran, Algeria and others.

Isnt EIL which came with a FPO at a rock bottom price of 144 almost at a 4 year low a prime pick for buying at cmp of 152 due to FPO overhang which is finally getting clear.Also

On an Expected EPS of 16 rs for FY 14 PE of 9 odd becomes very attractive .The main factor that has attracted analyst to this counter is the cheap valuation. The company is now trading at nine times its consensus forward earnings, significantly lower than its 3-year average. With the improvement in growth, a re-rating is expected, which promises handsome returns to the long-term investors. The downsideriskto this counter is limited from current levels because the company has extremely strong fundamentals.

Due to its asset-light business model, low capital requirement, high operating margin and negative working capital,

Engineers India’s return on equity is above 30 per cent. The returns ratios are expected to remain at elevated levels because 54 per cent of its current order book is from the high-margin consultancy segment. It is a debt-free company and also boasts Rs 2,600 crore cash balance, which is about 50 per cent of its current market cap. The management is following a liberal dividend payout policy and this is expected to continue in the future.

Cash equivalent of almost rs 74 on books.

Excellent div yield including interim dividend of rs 3 expected to be announced in march 14 like in last year.

4)The company’s effort to increase its international presence is also yielding fruit: 28 per cent of the orders were from international clients as on 31 December, compared with just 7 per cent as on 31 March 2013. While easing tensions in the Middle East area have helped get more orders, the weakening rupee is helping the company with better export realisations.

5)Due to flipping by IPO applicant the price may fall down further making it more attractive?

No wonder different research houses like Ambit,IndiaNivesh,Religare & Quant broking has given a price target ranging from 160- 209.

Views Invited.

Discl- Have been allotted shares in the recent FPO.

This is my first reply on the board.

I have been tracking EIL for last 2 years and looks like the financials have been improving. Moreover oil prices have bottomed out amid the squabble in OPEC and there is considerable interest in new exploration activities inside India and in near vicinity. I have an optimistic view on the stock from a long term ( 3-5 yrs).

I am looking for view from others who have been tracking the company and have an opinion on the sector or stock and how the growth prospects might look like.

Disclosure: Had initiated exposure to the scrip for tracking purpose 1 year ago and thinking of increasing it

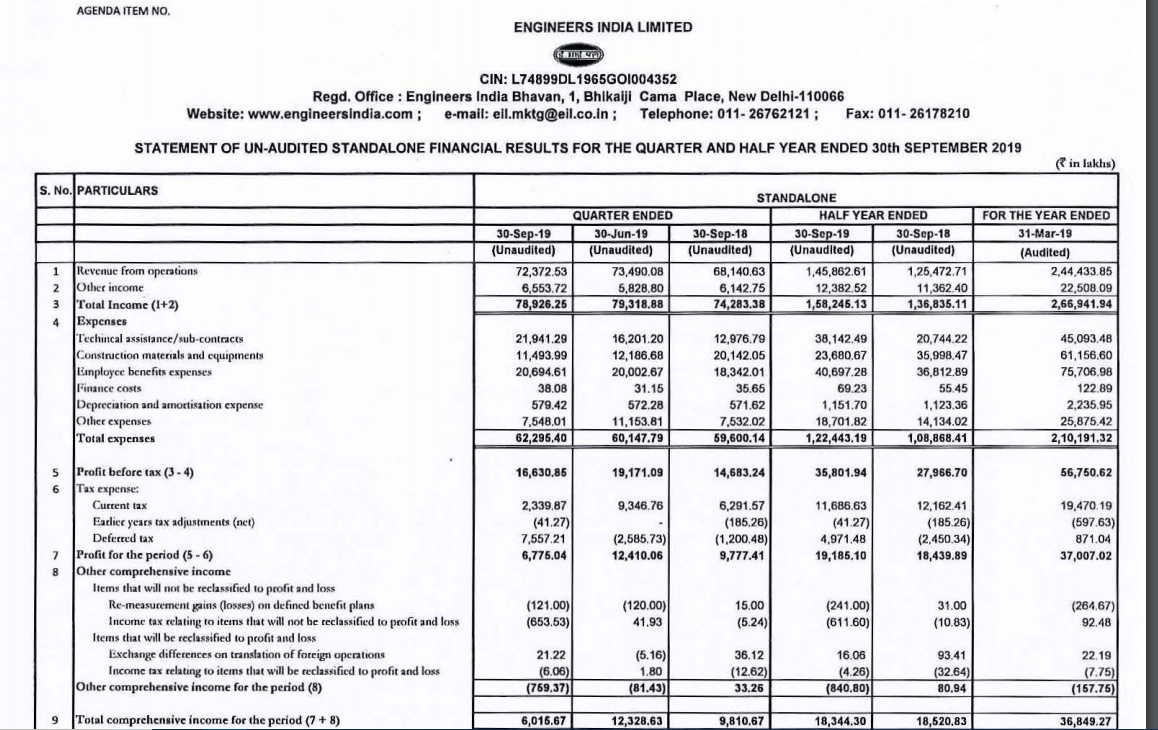

Hi All, Was wondering if any of you could throw some light on the deferred tax of 75Cr which the firm paid in this quarter? The operational performance seems good with profit before tax increasing by more than 13% Why was this deferred tax expense created in the P&L for this quarter?

The dividend yeild is too juicy at this moment. What is Mr Market pricing in for such consistent roce players? What are the key metrics to track for this company ?

Can someone shed more light on Engineers India’s Numaligarh refinery bid?

I understand Engineers India and Oil India consortium has bid for over 48% stake in Numaligarh which I believe is worth approximately 5500 crores.

Engineers India takes minority position.

My questions

Minority position is what percentage? Did Engineers India management shed any light on this.

Numaligarh refinery financials?

Engineers India can mostly fund this bid from internal cash reserve.

Also the recent buyback extinguished 10-11% of outstanding shares. Should help to offset the “non-core stakes” concerns raised by financial ratios focused analysts.

NRL will be a key customer for next few quarters and it helps to have a stake to keep getting business I think… The geographical location of NRL is a bit of concern though.

Personally, I think they should not invest more than 1500 cr out of the 2800 cr internal reserves - which makes it about an 8% stake in NRL. But let’s see how it works out in practice.

It’s not really a great decision to invest - running a refinery has nothing to do with their business. Clearly appears to be a case of the government asking them to pitch in. The only thing is given it’s a refinery that is profitable and seemingly well-run, and with EIL’s stated desire to consider this as no more than a financial investment, it may work out alright. If NRL’s numbers are right and don’t deteriorate, it’s good dividend yield for EIL’s minority stake. It’s also probably better than being forced by the government to use the reserves for something else.

So EIL will spend 500 cr for a 4.37% additional stake which is not a bad outcome at all. (Per ET article behind paywall). Seems there is no communication to exchange yet so there is a chance this might change.

Pretty solid result overall. However all that is impacted by one provisional item.

There appears to be one big hit that company has taken of INR 154.96 crores.

This is the exact statement.

"The employee benefit of PF is administered through a separate Ell Employees Provident Fund Trust. Out of the investments made by PF Trust in the past, some

issuers of securities have defaulted in interest payments and I or principal repayments. The amortised value of probable future principal defaults is i1’ 19,370.59

Lakhs as at 31 March 2021. Considering the Employers obligation to make good the loss in value of these investments under the Provident Fund regulations, the

Company has provided in its books of account 80% of the amortised value (of probable future principal defaults) amounting to i1’ 15,496.48 Lakhs in the current year

and charged to consolidated statement of Profit & Loss.

The above has been disclosed as Exceptional item in the consolidated statement of Profit & Loss of the Company. "

Yes pls. Senior boarders pls help understand this.

Govt is crying that it has been robbed? Is all sunk now or there must be legal recourse to get it back albeit with a lag?