Have you seen their presentations of executed projects? They have lots of repeat business in OIL & Gas sector from E&C to maintenance and expansions. They may not know HOW to run it financially but technically, they do know. EIL managing their own commissioned refinery parts is not an issue but do they know how to manage finances?

Of course they do.

The board must have thought, we commission these kind of units every year, we might as well own a bit of the profits that come to the owner of the installed asset. As posters have mentioned above, it’s not a bad move technically but definitely will lock up manpower in managing these assets IF they decide to do the Operate part of refinery biz

Fair points. But I was speaking of “Operating” the business only. They don’t plan to do it is what I gathered from their announcements and I hope that’s so.

Management expects margin to normalise over the coming quarters with pick up in consultancy revenue, led by pick up in order inflow.

EIL will be a beneficiary of sun-rising opportunities like coal gasification and green hydrogen backed by a strong order pipeline stemming from the expected investments in the hydrocarbon industry.

For FY23, management has guided for 15% revenue growth with 45% coming from consultancy. Standalone PAT target is Rs. 350 crores. Order intake of 40000 crores is expected in FY23.

Order intake for Q2 was 340 crores and total for H1 FY23 is 800 crores. Its targeting an order intake of 50000 crores each in FY24 & FY25.

Company is targeting to increase its exposure in the Middle East and Saudi Arabia.

Company is working on multiple new opportunities in green energy: i) Green hydrogen, where it is operating two projects that are in advanced stages; ii) coal to methanol; iii) emission control technology for steel majors; iv) emission control technologies to help oil & gas companies achieve their net zero targets

Margins are lower in consultancy business. Higher revenue share from turnkey business. EBITDA margins contracted overall.

-

Management expects margins to normalize. Consultancy revenue is expected to increase along with order inflow where a segment profit of 25% is expected which is currently 20%.

-

They will benefit from opportunities like Coal Gasification, Green Hydrogen backed by strong order pipeline from hydrocarbon industry.

-

Orders worth 1275 crores are in the finalization stage and orders should be received in Q4 FY23. Company has maintained its guidance of order intake of 4000 crores.

-

Company is currently working on feasibility projects across multiple hydrocarbon fuels, pipeline and renewable fuels and biofuels. As the capex cycle picks up across industries, they will benefit. Need to keep a check on order intake outlook and balance sheet which is necessary to be kept cash rich.

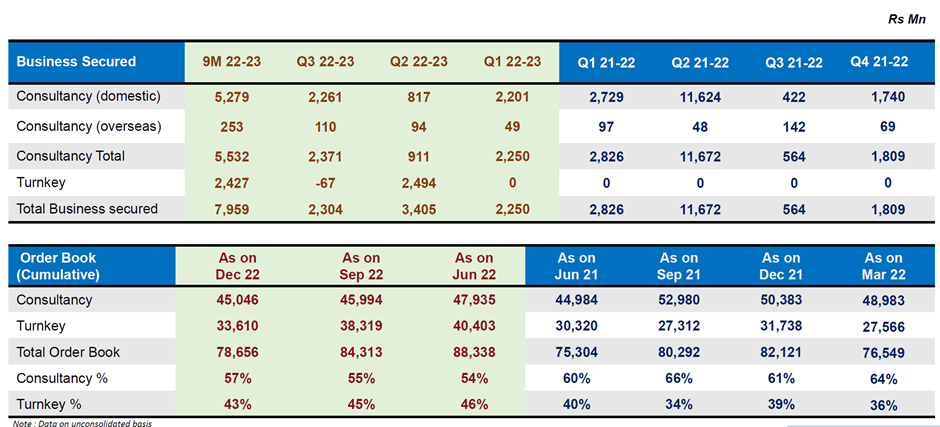

Total Order Book stands at 9079 crores as of 31st March, 2023. 83% of the orders are domestics where as others are overseas. Mix of order inflow expected to be 50% consultancy and 50% turnkey. The company expects to maintain the guidance of INR4,000 crores to INR5,000 crores of order inflow in '23 and going ahead.

There is huge opportunity in Natural Gas Pipeline Sector. The company wants to foray into renewables and nuclear power. EIL is targeting the petrochemical complex sector and has already moved into sectors like green hydrogen, bioethanol, biofuels, coal gasification, and fertilizer.

Company targeting niche projects in institutional buildings, data centers, airports, and bullet train project in the infrastructure segment.

The company is focusing on international markets and has strengthened its Middle East office. EIL is targeting African countries for projects in LNG, fertilizer, and oil and gas. The company is shifting its focus from being a purely domestic company to overseas companies and is also focusing on infrastructure projects.

The company aims to maintain a range of 27-30% margin for consultancy and 4% margin for EPC.

Introduction (00:01): The call, hosted by Dam Capital Advisors Limited, begins with a welcome message and a reminder that participants will have a chance to ask questions after the presentation.

Introduction of EIL Management (00:35): Ms. Buika N introduces the EIL management team, including Mr. Sanjay Jindal (Director of Finance), Mr. Sendu P (Company Secretary and IR), Mr. RP Batra (Executive Director, Finance and Accounts and IR), Mr. Sun Saka (Executive Director Technical and IR), Mr. Aman Singh Chopra (Senior General Manager, CMD Office and IR), Mr. Viv Maida (General Manager, Marketing BD and IR), and Miss Niha Narula (Senior Manager, Company Secretariate).

Opening Remarks by Mr. Jindal (01:13): Mr. Jindal provides an overview of the financial results for Q2 and the first half of FY 2324, noting a turnover of INR 777 crore for Q2 and INR 1,586 crore for the half-year. He details segment-wise turnover and highlights an increase in profit before tax (PBT) and profit after tax (PAT), with a notable improvement in EPS.

Order Book Status (03:37): Mr. Jindal mentions the company’s order book value of INR 8,188 crore, divided between the consultancy segment and the turnkey segment.

Q&A Session Announcement (04:28): The floor is opened for a Q&A session, with instructions for participants on how to ask questions.

Question on Financial Adjustments (05:17): An analyst asks about adjustments related to liquidity damage settlement, leading to a discussion on margins and revenue adjustments. Mr. Jindal clarifies the impact of a 45 crore adjustment on turnover and profit.

Discussion on Turnkey Segment Margins (05:55): The conversation shifts to margins in the turnkey segment, with explanations on quarter-to-quarter variations and long-term margin expectations.

Pipeline and Future Prospects (07:07): The management discusses future business prospects, including ongoing bids in various sectors like oil and gas, petrochemicals, and infrastructure.

Consulting Margins (08:20): An inquiry about consulting margins leads to a discussion on quarterly variations and expected change orders.

International Initiatives (10:51): The management talks about increasing international initiatives, mentioning projects in Algeria, Nigeria, South America, and the UAE.

Non-Oil and Gas Initiatives (12:34): Discussion on diversification into non-oil and gas sectors, focusing on decarbonization projects, including green hydrogen.

Investments in Fertilizer and Refinery Projects (20:32): The call covers EIL’s investments in fertilizer and refinery projects, discussing returns and related work orders.

Future Investment Plans (21:08): There’s a discussion about future investment plans, particularly in the context of the NRL expansion.

Ordering Activity in International Markets (32:34): The management speaks about international business, order sizes, and the nature of these orders.

Strategic Alliances (37:14): The call touches upon strategic alliances, particularly with Sunrise Group of Australia, and their role in emerging technologies like solar concentration.

Opportunities in Decarbonization and Defense (39:02): The conversation shifts to opportunities in decarbonization, green initiatives, and the defense sector.

Expectations for FY 25 (41:38): The management discusses expectations for FY 25, focusing on the cyclical nature of the business and project-oriented strategies.

Coal Gasification Projects (43:03): There’s a discussion about coal gasification projects and collaborations with companies like Coal India and NLC.

Closing Remarks (47:44): The call concludes with closing remarks and a thank you to the participants and the management team.

What I learned after reading the Engineers India Q1FY25 Earnings Call

This is a positive development. It shows that the company’s order book is robust and growing rapidly. The fact that these orders are in the LSTK and OBE segments suggests that Engineers India is expanding its service offerings and tapping into new growth areas.

The Middle East is a competitive market. Engineers India needs to maintain its competitive edge to continue winning projects in this region. This region could become a major revenue hub for the company.

The Indian government is heavily promoting green hydrogen, and Engineers India seems to be aligning its strategy with the national agenda. This could lead to potential government support and incentives.

In Engineers India, 8300 cr mcap, and cash is 1134 cr, company generating annual PAT approx 400 cr and sitting on a robust order book 11300 cr order book with 46% consultancy which fetch better margins. Can it be a value buy?