1 Like

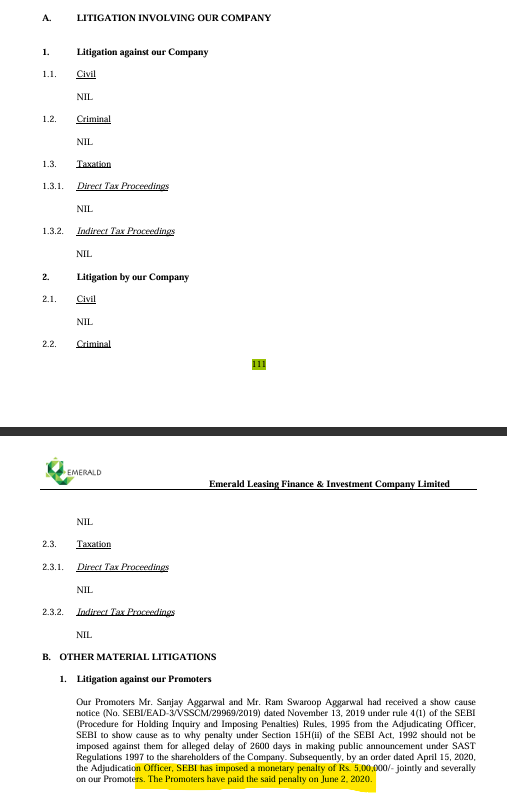

Went through the whole thing. Seems like 5-6 years ago they didn’t have proper systems in place to track their own disclosure requirements, and hence it was delayed by 7 years!! Other than that the penalty quantum is at the absolute floor of the SEBI penalty matrix for Section 15H that section can attract penalties up to ₹25 crore or 3x profit. The AO opted for ₹5 lakh, maybe the adjudicator viewed it as procedural and not deserving of meaningful punishment. It was paid promptly (within ~7 weeks of the order), disclosed transparently in the 2021 LoO, and there’s nothing about wilful default. Hundreds of similar SAST disclosure-delay penalties get issued every year against small and mid-cap promoters across India.. it’s actually one of the most common categories of SEBI adjudication. From the dataset I’m aware of, this would not be flagged as a “red item” in most institutional PE legal DD reports; it would land in “noted items, no material concern” with a one-line explanation.

6 Likes

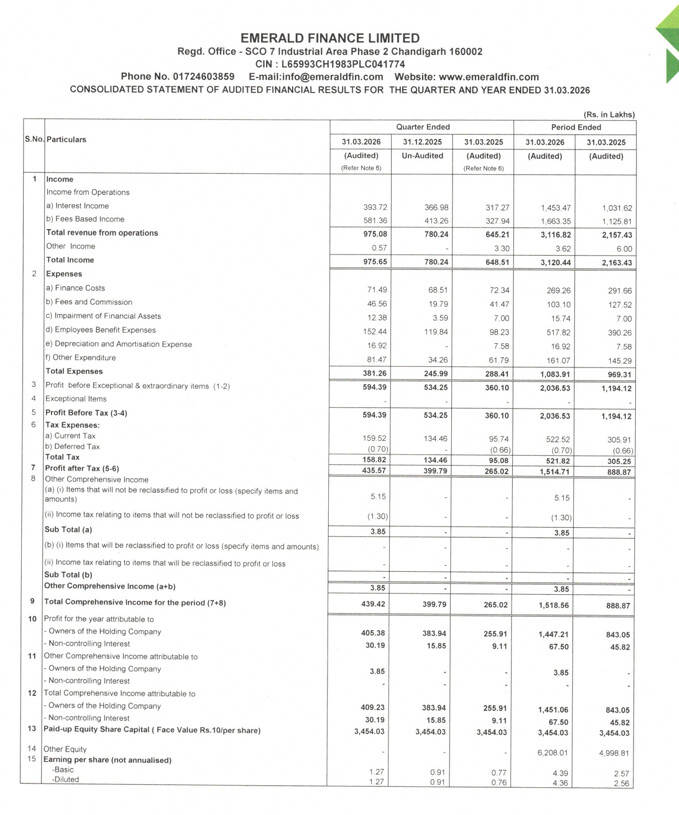

Results are out, revenue for Q4 is 9.75 Cr (+51.13% YoY & +24.97% QoQ). Interest based income is up around 9% and fee-based income is up around 30% (QoQ)! Repeat customers I believe played a big role.

Employee benefits and fees/commissions increased quite a bit as well, most likely its Q4 thing as seen in previous years. Bottom line growth figure 4.05 Cr (+58.41% YoY & +5.58% QoQ).

TTM EPS now stands at 4.39 making the current PE 14.5 from 16.1

QoQ table

| Quarter | Sales (₹ Cr) | Absolute Increase (₹ Cr) | QoQ Growth (%) |

|---|---|---|---|

| Jun ’22 | 2.21 | — | — |

| Sep ’22 | 2.39 | +0.18 | +8.14% |

| Dec ’22 | 3.05 | +0.66 | +27.62% |

| Mar ’23 | 3.87 | +0.82 | +26.89% |

| Jun ’23 | 2.78 | −1.09 | −28.17% |

| Sep ’23 | 3.24 | +0.46 | +16.55% |

| Dec ’23 | 3.42 | +0.18 | +5.56% |

| Mar ’24 | 3.89 | +0.47 | +13.74% |

| Jun ’24 | 4.39 | +0.50 | +12.85% |

| Sep ’24 | 5.00 | +0.61 | +13.90% |

| Dec ’24 | 5.72 | +0.72 | +14.40% |

| Mar ’25 | 6.45 | +0.73 | +12.76% |

| Jun ’25 | 6.71 | +0.26 | +4.03% |

| Sep ’25 | 6.90 | +0.19 | +2.83% |

| Dec '25 | 7.80 | +0.90 | +13.04% |

| Mar ’26 | 9.75 | +1.95 | +24.97% |

5 Likes

why is that specific to Q4? hoe do you interpret this? would love to hear thoughts.

I think it’s more financial year ending thing so they might be giving yearly bonuses and settling fees for their collection team and other non-permanent staff. I might be totally wrong though; we will know details soon enough from the concall (1st june 4pm)

1 Like

All sort of expenses rose actually. Thinking about a few abnormal ones like impairment of FA (what exactly does that mean?), D&A (why was it 0 in Dec, which is a bit weird), other expenditures also increased quite sharply! Other than that everything is easily explainable.

2 Likes

Got little bit surprised to see management is not giving gnpa and nnpa data in presentation.

Thereafter I read concall in which one of the retail investor asked this rigorously that last time also you agreed to give data but unfortunately you haven’t given. This seems to be red flag for me.

loans gone bad is impairement of FA