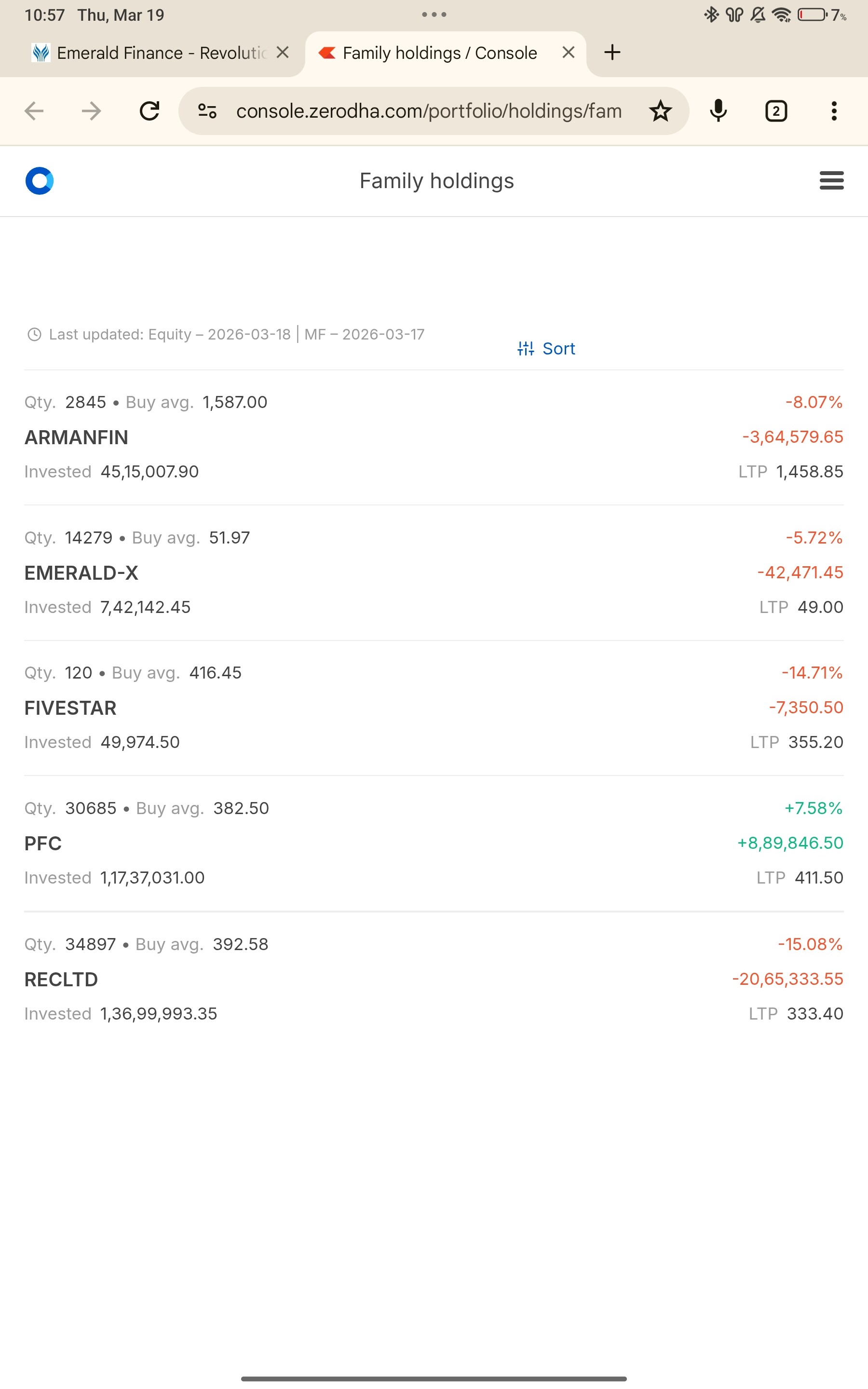

Almost half of the day’s trading volume happened in the last 30 mins, when I looked at the 5 Min chart. I knew there were high chances the promoters must have bought it from the market (looking at the price movements as well).

Basically, I was right. Yet another promoter acquisition. Since Feb till now they have increased their stake by ~0.2% (65000+ shares)

Great sign!!

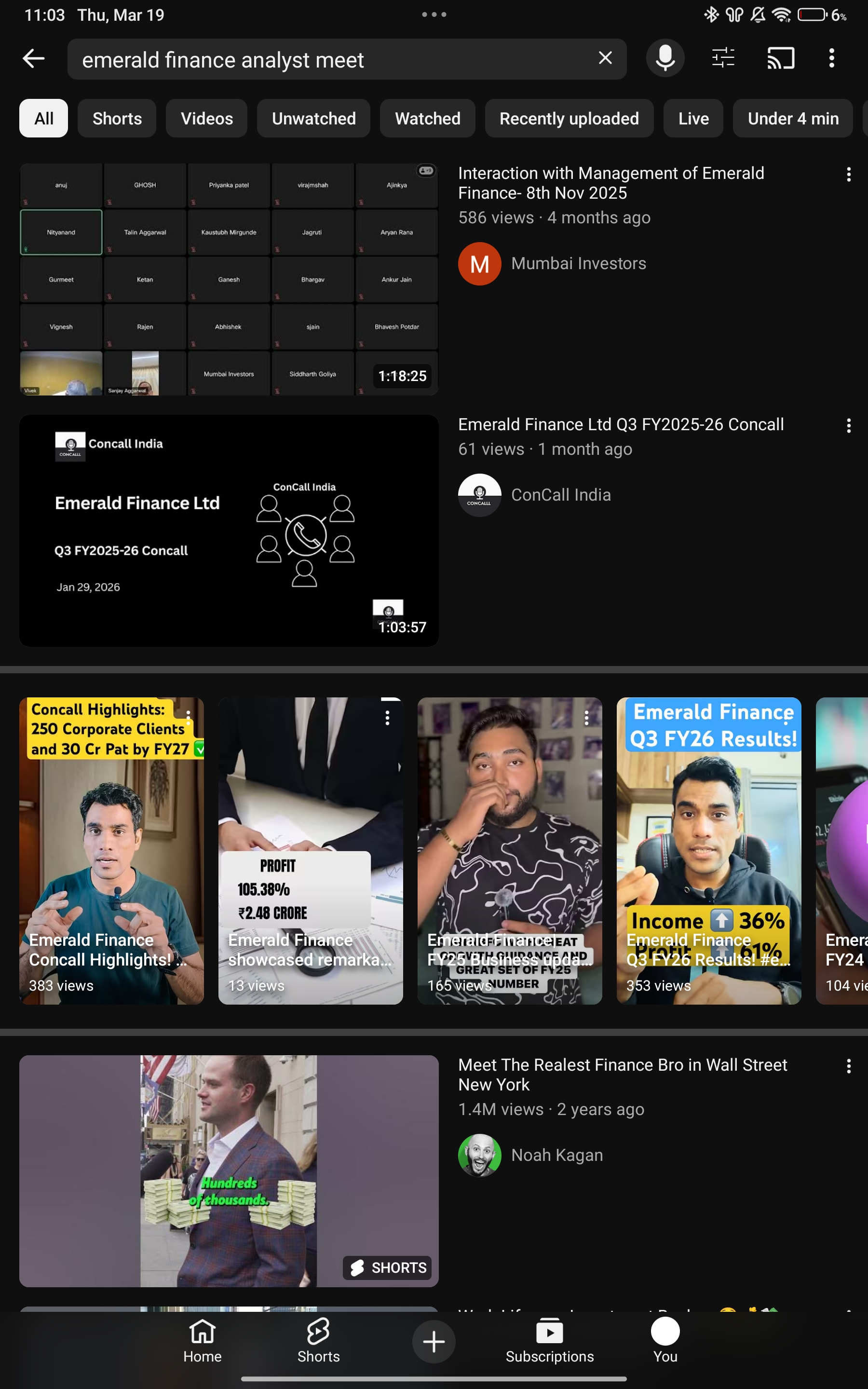

Help me out on 1 thing guys. The management did an analyst interaction on 8 Nov 2025. I watched it on YouTube and it was helpful, even better than the concall. They did a similar interaction after Q3, I was notified on screener. I tried looking it on YouTube, on their website but can’t find it. Could you help find that please.

Regarding their share purchase Harsh, yeah it helps a lot boosting confidence and faith in the company. I have also bought 14000+ shares this month.

You have entered at a great price, Virat! having said that, could you please tell me which channel you found the previous interaction? And we can figure things out.. I know which Q3 analyst meet you’re referring to but wasn’t sure that these are also available publicly on YT.

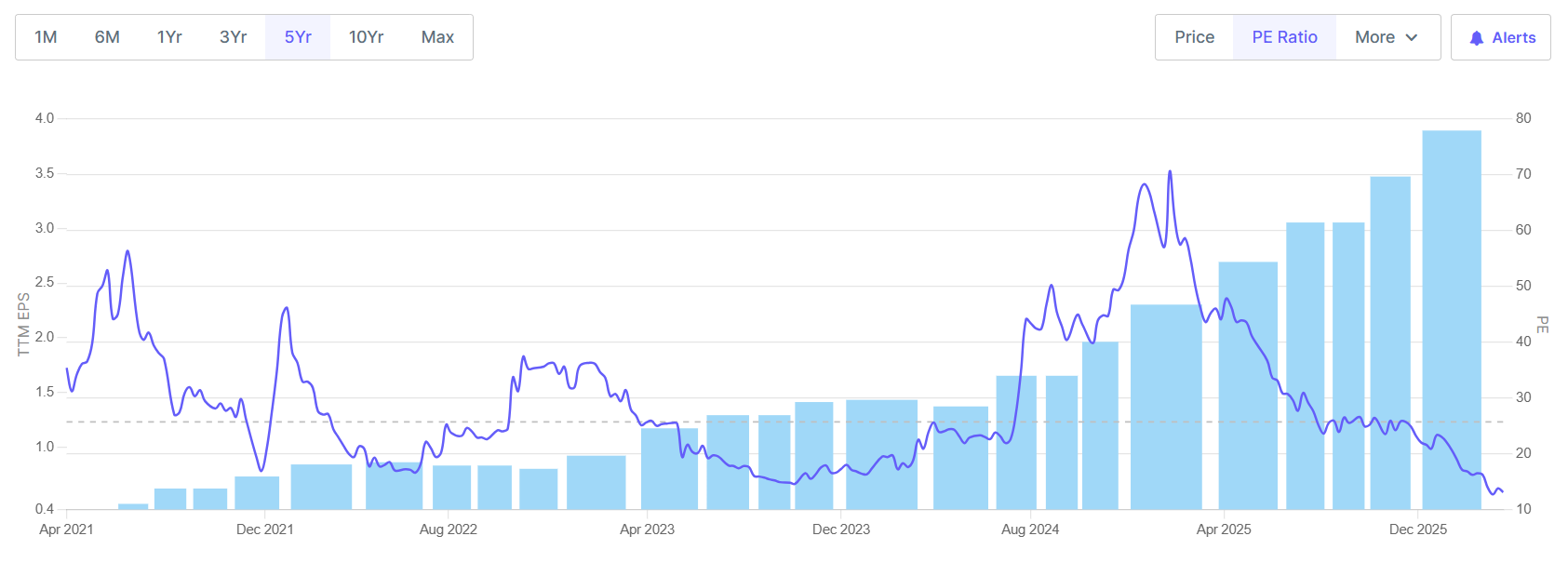

Markets can sometimes be weird! The P/E ratio of such a high growth, high visibility microcap at an all time low!!

Share prices move in waves. The higher the peak,the lower the trough. Infact, if emerald dint hit 160 rs at 70 p/e which was stupidly expensive, then maybe Emerald would have been closer to 80-90 rs. Current prices are stupidly cheap, so absent any serious issues, it’s looking real good.

Also p/e is below long term averages and even below their pre EWA days. That itself says a lot. Conservative p/e should be 25-30 in my opinion given the tech angle and growth

Not sure what is the correct way to value emerald finance but ewa profit are very small percentage so I think it’s valuation as P/B .current P/B is 1.8 which is still near to median P/B of nbfcs(1.75).so I think it’s not cheap but reasonable.

Agreed! But I think its book value is also increasing at a fast pace and on a forward basis the current P/B compresses rapidly. Hence the market is not discounting its growth right now in the valuations.

Infact P/B may also not be the best way to value it as only about half the income of the company comes from own books (interest income) the remaining half is a fee based income, where the income doesnot come because of the books of Emerald hence, P/E does make some sense as well. Just thinking out loud.

1.8 PB for an NBFC growing at 30 odd percent with almost nil NPA is cheap

SOTP would be the best way to value emerald imo

Slow growth in corporate additions (only 30 so now the total corporates onboarded stands at 210) but massive uptick in their gold loans disbursement in quarter Q4 (375Cr+) averaging at a 125Cr/month run rate for the quarter. This was and will be expected given the rise in gold prices (for the month of December it was 105Cr). But RBI recently came with a rule change in the repayment method for gold loans (regarding bullet loan repayment). Attaching the summary of a Ken Article I read regarding Bain Capital’s (a major global PE fund) investment in Manappurnam Finance and how RBI impacted it. Wonder how it may compress there commission structure for newly originated loans for these NBFCs (especially given that they are the lead DSA for Muthoot). They might renegotiate their commission rates with their DSAs maybe, given their own NIM compression??

SUMMARY (The Ken Article today):

The Competitive Landscape

-

The Shift in Dominance: For decades, specialized NBFCs like Muthoot and Manappuram controlled the gold-loan market due to their speed and local presence. Now, banks have aggressively entered the fray, lured by high yields and low defaults.

-

Bank Aggression: Public and private sector banks have rapidly grown their gold-loan portfolios, often offering interest rates significantly lower (8–10%) than the 18–24% charged by NBFCs.

-

Yield Pressure: To compete with banks, specialized NBFCs have been forced to lower their own interest rates, leading to a visible compression in their Net Interest Margins (NIMs).

-

Fintech Entry: New-age fintech startups (e.g., Rupeek, Indiagold) are acting as aggregators, partnering with banks to offer doorstep gold-loan services, further eroding the NBFCs’ “convenience” moat.

Operational Nuances and Risks

-

LTV Regulation: The Reserve Bank of India (RBI) mandates a 75% Loan-to-Value (LTV) ratio. When gold prices drop, many loans breach this limit, forcing lenders to call for more collateral or auction the gold.

-

Price Volatility Management: While rising gold prices help increase the book value of loans, a sudden crash is the biggest systemic risk for these lenders.

-

Speed vs. Cost: The core value proposition of NBFCs remains speed (15-minute loans), whereas banks, despite being cheaper, often have more bureaucratic processes and paperwork.

The “Value Migration” to Diversification

-

De-risking the Portfolio: Both Muthoot and Manappuram are aggressively diversifying into non-gold segments like Microfinance (MFI), Housing Finance, and Vehicle Finance to reduce their reliance on gold.

-

Profitability Mix: While gold remains the cash cow, the faster-growing MFI and housing arms are expected to contribute a larger share of the bottom line in the coming years.

-

The Valuation Gap: Despite strong earnings, the stock market has been cautious with gold NBFC valuations, fearing that the golden era of “easy growth” is over due to bank competition

The Death of the “Bullet Loan” Playbook

-

Regulatory Game-Changer: New RBI rules (effective 1 April) mandate that the 75% LTV ratio must be maintained throughout the life of the loan, not just at disbursement.

-

Bullet Loan Mechanics: In bullet loans (60% of NBFC portfolios), interest is not paid monthly but at the end. This causes the “Effective LTV” to rise every month as interest accrues.

-

The Ceiling Breach: Under the old system, a loan starting at 65% LTV would often end at 80% due to accrued interest. The new rules make this illegal.

-

Forced Friction: NBFCs must now either force rural borrowers into unfamiliar monthly interest payments or drastically reduce the upfront cash disbursed.

-

Shrinking Disbursements: Industry experts (Crisil/ICRA) predict that initial LTVs will drop from ~68% to ~55%, resulting in 25% lower loan amounts for the same gold.

-

Margin Erosion: The yield compression across the industry is expected to be 1% to 2.5%, depending on how much banks turn up the heat.

-

The Operational “Clog”: Moving away from the “bullet loan” habit increases customer acquisition costs and introduces massive friction for the core rural borrower

-

-

The Bottom Line: The article concludes that while the “Golden Era” of monopoly for Muthoot and Manappuram is over, the market itself is expanding, and they remain formidable players who are now being forced to evolve.

wont it get reflected on its Annual report when analysing Cash Flow statement’s in-depth detail ?

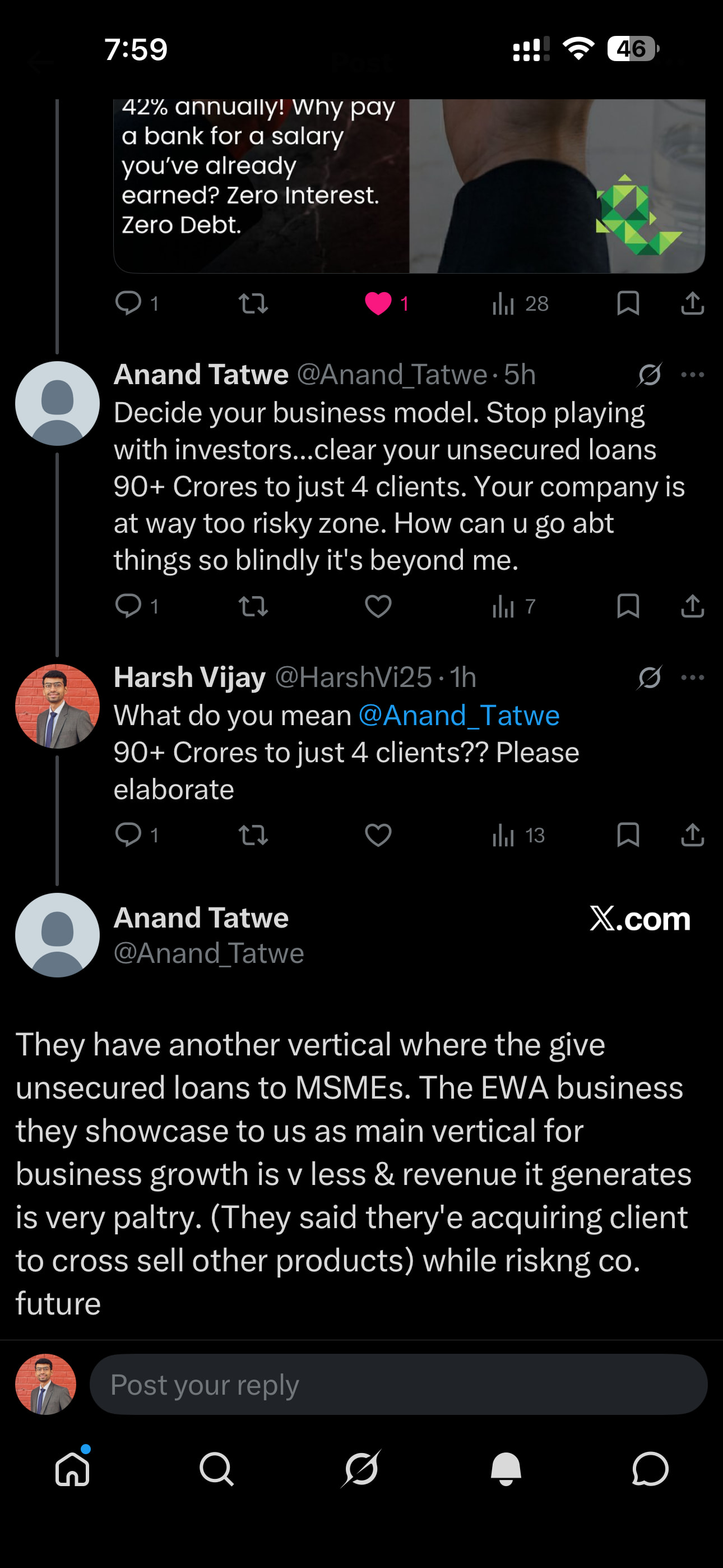

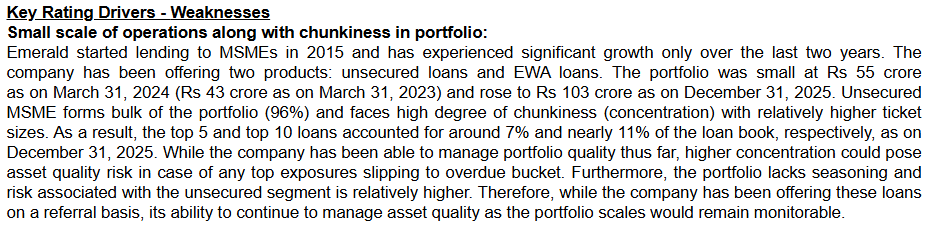

Just read this section in the recent Crisil rating report. No need to worry; that guy was over-exaggerating it by orders of magnitude. The top five loans only accounted for about 8 crores or 7% of the total loan book and not 90+ Crs.

Eagerly waiting for the results, the size of the companies they are tieing up is really small, like one was just an electronic shop. The rate has slowed as well, I hope there is atleast 12%MoM increase in sales. Will like to read their annual report as well, and if any of you guys get to speak in concall do ask about-

- their aspirations of being a ‘big bank like kotak and hdfc’, they said it in one of their old concall.

- customer retention and repeat, what percent of the EWA are from repeat users

Hope for the best, The MSME loan will be in focus while customer acquisition through EWA.

In EWA big fishes is yet to be catched. Let’s see

The company has found that its sweet spot lies with mid-sized companies having 200 to 500 employees, as this size is optimal for their sales cycle, engagement, and conversion rates. Despite this focus on mid-sized businesses, they have successfully onboarded larger entities, including a Municipal Corporation with 3,000 staff, an IT company with 1,500 staff, and EBIX Technologies with 3,500 employees.

When it comes to targeting very large companies, Emerald Finance is open to them and has made some efforts through HR firms to approach large conglomerates. However, management has stated that penetrating very large companies (like Tata Steel) is highly difficult due to bureaucracy, which is why they prefer focusing on mid-sized companies where decision-making is faster. Furthermore, they generally do not target public sector companies, the armed forces, or government bodies, as these organizations typically already have robust internal employee loan programs and subsidized schemes, making Emerald’s product less lucrative in that space

(source is their concalls, formatted with llm)

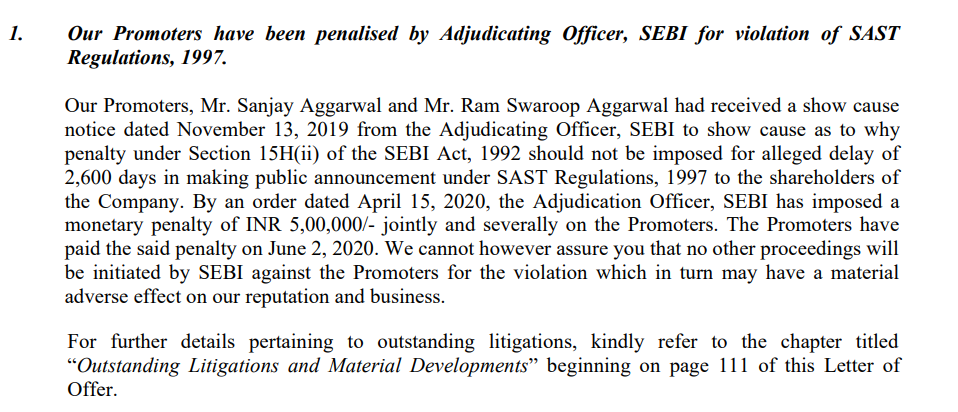

there’s a 2020 SEBI adjudication order against the promoters in the matter of Emerald Leasing Finance and Investment Company. Does anyone know what the matter was exactly and whether it has been resolved and what happened? Asked Talin as well on LI but haven’t received an answer yet.

Have a few more queries, eagerly awaiting the next concall.