About the Company

Emerald Finance Limited is an Indian non-banking financial company. Originally incorporated as Emerald Leasing Finance and Investment Company Limited in 1983, it rebranded to its current name in April 2023 to reflect its evolving business focus.

Headquartered in Chandigarh, Emerald Finance specializes in retail and MSME lending. Its product portfolio includes personal loans, business loans, machinery loans, home loans, loans against property, invoice discounting, and microfinance. The company also offers a digital product called Emerald Early-Wage-Access (EWA), which provides employees with on-demand salary access, allowing them to withdraw a portion of their earned wages before payday.

Through its subsidiary, Eclat Net Advisors Private Limited, Emerald Finance acts as a loan origination platform for over 40 financial institutions across India.

Service Offerings

1) Lending: The company is a non-deposit-taking NBFC, focused on retail and MSME lending. It acts as a loan origination platform for 40+ financial institutions including SBI, Canara Bank, Yes Bank, Axis Finance, etc via its subsidiary, Eclat Net Advisors. It has also broadened its offerings to include personal loans and business loans. The company had NIL NPAs during 9M FY25.

2) Early-Wage-Access: In FY24, the company launched a digital lending solution for Early Wage Access (EWA), offering salary advances through employer partnerships. It secured 40 partnerships, with 31 active as of the third quarter of fiscal year 2025. The EWA program was expanded to include 250+ brand vouchers from companies like MakeMyTrip, Amazon, Zomato, etc. As of Q3 FY25, the company has processed Rs. 46 Cr in salary advances.

Focus

Emerald Finance’s Early Wage Access (EWA) product is rapidly gaining traction as a key offering in the employee financial wellness space. As of March 31, 2025, the company had secured 62 active employer partnerships, surpassing its projections for the year. Management now aims to scale this to 250 partnerships in FY26, reflecting strong market demand and confidence in the product. EWA enables employees to access a portion of their earned salary before payday, a concept well-established in the US and EU and now increasingly adopted in India, Indonesia, and the Philippines.

In March 2025 alone, disbursals crossed ₹3 crore, exceeding the ₹2 crore projection, with an average ticket size of ₹25,000 and approximately 30 daily active users. Positioned at the intersection of technology and financial inclusion, EWA is becoming central to Emerald Finance’s broader strategy to offer responsible, employer-backed credit access to working professionals.

Product Portfolio & Business Model

a. Earned Wage Access (EWA)

- Nature: Short-term personal loan (28-30 days), deducted from next payroll.

- NPA Classification: NPA, if any, is on employee, not employer.

- Pricing: Employee pays a fee (not employer); “APR, so this one does not fit in line with what the banks can do.”

- Competitive Positioning:

- Full-stack model: Distribution, technology, lending all in-house; not dependent on LSP/fintech partners.

- EWA is used as a “customer acquisition tool” to cross-sell higher ticket loans (personal, vehicle, business loans) via subsidiary ShubhBank.

- Engagement: 10-12% of employees in partnered corporates use EWA, with 80-85% repeat usage.

b. Bill/Invoice Discounting

- New Strategic Partnership:

- Tie-up with Baya PTE Ltd. (Singapore) for invoice discounting.

- Targets suppliers to large anchors (JSW Steel, Delhivery, PVR, Reckitt & Coleman, Haldiram).

- Not a vanilla product: Baya acts as LFC and technology platform; stringent due diligence, only AA+ anchors, 6-month proven track record required.

- Margin: “They get about 17% and 50% of the processing fees net.”

- Rationale: Cross-sell to corporates already onboarded for EWA; underwriting already done.

c. Other Lending

- Loan Book (as of 31 March 2025):

- Total: Rs. 80 crore

- Business Loans: Rs. 77 crore

- EWA: Rs. 3 crore

- All loans are unsecured; cross-sell includes both secured and unsecured via own book and DSA.

- Gold Loan:

- Distribution for HDFC, ICICI, and soon RBL; not impacted by recent RBI guidelines.

d. Technology Stack

- In-house Tech: 5-member IT team, fully in-house platform.

- Business Continuity:

- Robust disaster recovery; “can go live with the entire data in less than 12 hours.”

- Compliance with RBI IT norms.

- Mobile App: Approved by Play Store, launch imminent.

Financial Performance

-

Q4 FY25 (Consolidated):

-

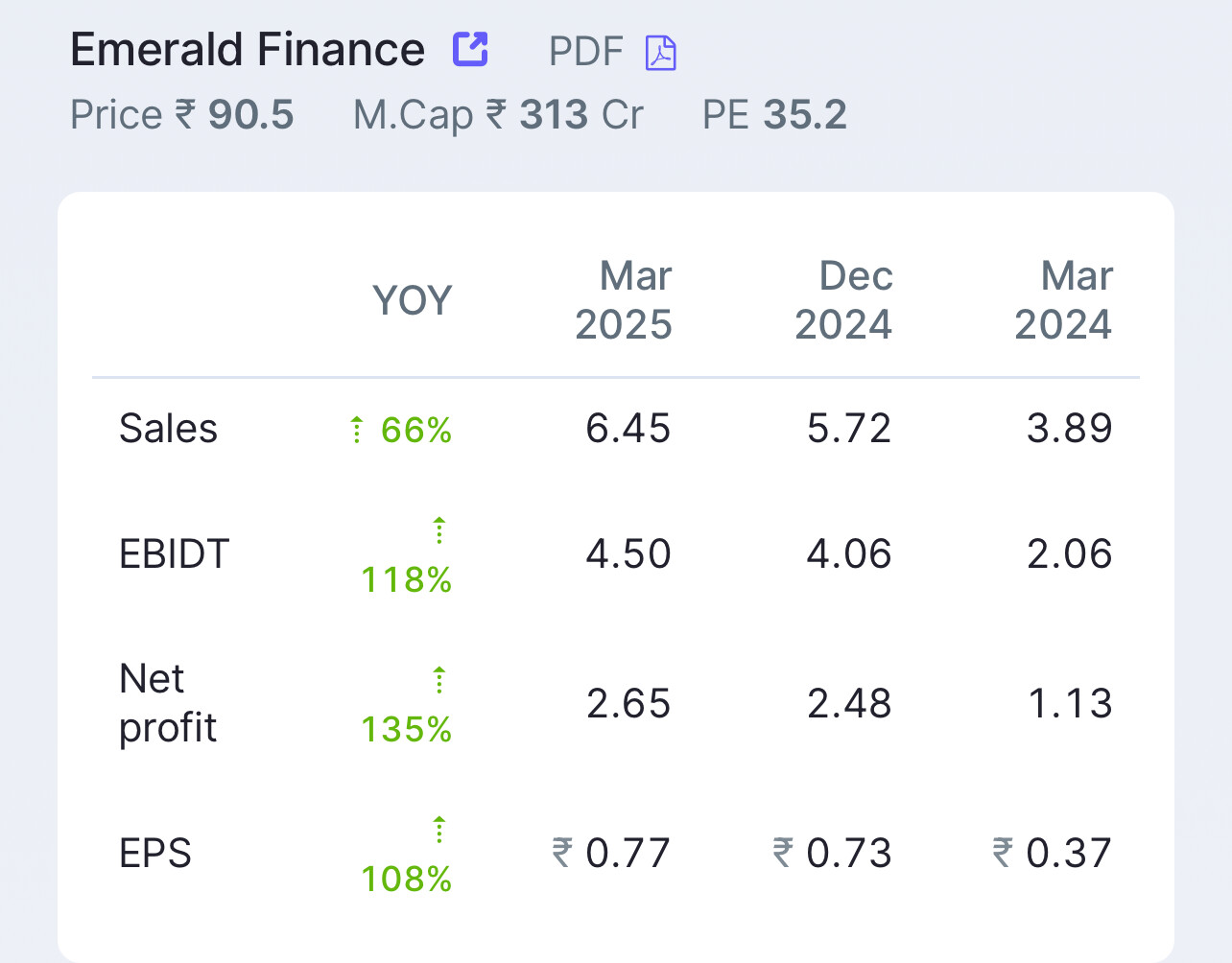

Total Income: Rs. 6.5 crore (vs. Rs. 3.9 crore YoY)

-

Net Profit: Rs. 2.65 crore (vs. Rs. 1.14 crore YoY, +132%)

-

Q4 FY25 (Standalone):

-

Total Income: Rs. 4.6 crore (vs. Rs. 2.02 crore YoY)

-

Net Profit: Rs. 2.16 crore (vs. Rs. 0.63 crore YoY, +246%)

-

FY25 (Consolidated, Full Year):

-

Total Income: Rs. 21.63 crore (vs. Rs. 13.36 crore YoY)

-

Net Profit: Rs. 8.89 crore (vs. Rs. 4.14 crore YoY, +114%)

-

Asset Quality:

-

“NPAs are absolutely zero” for FY25; historically <0.5% over last 3 years.

-

Management is focused on keeping delinquencies “very low,” even at the cost of growth.

-

Revenue Mix:

-

48% from interest income, balance from fee-based (processing, DSA, customer charges).

Industry Outlook & Management Commentary

-

Industry Trends:

-

NBFCs have 22% share of credit market; projected 17% growth in FY25.

-

Digital lending expected to be 60% of Indian tech market by 2030.

-

Competitive Moat:

-

“Only four major rivals” in EWA in India; Emerald claims end-to-end control, zero delinquencies, and robust tech as differentiators.

-

Risk Appetite:

-

Conservative stance: “We do not want to take extraordinary risk at this stage.”

-

Growth will not come at the expense of asset quality.

-

Vision:

-

Ambitious scaling: Targeting 1,000 corporates in EWA over time.

-

EWA as a “Bajaj Finance consumer durable” equivalent—acquisition channel to build credit history and cross-sell.

Guidance & Outlook

-

FY26 Targets:

-

250 EWA partner corporates.

-

EWA disbursement: Rs. 15 crore by March 2026.

-

Business loan book: Rs. 110+ crore.

-

Maintain zero/very low NPA.

-

ROE:

-

Currently at 10.8%; management prefers low-risk, low-leverage model.

Key Risks & Threats

-

Ticket Size & Scale:

-

EWA is a small-ticket, high-volume business; scaling requires significant volume growth.

-

Concentration:

-

Business loan book still dominates AUM; EWA is only ~4% of total book as of FY25.

-

Execution:

-

Success depends on ability to onboard and activate large number of corporates and drive usage among employees.

-

Competition:

-

While only “four major rivals” for now, the space may attract larger NBFCs/banks in the future.

-

Regulatory:

-

EWA operates in a regulatory grey zone; management claims compliance with RBI norms, but regulatory risks remain.

Conclusion

Emerald Finance has delivered robust financial performance in FY25, underpinned by rapid scaling of its EWA product and prudent risk management. The company is leveraging technology and a full-stack business model to create a differentiated position in digital lending, with strong cross-sell synergies via its DSA subsidiary. Management is highly optimistic about the future, targeting aggressive expansion in EWA and invoice discounting, while maintaining a conservative risk posture and zero NPA. Execution on scaling, maintaining asset quality, and leveraging its capital base will be key to sustaining its growth trajectory.

Disc: Invested 1.5% of my portfolio.