@dd1474 Since you have been an investor in Embassy for a while, how do you feel about them appointing the ex CEO (Aravind Maiya) who was barred by SEBI now as the Chief Strategy Officer given his shady background.

@myloginid

I have invested in Embassy. While I appreciate Aravind Maiya being made moved from KMP post SEBI order, it fits within my investment profile requirment. I would rather be more concern about Embassy Promoter Virwani group, which hold stake, related party on most of purchase of the company and also influence on conduct on business. Aravind appear to be being a professional and despite critical position, I assume would have limited meanvouring ability in conduct of business, since he does not control ownership. This is my current understanding. It may be wrong and I may change my view based on development, increase/decrease/exit from my investment without informing forum. I have been wrong more often, sepcially when I tried to project future. ![]() (I have unique capacity to be wrong even to understand past events). Further, Promoter integrity is very personal matter and one shall do own evaluation and invest in my view. The assessment of promoter is the most important factor when bad news/adversity faced by the business. At that point, our conviction in business is signficantly determine by our view on promoter/manager integrity. Hence, I would suggest to please do through working before making any investment decision.

(I have unique capacity to be wrong even to understand past events). Further, Promoter integrity is very personal matter and one shall do own evaluation and invest in my view. The assessment of promoter is the most important factor when bad news/adversity faced by the business. At that point, our conviction in business is signficantly determine by our view on promoter/manager integrity. Hence, I would suggest to please do through working before making any investment decision.

Discl: Same as previous note.

4 Likes

Thanks Dhiraj. PPFAS has also taken up a significant position in Embassy and that adds to some “trust”.

But same as you I have been wrong many times before trying to seek better returns given the gross shadiness of Indian corporates and the unwillingness of SEBI to just outright sue and jail such culprits (DHFL, Yes Bank, NSE Colo, Ketan Parekh, Gitanjali Gems and the list goes on and on). Financial penalties are just not good enough IMHO to clean up Indian corporates.

3 Likes

this is not directly related to Embassy but the newly listed REIT " Knowledge Realty Trust" going over the DRHP

“We own and manage a high-quality office portfolio in India, and upon listing, we will be the largest office REIT in India based on Gross Asset Value (“GAV”) of ₹619,989 million as of March 31, 2025 as well as by Net Operating Income (“NOI”) for FY2025 of ₹34,322.67 million. 1 We will also be the second largest office REIT in Asia and one of the largest office REITs globally in terms of Leasable Area as of March 31, 2025. Our Portfolio comprises 29 Grade A office assets totaling 46.3 msf as of March 31, 2025, with 37.1 msf of Completed Area, 1.2 msf of Under Construction Area and 8.0 msf of Future Development Area”

I didn’t see any thread on this, hence wanted to check if anyone has looked into this.

Thanks

1 Like

I have invested in IPO and also purchased at Rs 103-104 on first day on listing. The REIT is promoted by Blackrock and also have office assets in kind of equal spread in Mumbai, Bangalore and Hyderabad. My expectation based on IPO talk is annualised distribution of Rs 7.2/unit for FY26 (adjusted for 7 months of listing, approximate Rs 1.8/unit in next two quarters) and I found it attractive at that level. At 107-108 price it is trading as same yield as compared with existing REIT.

Disclosure: My view may be biased due to my investment. I may not correct understanding of REIT market. I ma not suggesting any investment action in the REIT. Reader shall do his/her own due diligence before making any investment. I am not SEBI registered advisor.

11 Likes

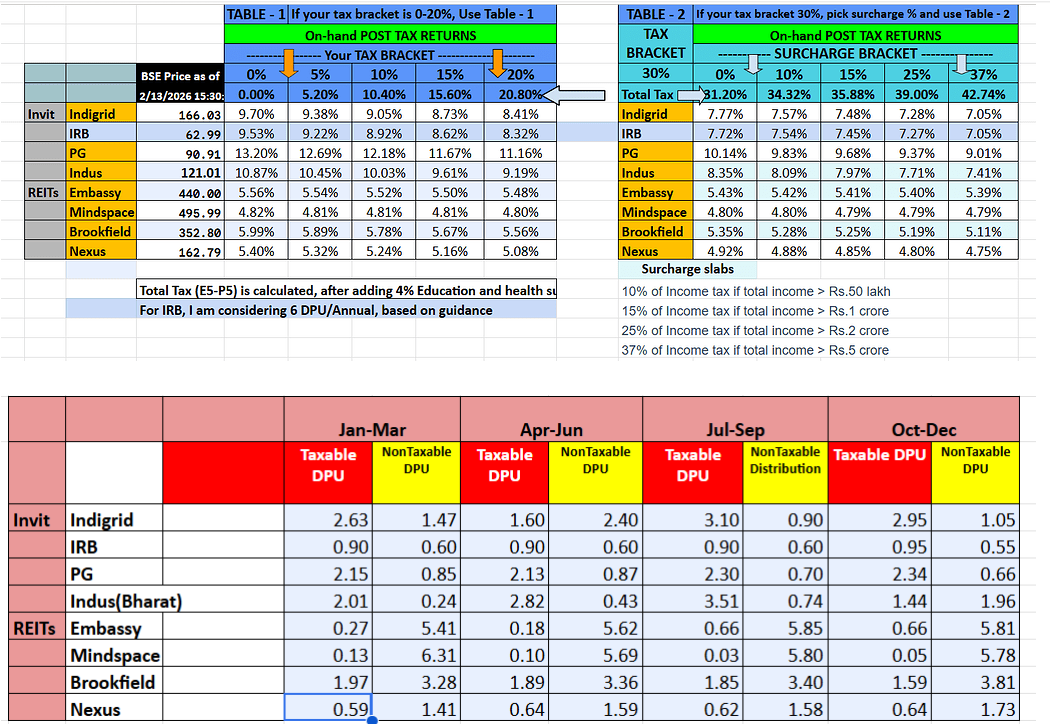

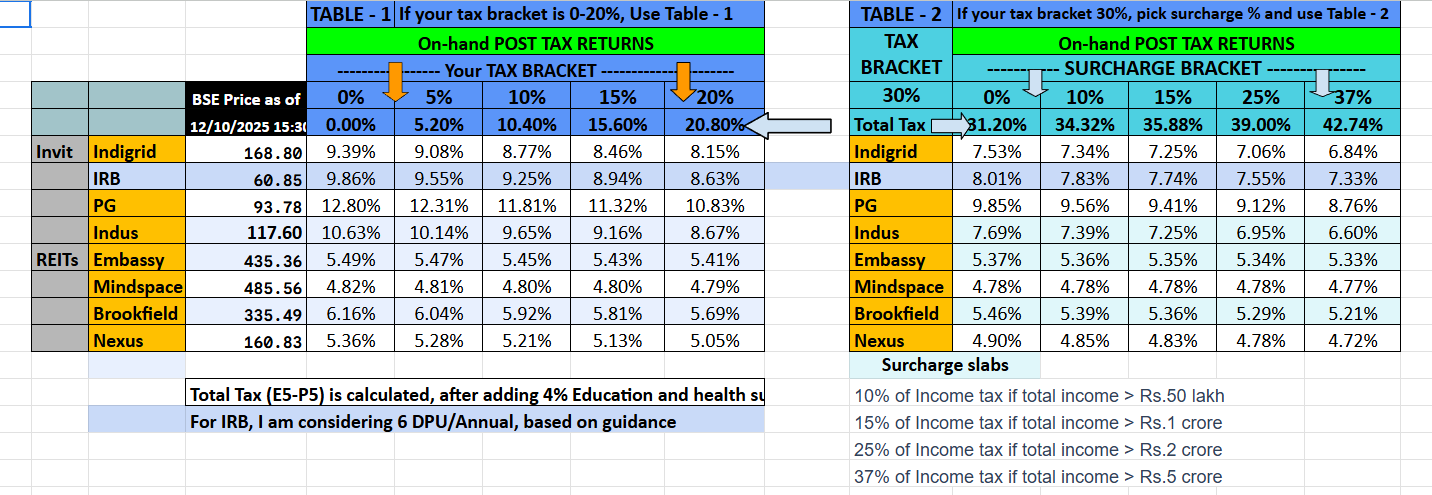

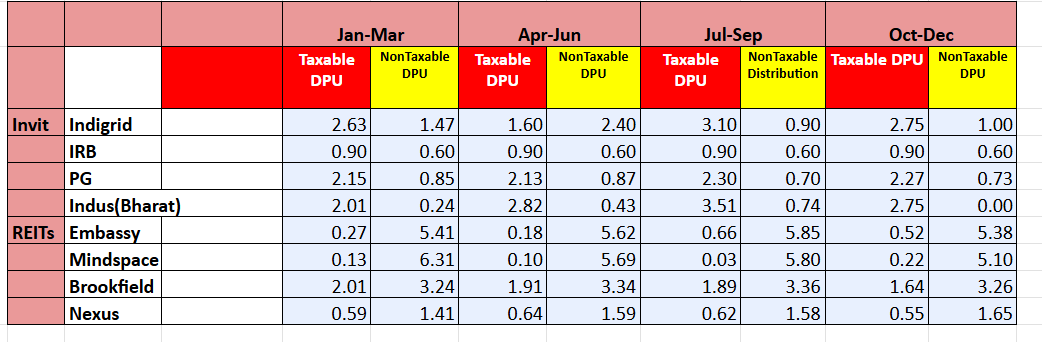

Post tax Yield tables, based on running 4 qtrs…before you deep dive into the numbers, here are some important points to be read

- The separation of taxable and non-taxable is a tedious job and one can be only sure, if you have the distribution advice (one can look at the TDS and if there is TDS, I take it as taxable). Since I don’t own every single REIT and INVIT below, there can be an odd mistake but that is why, I am giving the underlying table, that feeds into this yield calculation. I am no expert in Tax and hence do your diligence

- The fine print in IRB’s case is that, I have assumed, the last qtr payment of 1.5 DPU (and its breakup) as the common one across the entire year since using the previous 2 DPU will not give the correct picture

- The intent as always is that , if you go and buy these instruments today morning at 9.15 AM (assuming they open at the previous day close price), then what will be the yield on hand? that is the intent…

- Comments are always welcome

16 Likes

Hi Kalyan, you are doing a great job providing this detailed yield table of InvIT and REIT! Truly helps in providing a comprehensive look across these asset vehicles.

4 Likes