Management is walking the talk.

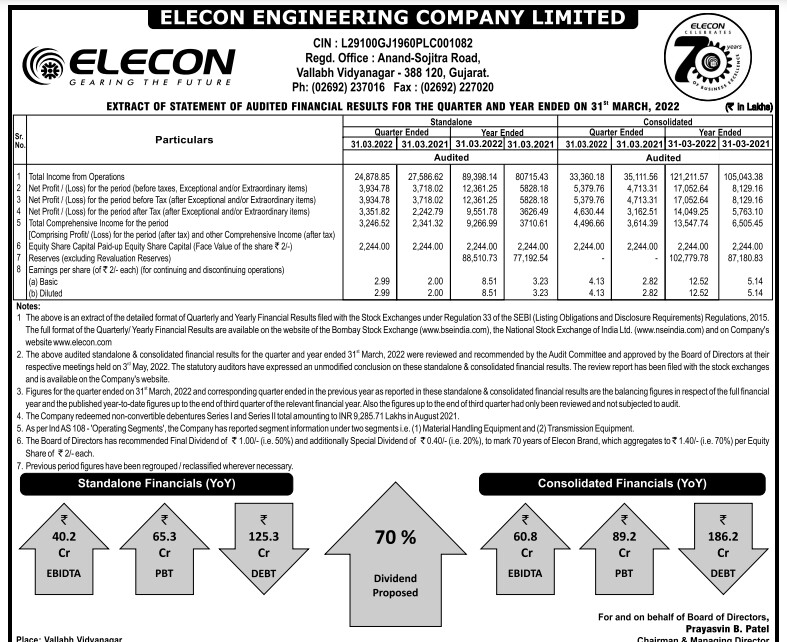

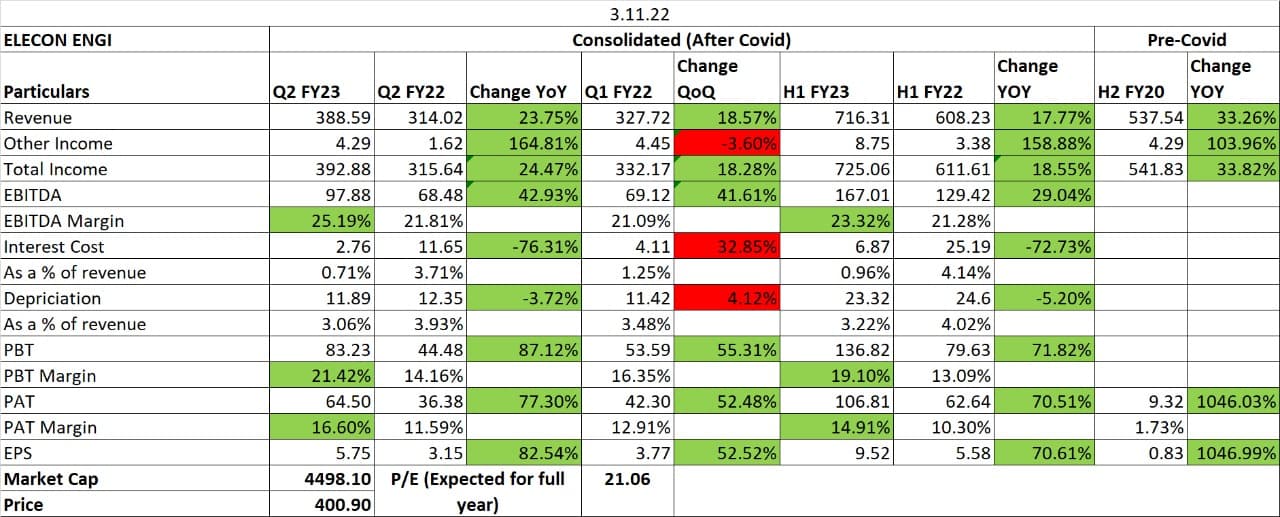

Substantial reduction in interest cost…from 12 cr of interest cost in Q2 to 4.82cr in Q3.

Waiting for Q3 earnings call to hear from the management.

Management is walking the talk.

Substantial reduction in interest cost…from 12 cr of interest cost in Q2 to 4.82cr in Q3.

Waiting for Q3 earnings call to hear from the management.

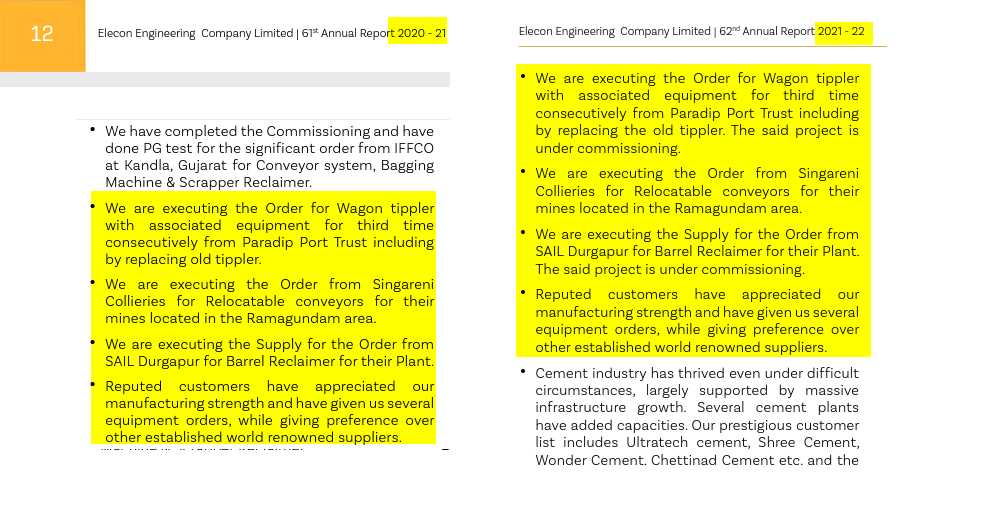

Results seems to be fine. Gear divison business seems to be doing well. Capacity utilisation can go up and that can aid in margin expansion.

Can do a 20% growth in gear divison as per management on topline in gear division provided Navy order also materialized which they are hopeful will flow in.

Debt reducing which will be beneficial which will lower interest cost .

With boost to infrastructure and industry they cater to power, steel and others looks like next 2 years will be good for business.

Insider buying 35000 shares purchased by aakash mechatronics group company of elecon

Once they get debt free we can see some P/E re-rating happening.

Management is confident to be debt free before timeline.

Also interest cost will be saved and be added to bottom line.

As company has only 60% capacity utilized with growth ticking in next 1-2 years will be good driver.

Have been seeing this company since some 15 years .

Since steel cement and other industries doing well this is a good proxy play for the same.

Imp points from Q4FY 22 Con call

• All overseas entity profitable & same to increase

• To invest in marketing activities to scale brand

• 410 Gear orders 5 months+127 MHE is 8-10 months order book- If things show traction can ramp up

• On April 30- 490 cr order book Gear division

• Exploration of new growth avenues to strengthen utilization levels

• 1500 cr fy24 revenue target - standalone

• 100cr capex over 2 years from internal accruals only

• Export to be 50% by fy 2030

• MHE Business retention money – No overrun costs pending for legacy projects, 2 projects money to be received, all 3 executed, near 100 cr, Majority to be received this year or max by Sep 2023

• EBITDA margin 15-20% for MHE business

• Growth of 30% expected be in gear business & margin to further improve

• Have 5 months order based on current year targets with healthy margins

• Debt reduction savings to add in bottom-line

• 12 cr interest cost for FY23

• Raw material price increase will not affect much as 5-10 days is the quotation validity

• New orders in MHE division is for products & payment terms & margins are very good. No retention money

• After sales service margin at 25%

• Passing of price is not being that difficult

• CAPEX – Large amt will be for alternative energy solar & wind

• Few machine tools which have aged will be replaced with new tech

• Some buffer for capacity expansion

• Gear capacity utilization at 65%

• Standalone 1500cr guidance

• Gear division 10-12% exports likely 15-17% this year end & ultimately 50% level is strategy

• Have got some opportunities in USA to start & our execution & references will act in our favor as its just entry point. Similar situation is starting to play out in South America

• Majority orders from Steel then cement & then sugar

• Recession will be a risk & avoiding debt will be key

• Capacity utilization for standard products 4-6 weeks. Right now, not utilizing sub-contractors, that provides a further opportunity to expand

• Steel orders expected in both Gear & MHE division

• With minimal CAPEX company can cater to maximum opportunity

• Gears export share q4 – 14%

• Market on overall basis is expanding

• Gears after sales revenue on sustainable basis -20 to 25%

• For Benzler Radicon Sustainable EBIT margins to be 18-22%

• No shortage expected at foreign entity level due to capacity – only labor can be issue. Demand is growing there in range of 10-15%

• For strategic acquisitions it will either be through internal accruals or through a strategic investment

• Steel plants will go ahead and put capacity, irrespective of inflation as they feel capacity will required for nation to expand. So demand does not hamper.

• Competitors include Shanti gears, premium gears, Flendor.

Can some one share latest conference call link

Can’t locate the same

Imp points Elecon Q1FY23 Concall:

• MHE business has turned profitable & so should be seen for full year

• Oversees impacted due to global logistics, order from there 114cr, should achieve our 140 target of export from India

• Employee cost up 35% YOY due to increased strength in Business development, designing, logistics

• See some companies in India are pausing CAPEX, however no reduction in demand, no impact on us as order book is good, maybe better for us as these are delayed

• Consolidated order book -617 CRS

• FY23 1500 CR top line expected – 1300 gear division & 200 MHE

• Scope for improving margin upwards of >20% with better capacity utilisation as Fixed costs is high in this industry (Can be a 25% margin business depending on product mix)

• Q2 export 25 CR expectation, 22 CRS for this qtr

• Presently retention money is 83cr from 110 last qtr

• Reasonably confident of CAPEX cycle to continue

• 1000 gear, 200 gear & 400 overseas subsidiary – Breakup of sales expectation (Gross & net will be 1500)

• Not seeing any change of demand/ impact particularly for steel sector

• Recently got 130crs order from navy, getting good enquires from defence, current order to be executed over 2 years. Same is not including in order book as received this week.

• Export & domestic margin over time should be same, currently export is higher, however can negotiate same for domestic

• Q1 generally is weakest vs a strong Q4 generally

• Risks can be from economy side

• FY 24 Consol >2000 Crs

• No strategy as of now in regards to use of surplus cash to be generated

• Negotiating with 2 customers in steel & cement space from USA. Can have good opportunity once brand name & initial orders are executed in this market.

Debt free status .

Next 1-2 years will be interesting .

Margin expansion and topline growth expected in next 1-2 years.

Next 2-3 quarters will set the tone for growth and margins .

Disc - Invested

Idea borrowed from Intelsense advisory .

Had been invested in elecon long back sold during downcycle in 2015.

Hello, does anyone have an Elecon engineering financial model?

Elecon Engineering Q2FY23 Con call Imp pints:

• Guidance: Standalone and Consolidated Revenue target of Rs. 1,500 Crores and Rs. 2,000 Crores respectively by FY24- This will be achieved keeping in mind bottom-line thus maintain margins & no price cuts- current operating margin guidance of 22% will sustain

• Planned Capex of Rs. 100 Crores over a period of two years considering revenue growth projection and long lead time for key machineries- 15Cr is solar of this

• Overseas & Exports Revenue composition to be 50% in Consolidated Total Revenue by FY30- Have started moving into south America & Canada from US markets as part of our strategy- Right now we are at 10%

• Outstanding retention money is 60CR- Till now all judiciary orders in our favour

• Order book (In hand) – Gear business 602cr & MHE 104CR for H1FY23

• New product development planetary gearboxes – Used in all type of industries – we have specialisation in cement, wind mills, coal handling, sugar plants-potential will be from few 100 to 1000Crs exact assessment is difficult – 300 to 500cr on annualised basis

• Freight costs have now rationalised- however receipt of material time is not reduced leading to longer lead times

• 70% revenue is from larger gearboxes & 30% from small to medium

• Defence orders on hand – 80 Crs. Indian navy & coastguard’s biggest competitors. Till now demand in same was cyclical typically 3-4 years. Now due to governments focus on shipbuilding we expect strong growth 5-7 years – 100 to 200crs orders can be expected potentially

• Steel, cement, power & sugar sectors constitute main order book

• EV opportunity for gearbox manufactures has lot of potential for likes of us – especially with domestic EV manufacturers. Will update once we sign for similar opportunity. In terms of skillset & deliverables falls under our expertise

• In MHE division margin to be increased to 15-17% as we achieve 400 CR benchmark- Conservatively will maintain as what we are doing now- Railways/ highways/ construction industry will drive growth

• Gear business margin is 24%- this will continue

• Operating at close to 60-65% without subcontracting- can increase more subcontracting without comprising margins. Even in house can go upto 85%

• We have put in a team to explore opportunities in defence apart from Navy in air force & other auxiliary departments. Since we have expertise to supply high precision complicated components.

• We are compared to likes of Flendor in tarnation markets. Our local presence through Benzlors/ Radiance in local markets helps us

• 30% gearboxes are customised & balance catalogue products.

• We are keeping our eyes open for right inorganic opportunities

• We have product line supplying to metros & railways excluding export, compressor also might come in future based on our capablity

Strong numbers for the quarter. Management also seems confident of the order book.

Management is current at 60-65 % utilisation and with 100 % utilisation they can do 2500-3000 Cr .

Looks like next 2-3 years good cash will be accumulated on book.

To be seen how management will use the cash going forward to scale buisness further.

Another good coverage to understand

If steel companies, sugar companies do capex. What is the guarantee that this company also benefits because there may be capex which may not be directly linked to benefit of elecon.

How is the corporate governance of the company

Is there any chance for order execution to be delayed due to recession in Europe- keeping into mind these things and taking a conservative approach- what can be the likely revenue and PAT for FY24

There are no guarantees , you can only take a view basis the application of products. Steel & Sugar are just one part , defence , infra also contribute to its topline.

Just take a look at their product line for more clarity on where growth is coming from.

Exports is also a good opportunity.

We need to now look beyond 24. If you read conference call for last 2-3 quarters / 1-2 years you will have more idea on topline bottom line