Nuvama also has AIF funds. In fact Nuvam’s owner is one of the top AIF manager in the Asia.

Before demerger Edel has two AIF- through Nuvam and their own AIF.

I think AIF is remunerative for a funds as it offers good returns much better than lending and requires less capital (in some funds Edel has placed 5% of the capital).

Based on their last week’s release, they want to separate AIF funds (sooner or later) so it is good move by MF subsidiary to go for their own AIF.

Additionally AIF market is nacent and huge run way, but needs time to get a real rewards (e.g carry income).

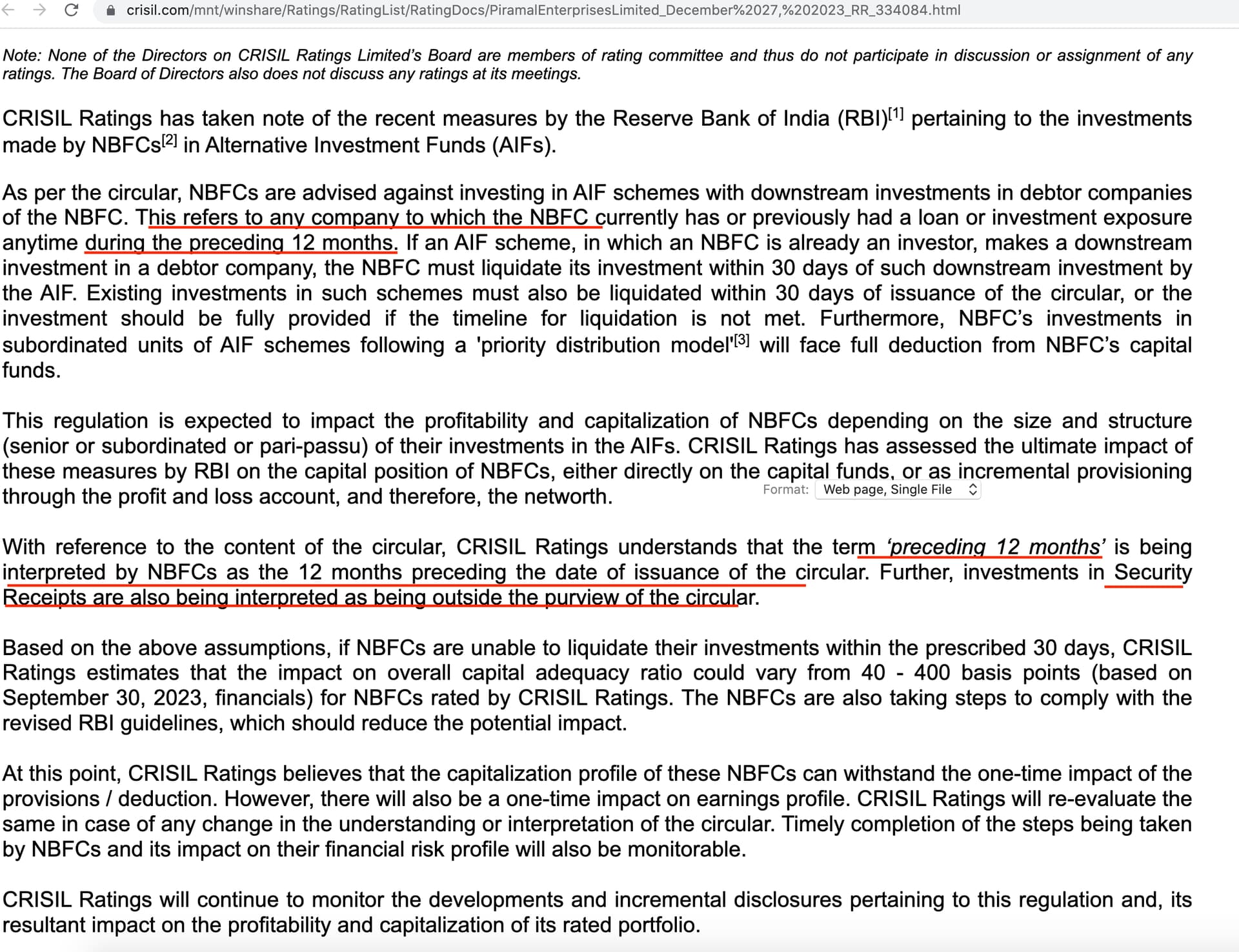

Unlike Mutual Funds, AIFs lack transparancy. Each MF declares its portfolio every month. The daily NAV and performance is clearly published. SEBI needs to come up with some disclosure norms for AIFs. They should be required to publish their portfolio at least quarterly. If this is not done more and more poor-quality papers/stocks will be pushed into these funds and the extent of the problem will be known only after some investors lose big money. Only transparancy can ensure quality

Rookie investor here. What I don’t understand is in the quarter of September company had PAT for insurance business. But there are multiple places in the earnings call(September) and ppt where we discuss insurance business to break even by 2027. What am I missing. Isn’t it already profitable ?

Nuvama has displayed excellent numbers in Q3. Wealth Management cos have all displayed good growth and profitability. This sector is clearly a sunrise sector with a long runway!

Why is Anandrathi enjoying premium valuation to Nuvama?? is it just because they do not have debts unlike Nuvama which has capital market business also???

I think that’s it. It is the capital markets business - effectively Investment Banking which is more cyclical, hence should have a lower multiple.

However there is some value to a joint offering if you can offer a promoter wealth management services for their personal wealth and capital market services for their business - so the flywheel is stronger.

And to add, I don’t think you can pencil any multiple expansion here but earnings growth will be durable and strong. In a couple of years they should probably institute a significant dividend as well (as a % of PAT)

You don’t need a lot of capex and operating leverage will be very good. This is effectively a 100%

Capital Allocation is one to look out for, you don’t want them going further down on the income/wealth range and you don’t want a lot of acquisitive growth.

I expect similar situation with the Alts business for Edelweiss - probably worth the whole market cap here.

They probably do make an economic profit but the way the insurance business works GAAP profits are away.

In layman terms - you acquire a customer at t0 for 100 and over T1 to t5 you’ll make 120 NPV from them. However you must charge the entire CAC today to the P&L. so it shows up as a loss today.

My concern is that these businesses are subscale and the market is large though fairly competitive.

Probably best to sell them as they’re on the verge of making money since these are fairly capex hungry and will be for a while.

Look at ROEs on that one. It is mediocre at best.

This used to be a very good business 5-7yrs ago. Now there’s restrictions on ownership structures and leverage - that makes this a lot less attractive.

@Srinidhi_Adiga Why do you think edelweiss is an inferior investment.? If they are able to payoff its debt wouldn’t it have a fair value of 45-60 T crores even with no additional revenue growth?

edelweiss is good, but Nuvama is much superior business model and as management is confident of having Flywheel effect with the scale they have achieved from here…

dis: extremely biased, heavily invested and with recent highs in share value it makes up 50% of my portfolio.

if you see in US the wealth management companies like Blackrock vanguard etc, the bigger gets bigger… Now compare it with India hardly 4-5 major players for such a huge market. say from 4 trillion India gets to 6 Trillion in next 2-3 year and with the market share Nuvama Commands now its AUM can grow from 3.3 lakh crore to 6.6 lakh crore(Conservatively), then revenue will easily be around 6k Cr, valuation would be at 15k/share.

What I meant was valuation metric. Do we look at price/book, market share/AUM etc while valuing a wealth management company.

I understand bigger picture but wanted to see relative valuation among Indian wealth management companies. Hence the question.