Yes I think it has a lot of potential and is a very strong business for them. I do not think the market fully understands that business, nor does it know how exactly to assign value to it.

1 Like

Can you please elaborate your understanding on the business, especially how revenue works and regarding debt…

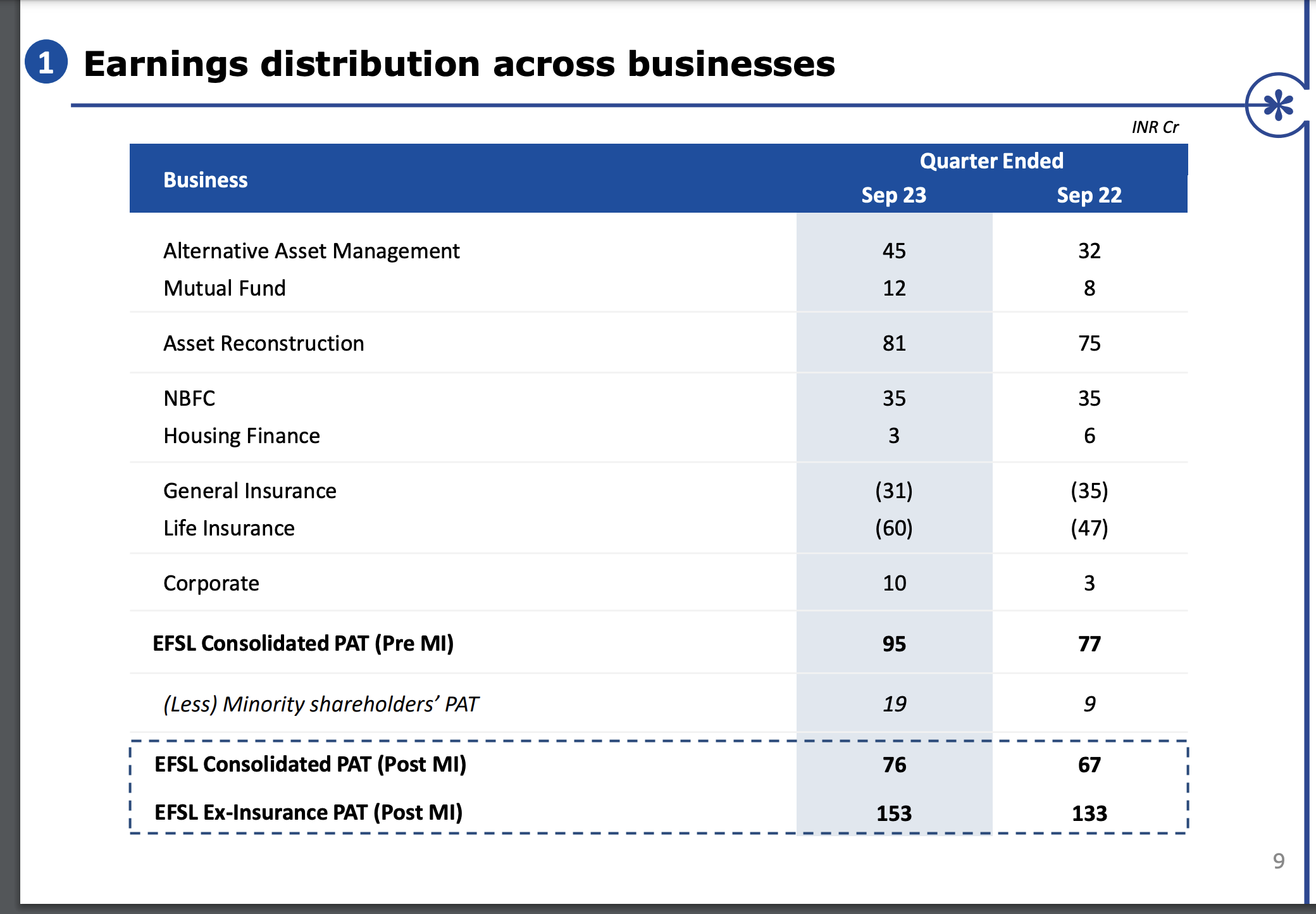

Edel reported decent Q2. Although the reported numbers does not seems different, but things are falling into place for Edelweiss after a long and brutal few years.

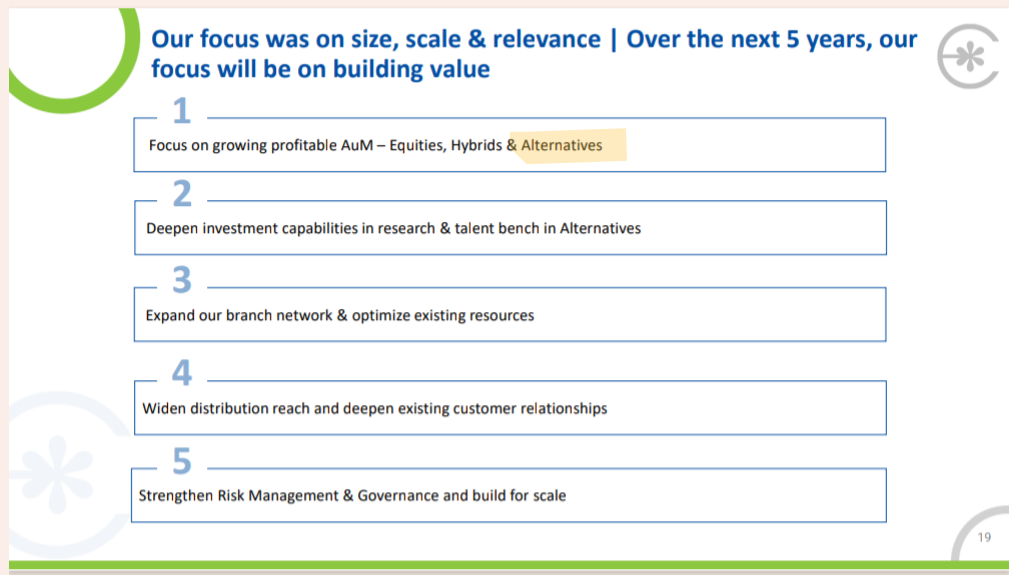

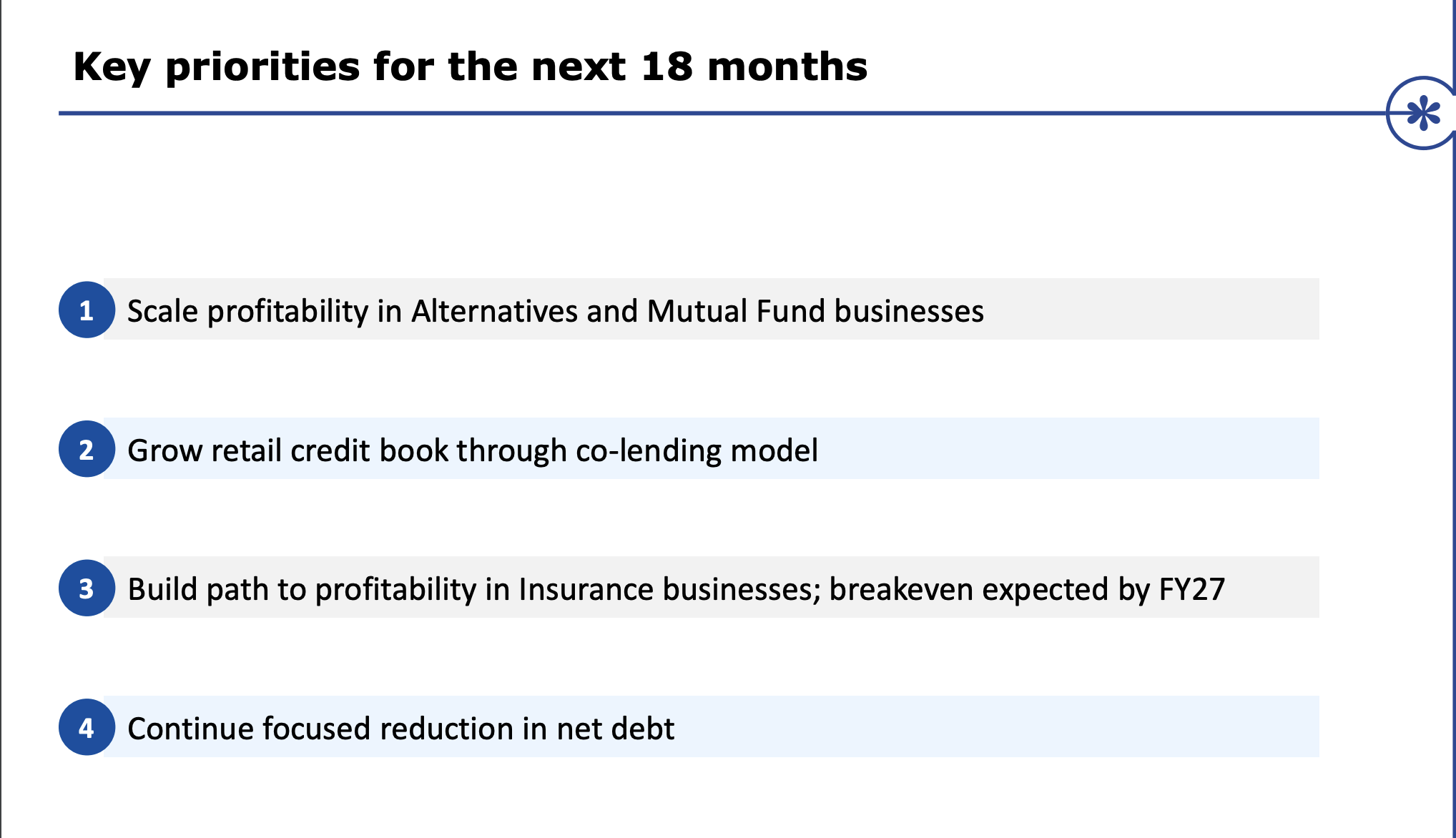

They have listed down key priorities and finally wholesale reduction is becoming less of a priority and other factors they will drive profitability seems to become more priority.

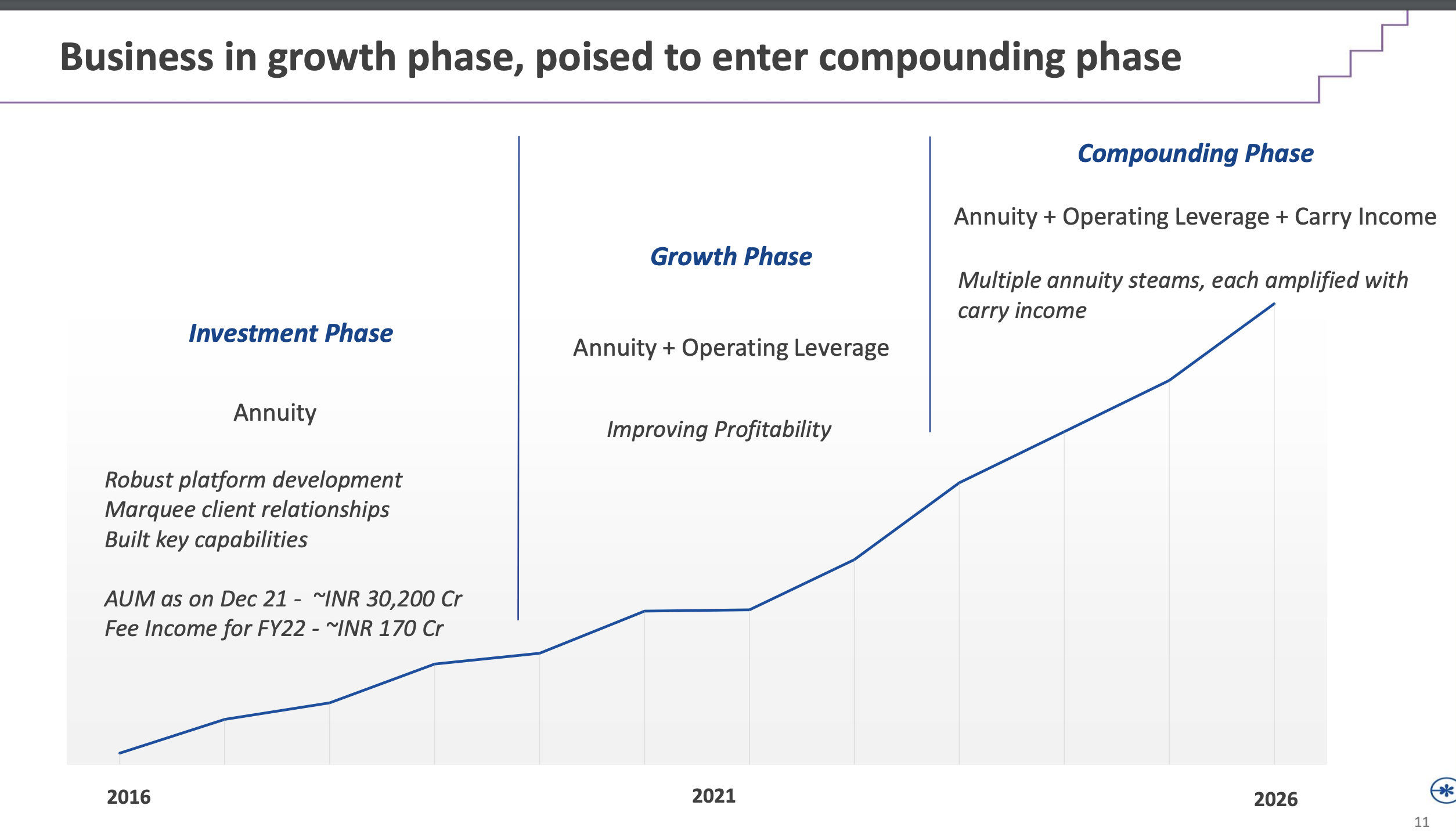

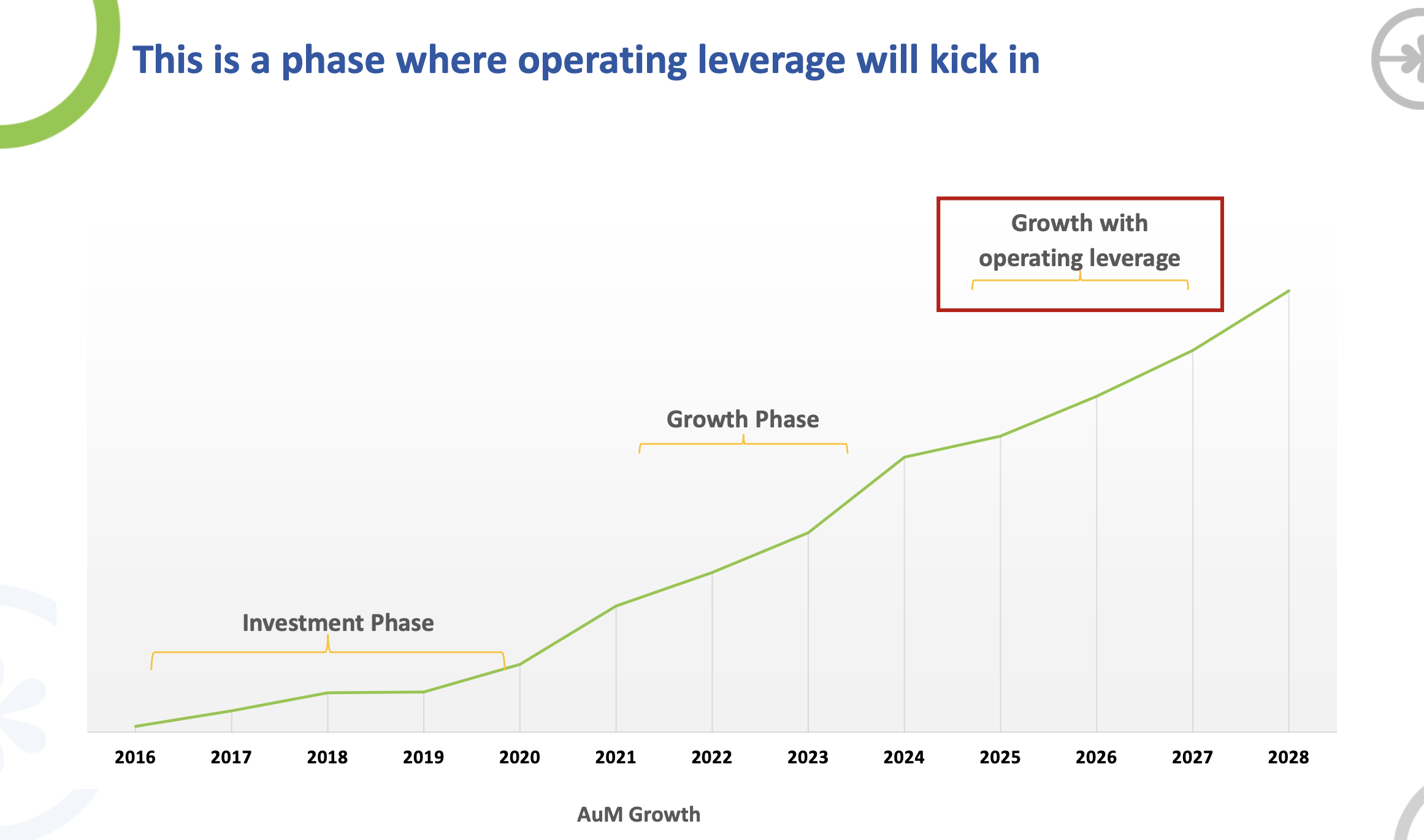

AIF is ready to take off, as they said in 2021/22.

In Q2 FY24

H1 PAT is around 70/80 cr, annualised to 150 to 170 cr PAT for Fy24. Their fee-based AUM of 27,000 cr is the same as committed capital in FY20/21.

This means they have doubled the deployed AUM (from 15 to 27,000 cr) in the last three years. Additionally, their earlier deployed funds are in good standing, boosting their carry income.

I won’t be surprised if AIF’s business profitability at least doubles in the next 3 years, and it could easily be in the range of 300-500 cr once the carry income becomes regular.

They are talking about profitable growth for MF business for the first time. This business is also sitting on operating leverage. Their SIP portfolio of 175 cr per month is quite handy. With the MF CEO joining Shark Tank as one of the investors, she will likely attract more attention to Edelweiss MF. Also, they are openly talking about improved profitability in the future, which is good.

From a PAT of 20Cr, it has the potential to improve towards 100 PAT in the next 3- 5 years.

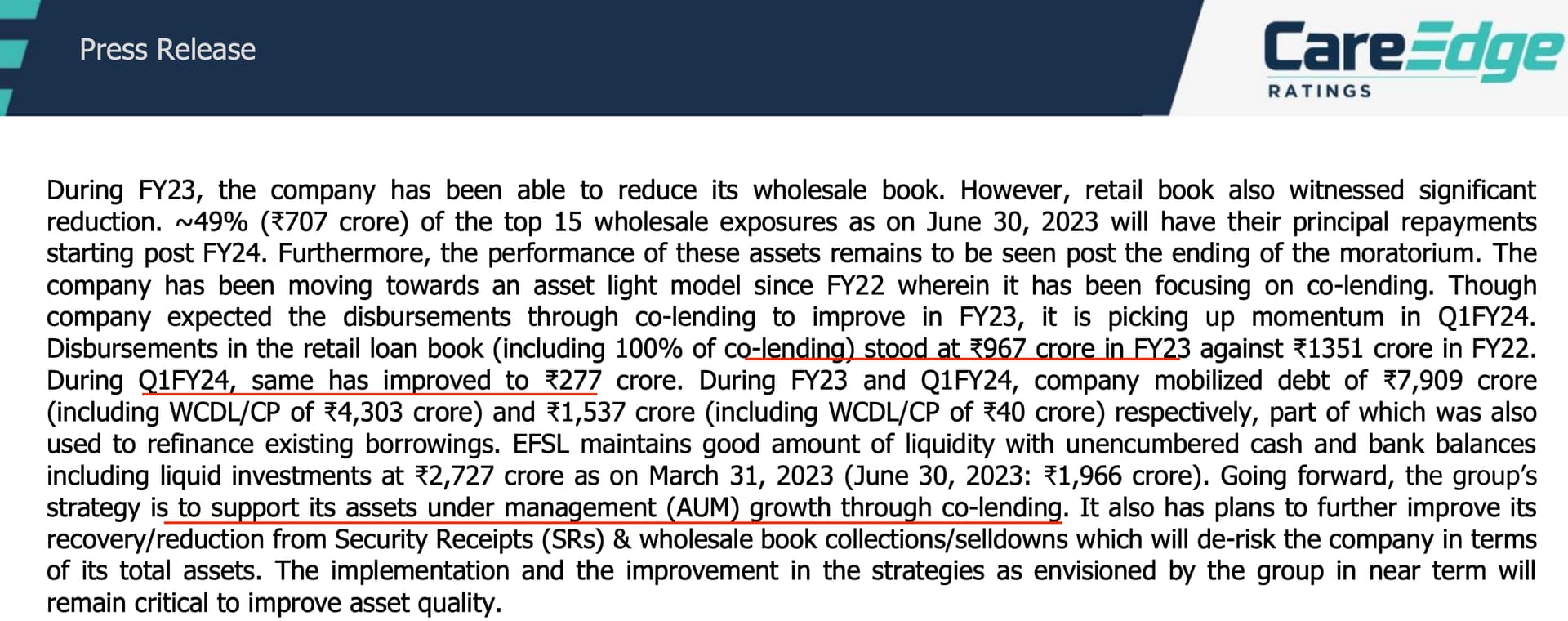

IN Credit space, Edel is lining up it ducks after a long delay. ECL finance pioneered Co-Lending, but in the 2/3 years, they struggled to scale the business as other NBFCs forged ahead.

IN Q1, they co-lend 290 cr, and in Q2, they lend more or less the same. Co-lending is a high ROE business where the banks’s equity is not tied up fully, and they earn good revenue with less capital. Also, the lending standard is stringent as banks check/vouch for the credit before taking it on their book. It is good to see that they are talking about co-lending, as it is one of the critical factors. This is what Care published few months back.

Insurance- Looks like they pushed profitability by one more year - FY27

Note; Invested and views are biased.

3 Likes

Alternatives

- Aim to earn 2-3% per annum on AUM (Fees+ Carry)

- The hurdle rate is 8%. Anything earned above that is part of carry income.

- It takes around three years to deploy funds in full amount.

- Aim to deploy around 10-12000 cr per annum

Co-lending

- AIM for FY26- If we get a disbursement of 5000-6000 cr per annum, we can generate 150-200 cr PAT. The current disbursement number is 1500. Last year, it was half of that.

→ This means FY24- 2000 cr/FY25-3500/FY25-5000 (my guesstimate)- This shall report more than 50 cr PAT in FY24 (assuming that number triples to 150 cr), as Mr Shah said in the call. - 15-20 ROE is possible

- Co-lending- Offer 80% to banks. Customers get a lower rate (bank’s rate for 80%) and NBFC’s effective rate of 20%. So, Customers get lower rates, banks get better business, and NBFCs get better ROE.

- It is 50% better from a returns point of view, but you have to work hard 200%

- It is still evolving and may take another couple of years to reach maturity.

MSME

- Current annual disbursement -

MSMS - 1000 cr (Fy26 target 6000 cr)

Housing - 1500 cr (Fy26 target 6000 cr)

Total - 2500/3000 cr per annum

Aiming for annual disbursement of 11,000 to 12,000 cr within the next 2 years

Housing

- Current equity is 800. Retained earnings will take it to around 1000 cr over the next 2 years.

- No plan to inject additional equity in HF

- If we get a disbursement of 5000-6000 cr per annum, we can generate 150-200 cr PAT. The current disbursement number is 1,500. Last year it was half of that

Other

- Nuvama stake, which is valued at 1400/1500 cr (based on CMP) shall be sold in a couple of years

- Value Creation priorities

- MF/AIF

- Credit business profitability based on co-lending

- Insurances

- Expect to communicate to shareholders the next set of value creation plans in the next 3/4 quarters

- Do not expect any impairment to the wholesale book. They can see SR if needed, and there is a good secondary market for it

- As the economy is improving, real estate is improving, recoveries are happening in SR

Note: Invested

6 Likes

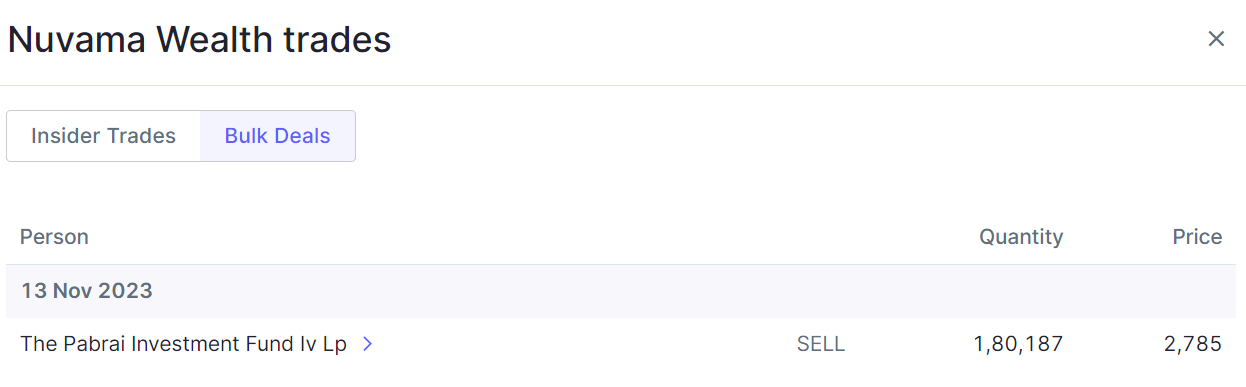

Pabrai funds sold Nuvama shares on 13th Nov

All were saying he was interested in wealth management business- but I think as valuation were high and as a value investor he exited.

3 Likes

I got one share of Edelweiss for free when I applied for their bonds … dont know what decimal point will be the amount due to me ?

Good read

7 Likes

I looked at HDFC AMC and compared it to nuvama. Sales are almost equivalent, profits are almost the same but market has given a higher valuation to HDFC AMC. In addition Nuvama has 9k cr of cash equivalents and 6k of debt. Whereas HDFC AMC has 5cr of cash equvalents and 0 debt. Nuvama seems better bet according to me and i think a fair valuation would be 30000 - 35000 cr. Am i missing any facet? Do share ur views on it

You cannot compare a wealth management firm with an AMC. Wealth/broking are businesses which fluctuate wildly with the markets. Also, as the networth requirement is not high, the entry barriers in wealth business is low. An AMC, particularly with the reputation of HDFC, will continuously get fresh assets through SIPs and in bulk, also they will keep earning AMC fees irrespective of performance. A large AMC like HDFC AMC has a huge moat in terms of track record and brand

5 Likes

While I agree with entry barrier but if you see developed market like US. Only the bigger gets bigger in this business and customer retention is 99% . So don’t you think if the market penetration from current 2-3% - 5-6% in this segment along with 4 trillion to 5 trillion economy makes this space more attractive.

I guess debt free company can get to this valuation of 30k cr, else if you see Motilal Oswal is also trading much lower to its performance

2 Likes

AIF circular by RBI, what is the impact on Edelweiss?

They have not come back to the market yet about impact. I heard they are one of the players who used AIF funds to park their NPA.

As they have AIF company (100%) I do not think they divest it (fully) so the other options for them is to provided 100%. I think they can absorb few hundred cr of provisions but anything more than 400-500 cr, they may have to sell down part of Nuvama stake (valued around 1700-1800 cr at CMP)

2 Likes

As per what I have read they need to divest in 30 days, this will be a s**t storm for Edelweiss.

1 Like

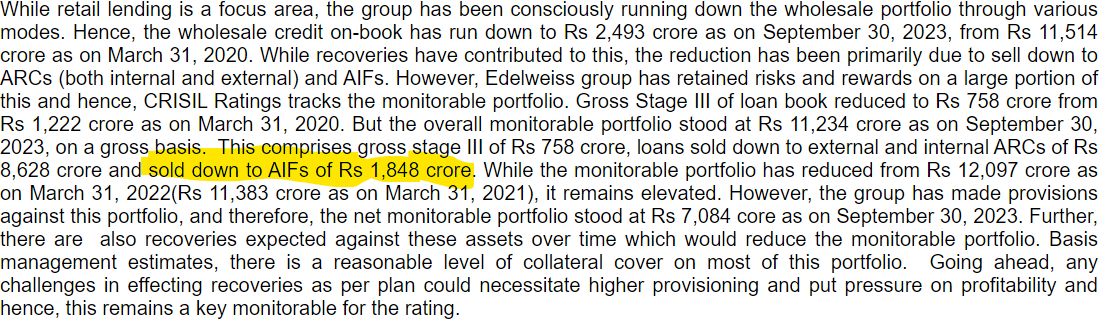

well spotted @Omkar11. Very likely they have to provide for 1848 cr of NPA if we go by what Piramal Enterprises and IIFL Finance has provided for.

1 Like

Sale to AIFs is different from investment in AIFs. As per my understanding, there is no issue with sale of loans to AIFs. The problem comes if Edelweiss had invested in AIFs/ if they accepted units in AIFs as consideration instead of taking money for the sale of loans

Hii, @camadhav you can go through the Moneycontrol article attached here Piramal, Edelweiss & other NBFCs under scanner as RBI cracks whip on loan evergreening via AIFs; provisions to rise

AIF as a % of investments is 11.4 %

Yes we don’t know how much of this AIF has invested in the company’s debtor company

@paragbharambe piramal enterprise and iifl fin has enough capital to support ![]()

Edelweiss needs capital for insurance businesses, debt reduction, and support credit business

Can’t say much let’s see what management do

Disclaimer - no recommendation for buy or sell