It is nice to see some uptick in SP after a very long time. Feeling optimistic after a recent management re-eval even though it is pretty generous.

1 Like

Edelweiss has increased the stake to Life insurance JV to 75%.

The rights issue of ETLI, the Company has been allotted 25,00,00,000 equity shares of the face value of Rs. 10 each for a consideration of

Rs. 250 crores. Consequently, the shareholding of the Company in ETLI has

gone up from 66% to 75.08%

Looks like Edel will end up owning the JV as Tokiyo Marine may not want to play significant role here as they could not raise the stake beyond 50%.

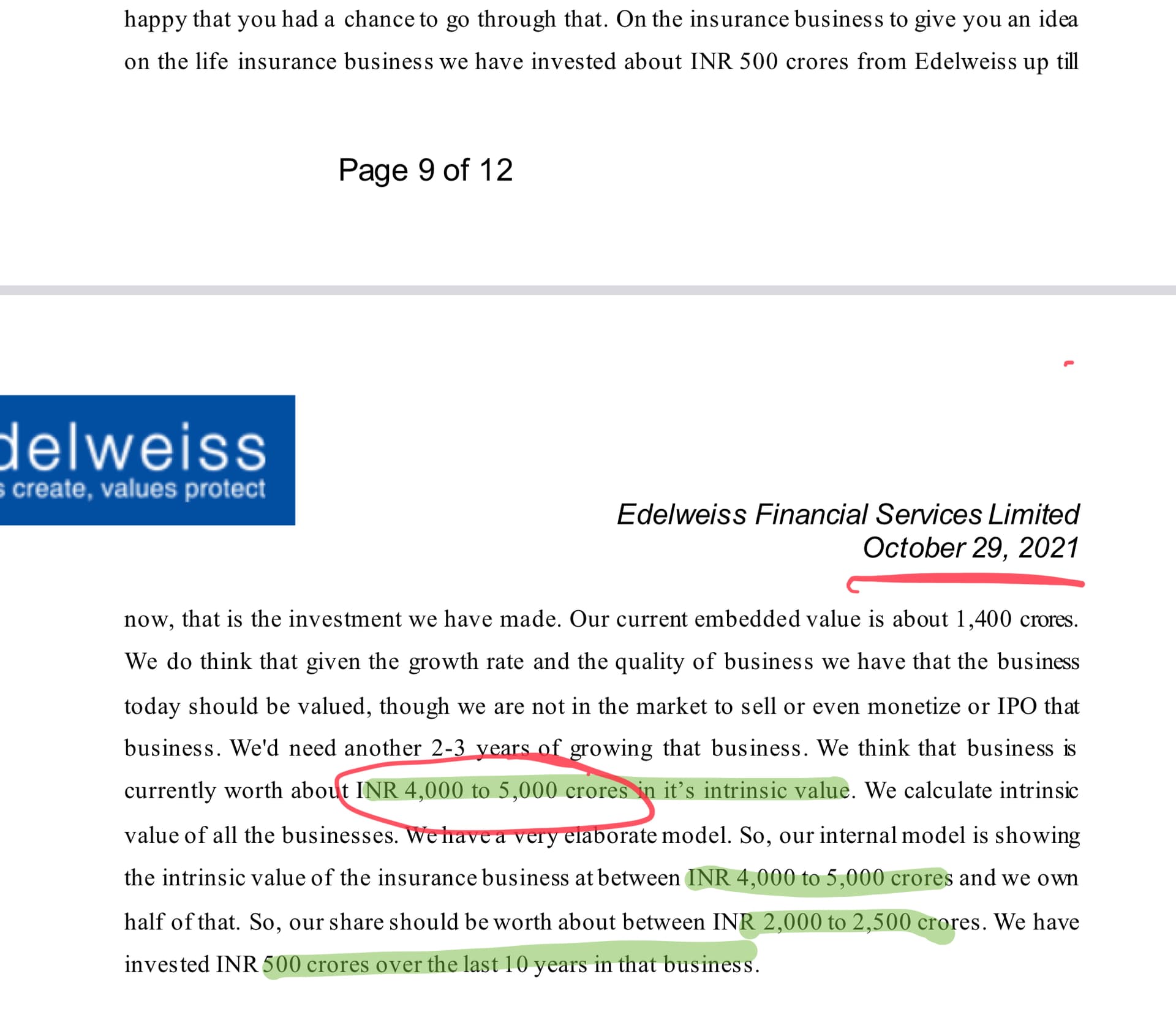

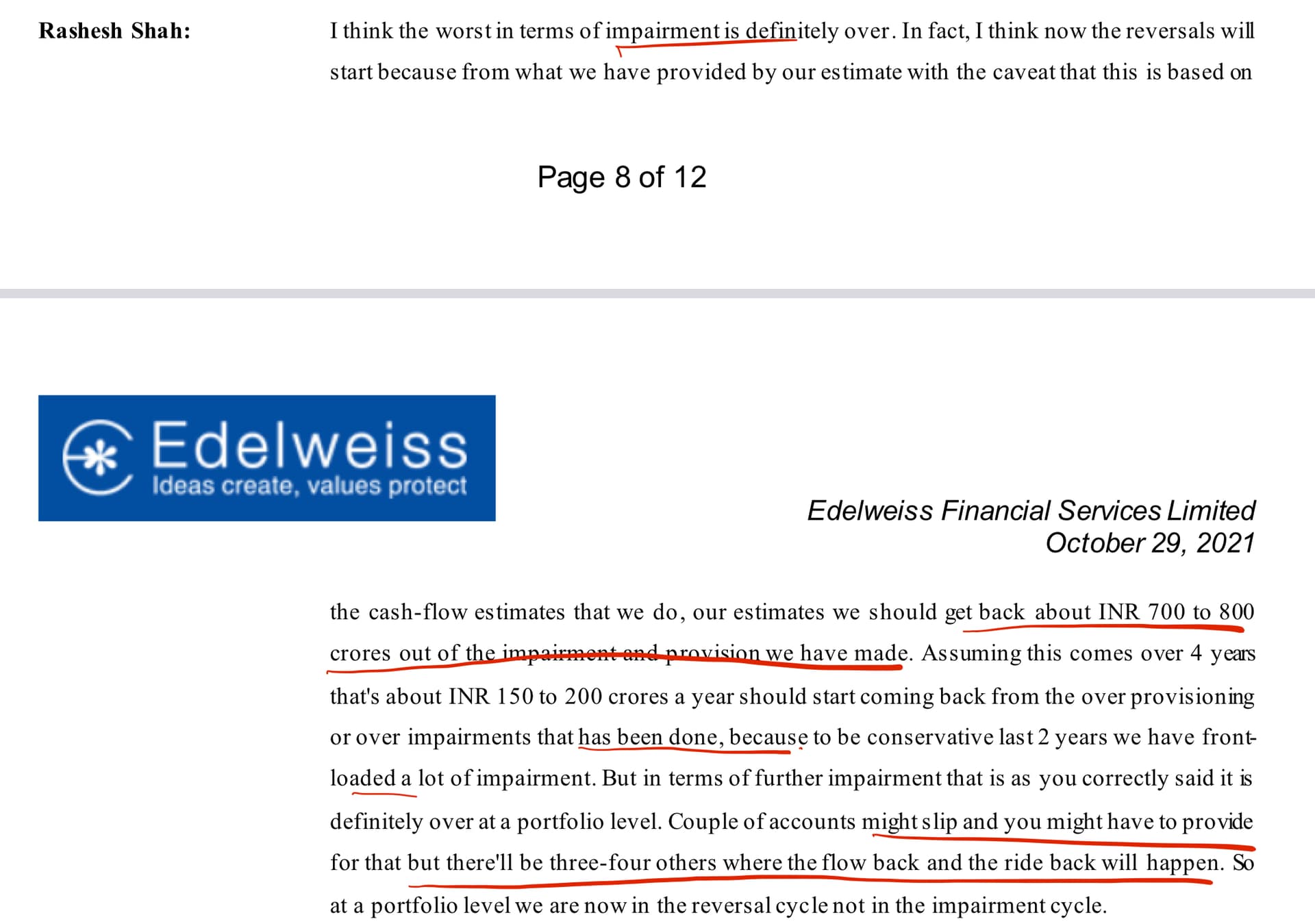

9% stake exchange at 250 cr, means Life insurance business is valued around 2500cr, far lower than Rasesh shah quoted intrinsic value of 5000 cr couple of quarters back.

This also means they will report more losses from Life insurance business going forward.

4 Likes

The negativity on the thread doesn’t smell right. Many of the above users have posted only about Edelweiss (90%+ posts) and all of it is negative.

The above post also reports wrong facts. The range for intrinsic value given by management was 3,800 cr - 5,700 cr.

It is exciting to see - Edelweiss owning more of their businesses!

Disclosure: Invested, biased. Holding for 10 years.

I have updated quotes from Management in Oct 21 where they have mentioned value around 5000. The intention of the post was not to be exact but give an indication

I agree the tone is negative, but there is not much positive happening in Edelweiss recently so it was obvious IMO that there will be negative tone.

If I see last 10 years return, they are 5% CAGR. Would be interesting to know what made you invested in Edelweiss for so long?

2 Likes

In AGM they have indicated that there can be a stake sale in life insurance business so now we can assume it is a temporary aquisition can go up to 100% and then sale stake at premium so to be conservative we should assume 45 - 60% stake of edelweiss only

And in housing finance we can see entire stake sale (my guess)as it is not growing if you go by numbers and management is also focus on scaling asset management and insurance businesses

Happy if they use the capital to scale general insurance business to 10000 - 15000cr or give some projections

2 Likes

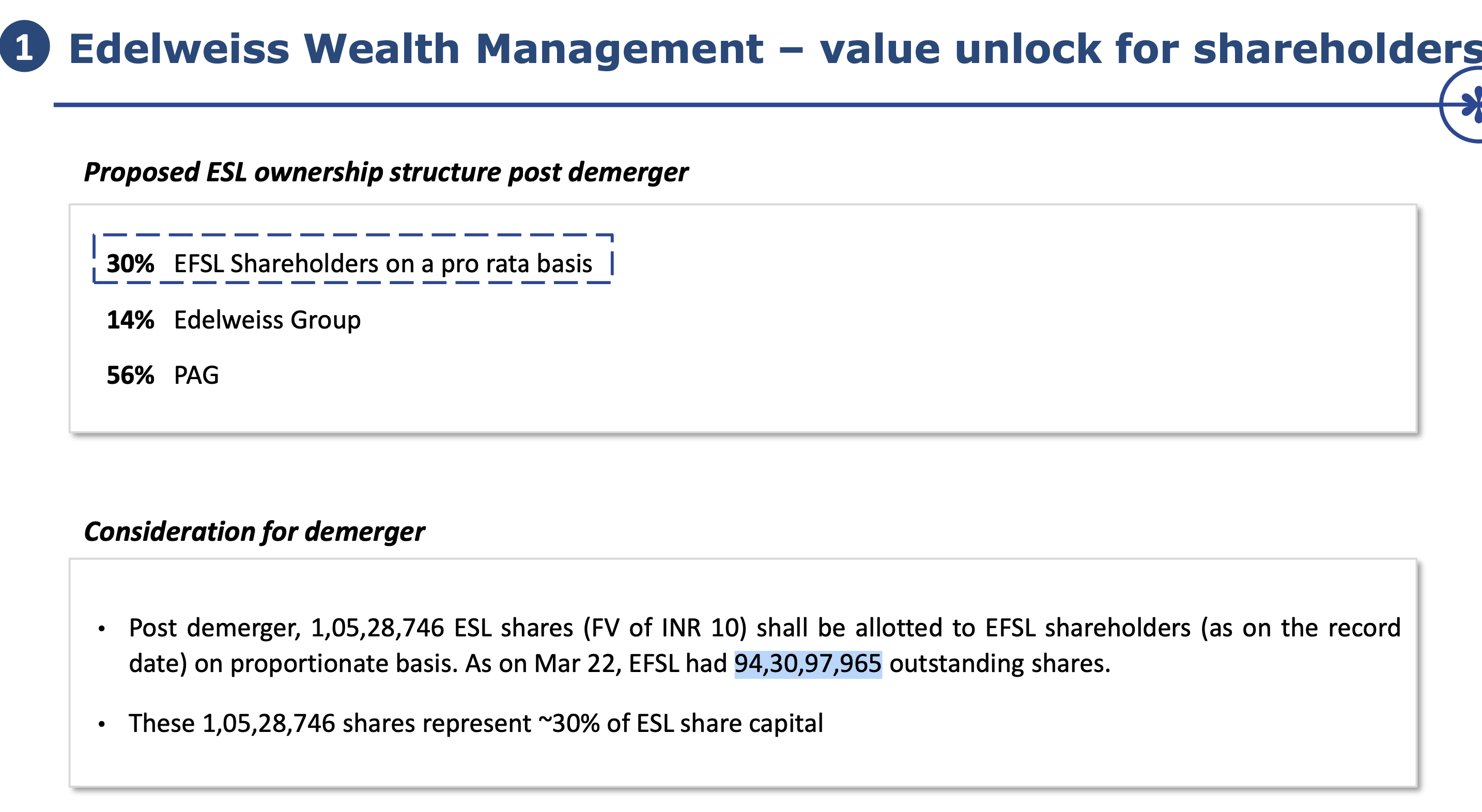

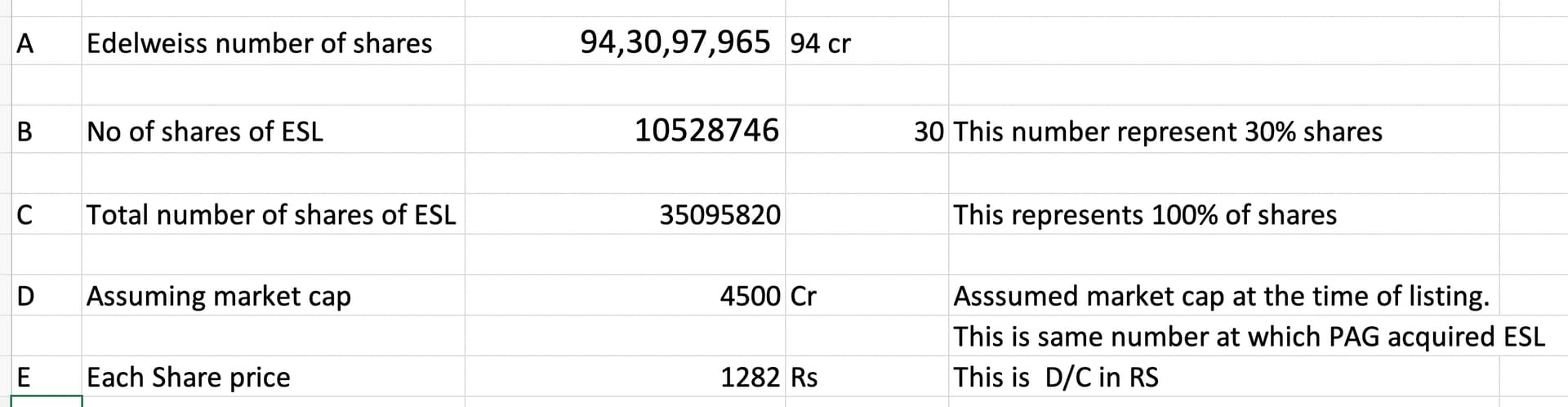

I am trying to calculate value of one share price of Wealth business with following assumption.

I am assuming market cap of 4500 once listed. This is the same number at which PAG acquired the business in June 2020. I am sure they have made investments in the business but the profitability has not improved. So I am assuming no changes in the valuation over the two years.

The shareholding pattern of ESL (Wealth business)

ESL Valuations

So assuming 4500cr market cap, each share may be listed around Rs 1282 . Of this number of very depending upon when it happens, but I thought of making it clear to myself and others.

Please feel free to point any issues with above calculation.

5 Likes

Can any one suggest about how much shares of ESL for 1 EFSL share post demerger ?

Yes they are conservative.

IN AGM this is the value they Edelweiss share of 20,000 cr, but the market value based on CMP of 60 is around 5500cr. So market is giving only 25% of value what management thinks their worth. So I would rather be conservative rather than aggressive. Hence I think the price around 1300 cr represent approximate price at which Edel sold to PAG in June 2020.

In a meantime , if they delivered good profitability in next few quarters it will be bonus, but I would not put too much hope into that at this point.

Lets say if I buy 10000 shares of EFSL @ CMP ~ 60 Rs. I am investing 600000 Rs and after demerger as per calc.

We 'll get 10000/9 = 1110 shares if ESL.

Value of one stock is 2100 Rs then directly it comes to 2100 * 11100 = 23,31,300 Rs

Is it possible by investing only 6 lakhs now you will get 23 lakhs and what will happen to EFSL stock price after demerger ?

Is there any calculation mistake?

You will get 111 shares in stead of 1110 shares

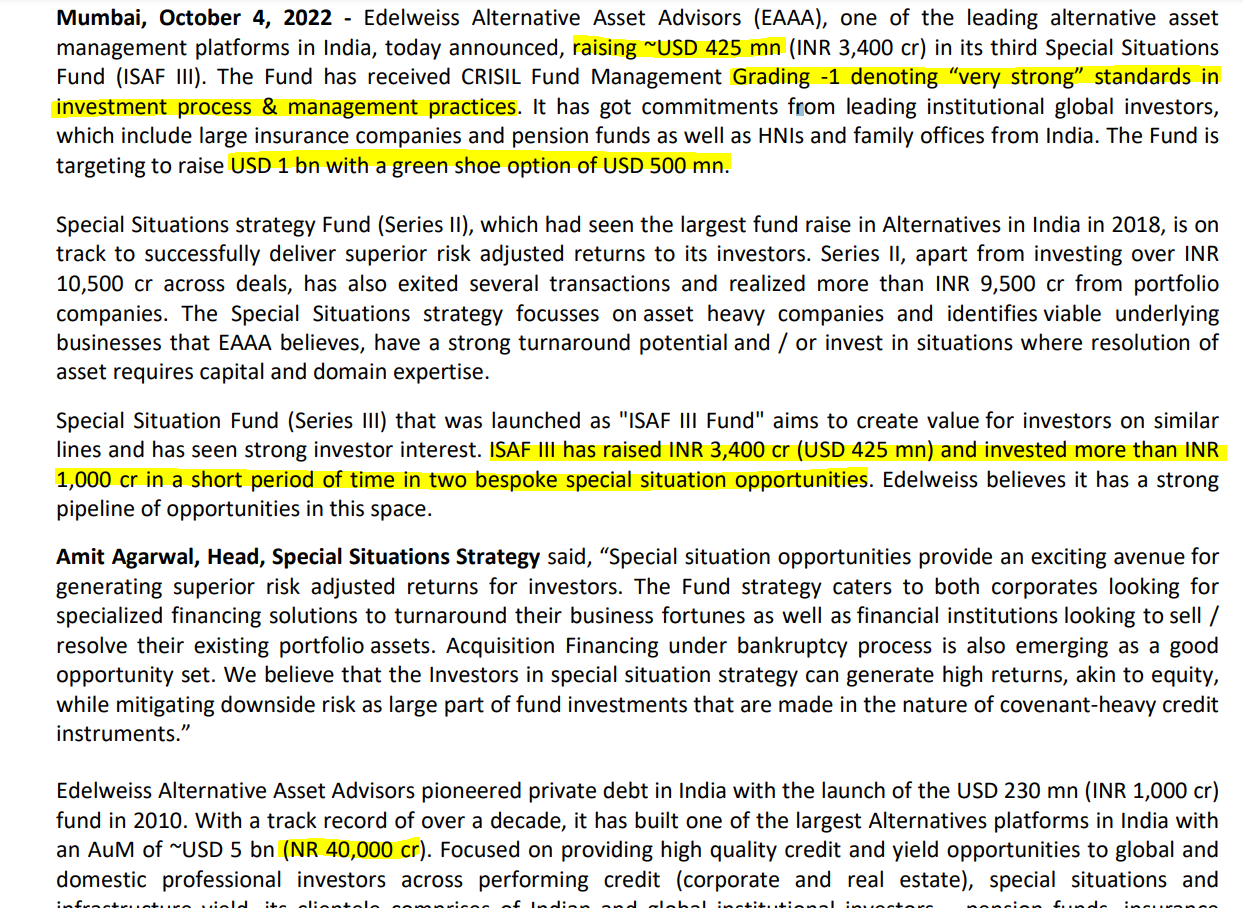

Edelweiss has raised $450 million through ESAF III funds.

Key Points from below:

- The funds has raised $425 million but they are targeting to raise $1 billion + $500 million option

- Already deployed 1000 cr. Looks like this quarters they will have good deployments across this as well as earlier raised money. This should auger well for AIF fees income in coming quarters.

- AUM of 40,000 cr. If the ISAF 3 raised unto billion, their AUM will near 45,000 (approx.), which is inline with what management has been saying so far.

I think AIF is where the action is as far as Edelweiss is concerned.

2 Likes

Considering face value ?

As per agm transcript to reduce debt edelweiss planning to reduce further stake of 14% in wealth management…Is my understanding correct?

I have deleted my previous post it can create speculation or anyone misinterpret it

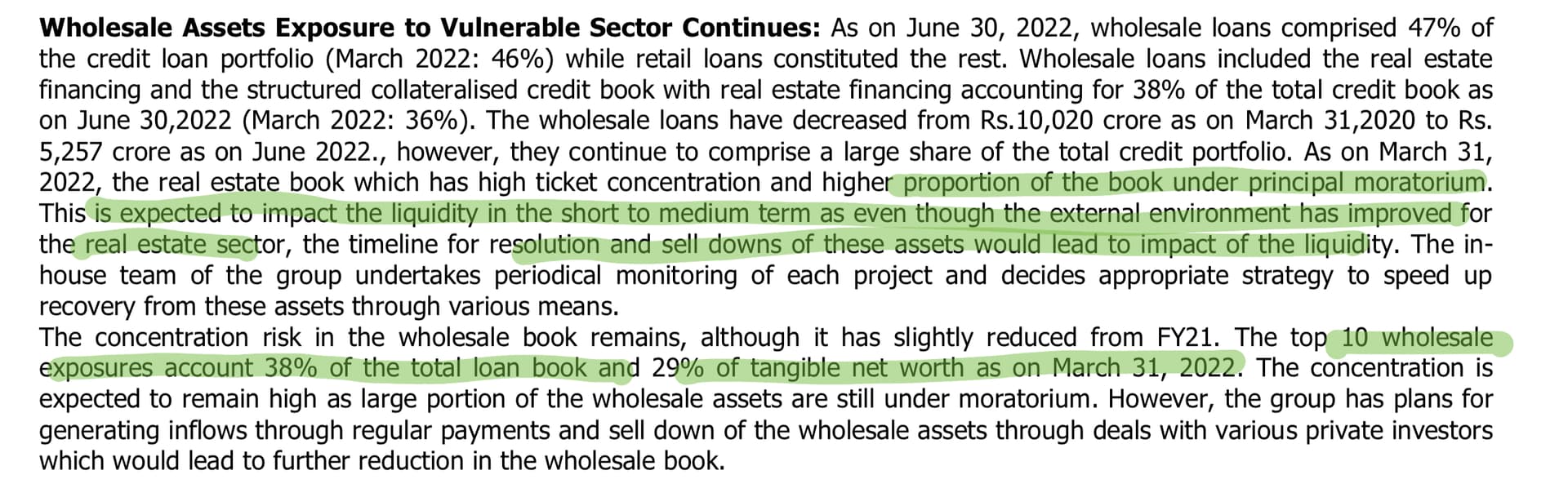

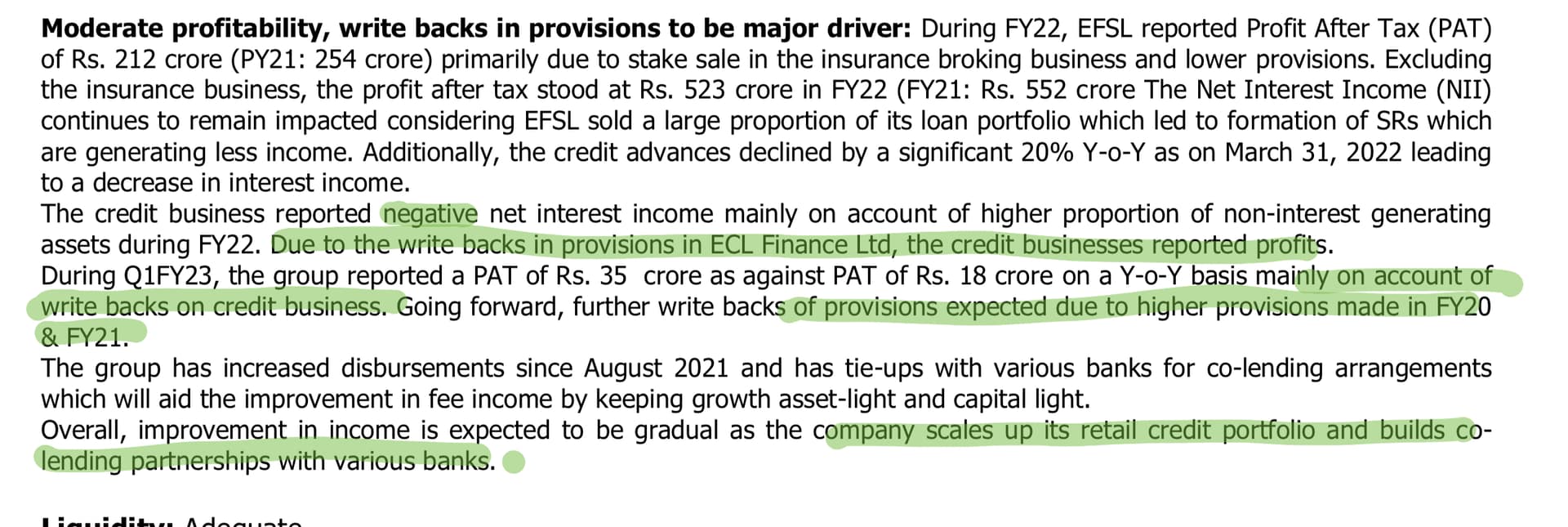

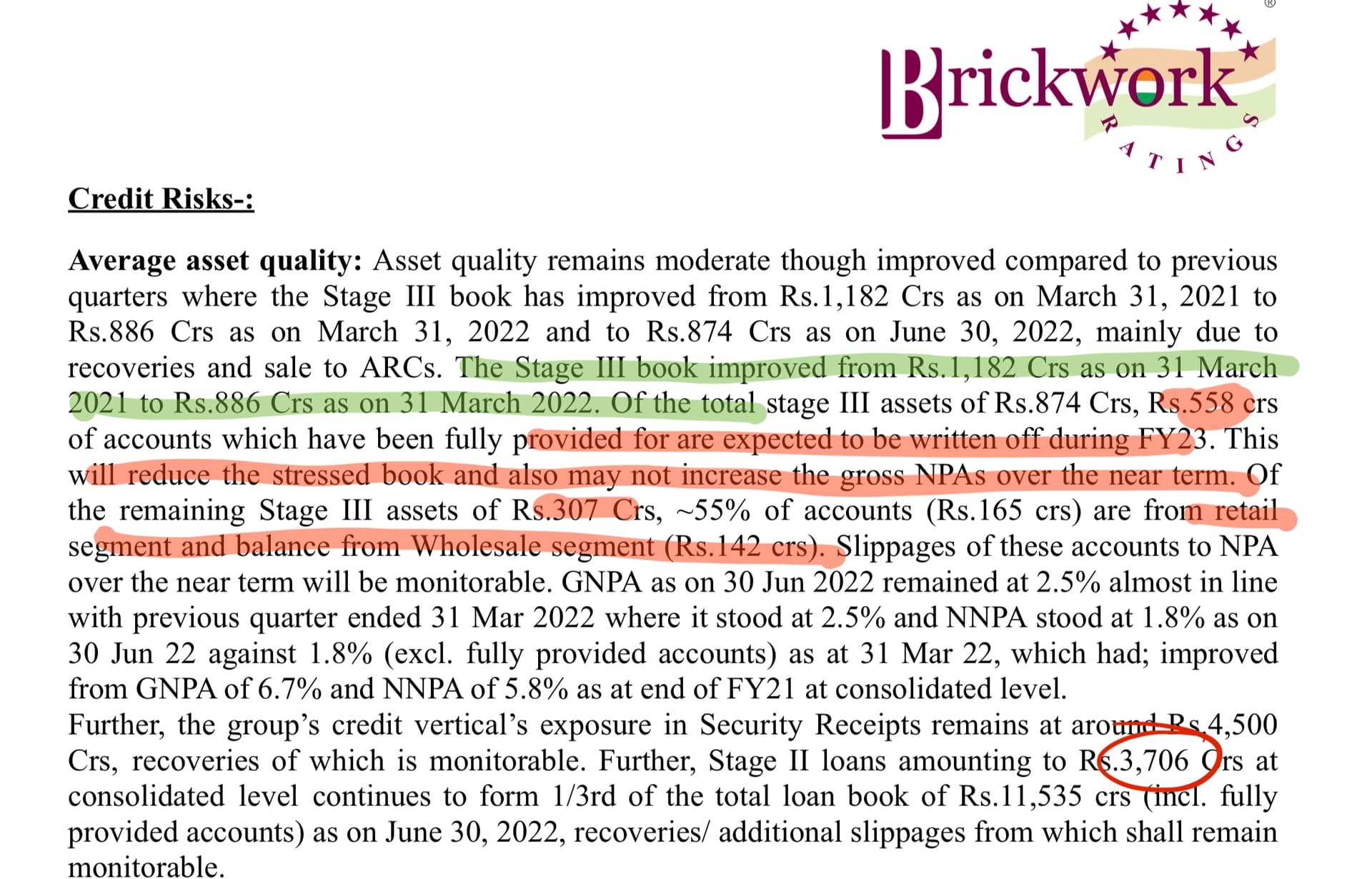

Brickwork and Care have come up with a Rating for EFSL. It is very interesting to read.

I am trying to connect a few dots here.

They have provided information which is very hard to get from the management, and a lot of time, even if management provides , they spin the number so that it does not come as negative. However, both rating agencies have mainly focused on the negative part, as that is the intention of the rating which is good from investor’s point of view (management always provide positive spin so it is better to understand other side).

The rating is mainly focused on Credit Business (NBFC) and has given very insightful information (to me at least). It seems the rating is based on their audited FY22 results but it looks like Care received some information which is not yet in the public domain.

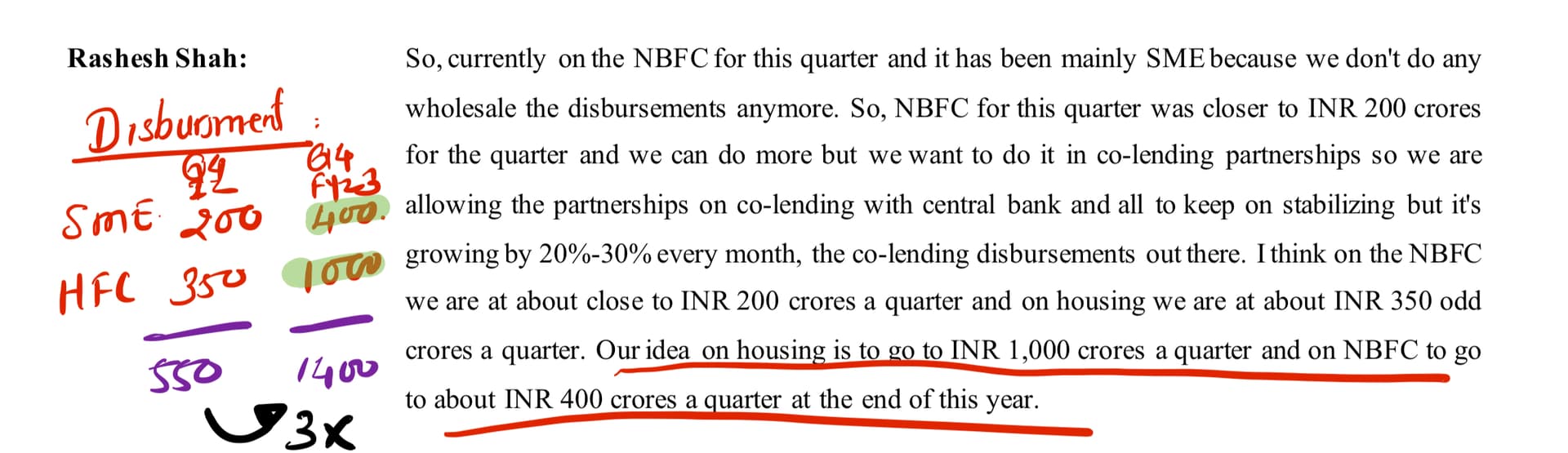

About Whole sale

Out of the wholesale book if 8580 cr, the loan book of 4500 cr is on with ARC. ARC has provided a security receipt for this amount and EFLS received a small payment initially. As and when recoveries happen, the loan amount with flow thrown P&L. Flow back on the written amount will gather pace as per Ramesh Shah in an earlier con call, and this is the main reason for Q1 profitability for NBFC.

The downside of SR Is this amount does not earn any interest for them as it is not directly on their book anymore. As a result, their Interest income is and continues to lower. I think most of the NBFC profit will be write back for at least 3/4 quarters until retail segment pick.

Both reports highlighted that EFSL sees a future in co-lending, which is what management has been saying for last 3/4 years. Other NBFCs such as IIFL Finance, and Capri has picked up loan disbursement in this segment, but EFSL is yet to show meaningful growth.

In Q4-FY22, ESFL has disbursed 550 cr and by Q4-Fy23, they want to triple co-lending. This will be an important monitorable from rating’s point of view as as profitability point of view.

6 Likes

Q2 Con Call Notes - 10 Nov 2022

General

- Now, getting reading ready for growth and profitability in the next few years (saying it for some time now).

- The balance sheet is shrinking, but customer assets are increasing as we are focusing on advisory

- AIF- Invested 20k. Like to invest the remaining 20k in 2 to 2.5 years.

- Plan: Next 2/3 years focus on Asset Management, AIF. Currently no specific plan for further demergers.

Wholesale

- Credit business has started growing.

- We choose to take impairment first and do not expect more impairment in the wholesale book.

- Loans are getting repaid. Not doing any more disbursement as a result wholesale book is reducing.

- Based on the cash flow we are seeing, this book should zero in 3 to 3.5 years.

- Can we reduce wholesale in one go (8500 cr book)?

- PE/ARC funds want IRR of 18-20%. If we reduce the book to one shot, it will be fair expensive for us.

- It may cost us 1000 to 1500 cr .

- When we see cash flow visibility for the next 18 to 24 months, it is better to reduce the book organically.

- Out of 8500 books- 5000 cr is borrowing, and 3500 cr is equity.

- Real estate market is increasing, so we might see the upside.

- So far, we have 4000-5000 cr through AIF/Sales.

NBFC

- Housing Finance- We will work/consolidate in Co-Lending, affordable housing business mode strongly validated in the next four quarters. Then we will look for the next course of action.

AIF

- Most of the Private debt.

- Private credit started in India 3/4 years back, and we are a leader.

- Large space with many strategies.

- Deploying around $1 billion per year.

- Carry comes when your funds are 3/4/5 years old.

- Next year onwards, carry income shall start kicking in

- The way to analyze AIF

- How much is AUM?

- How is Fee paying AUM?

- What is the vintage of AUM?

Wealth

- Wealth Management- 28% growth- H1 profit 138. Q2 profit 84 cr.

- Expect NCLT approval in Feb and listing in around four weeks. So listing shall happen sometime in March.

- We operate to affluent ++ to Ultra HNI- Which gives us large number of clients

- Take a long gestation period business.

- Focus on building more comprehensive products. This allows more value to the client.

- We also have an investment banking business. Helps are promoter level. We also work with them on an aspiration level, as when they monetize their business, we help them in wealth management.

- Blesses with a sectoral tailwind.

- Stock of wealth composing 10 CAGR.

- Money which we manage shall safely grow by 18 to 20. Any other products which we launch or innovate, we do on top of that. AIM is to 22 to 25 AUM growth.

- 90% of the transition is done. Another two-month rest of the things shall be overs. This results in our costs going higher as it leads to duplication. This will fall off next year.

MF Business

- Investing in business and there was some MTM cost in H1 which have affected.

- We will continue to invest for another year. AUM gain is coming at P&L cost.

- We would like to continue focusing on AUM and customer addition.

- There is no plan for IPO for the next 2/3 years.

Life Insurance

- Some partnerships related to distribution (e.g Bank).

- IRDA has increased the number of partners banks can have from 3 to 9. So we would like to go in that direction. That will be value unlocking. It may take a year to unlock.

- Likely to be profitable by 2026 then we can think of listing.

- Embedded value breakeven - next four quarters.

- Accounting breakeven around 2026. Same for GI business.

- Do not need a partner for capital infusion. We have allocated capital for both insurance businesses for the next 3/4 years.

General Insurance

- Very competitive business.

- We are the first company in Asia to be cloud-native. We could do it because we were late entrant.

- Wait and watch for the next 2/3 years.

- Industry will grow 18 CAGR for 4-5 years

- That industry is getting disrupted very quickly

- Differentiator-

- Product innovation that meets customer needs. We may launch small products, which others may find not interesting.

- Customer experience

Note- Invested.

3 Likes

Few statements are common for all con call.

Earlier timeline was 2023 for profitable business.

2 Likes

Can anyone explain how delisting will get benefited to shareholders?

how much will be gain after delisting?

The idea is that once the business demerges, it will have its own capital allocation, own board, own corp governance etc.

Investors will get a better insight into the business quality through more metrics - and it will start to become a pure play on a specific theme or sector in the market.

And all of this should lead to better valuation and value unlock than it was by sitting inside the parent entity alongside 7-8 other businesses.

Look at Motherson (a little bit more complicated than a simple demerger) - where you got the domestic wiring harness business as a separate entity - this business MSWIL is a much better (static) business than the rest of Motherson Group - it has a ROCE of 60% for FY22, and currently trades at NTM P/E of 37x.

Fwiw, I sold MSWIL at 85-87, and have continued to (bag)hold SAMIL - which is more of a play on recovery of auto globally, capital allocation of the Sehgals, and improvement in existing businesses.

EWM has 2 businesses effectively - Wealth Mgmt and Investment Banking/Institutional Equities.

WM has longer-term stable cashflows, IB though is a little bit more lumpy and cyclical.

They’re expecting to grow at 20-25% for WM and I assume IB can through the cycle grow at nominal GDP (let’s say 12%)

WM can potentially trade a high valuation let’s say 20-25x.

IB usually trades at lower (look at JM Financial, MOSL - high single digit P/E - although they also have lending operations lumped in together)

I suspect they can generate 350-400cr of net profits by FY24/FY25 and operating leverage will start to kick in once a platform is established and the incremental margins are higher.

Slap a 20x multiple and that’s a valuation of 7500cr to 8000cr

(In AGM earlier, mgmt put an intrinsic value of 7500 to 9000cr today, I am assuming it’s worth 7500-8000 in 2yrs)

Edelweiss’ stake (44%) will be worth c. 3400cr.

The market cap of EDEL today is about 5650cr.

So I think it is clear that EDEL is a good value opp - but requires value unlock through demergers and the market will only realise value if capital allocation improves.

5 Likes