They do not do con call every quarters now a days. Instead they do it in alternate quarters.

When they do not do con call, that time they publish investor letter like this one.

They do not do con call every quarters now a days. Instead they do it in alternate quarters.

When they do not do con call, that time they publish investor letter like this one.

Just want to know the possibility is there or no

Currently the ARC business is under edelweiss financial services as a subsidiary I am aware of ARC business is not allowed to list on markets directly or do IPO but currently it is listed indirectly through EFSL In the same way can edelweiss put the ARC business in asset management business as a subsidiary while unlocking value(demerger or ipo)in asset management business when it happens so the both the businesses will get valuation on the earnings asset management business can act as a holding company

Pls someone ask the management in the AGM or concall

Some problems and issues I want management to act

For Insurance Business

1)management need to do agressive partnership with banks for Bancassurance as it gives presence and strong distribution mix

2) Any guidance for protection products mix and VNB margins

3) focusing on building trusted brand and transperancy as insurance is selling trust and also competition is heating up

Management should compare with top 3 or 5 private insurers not with industry(inefficient)

management should improve quality of disclosures like revenue mix distribution mix segment mix commentary guidance etc like peers eg Aditya Birla capital current Disclosures are very limited

they purposely compare themselves with industry rather than top 3.

Their insurance been loss making for more than decade now, whereas they hade been keep giving hope to investor that they will be profitable by 2020.

I highly doubt that it will perform beyond 2x, lets see.

Me thinking aloud.

I am highly invested in it, but now i am losing all hope, not because i got bored sitting in it but i am not seeing any progress in their business.

I think now i am regretting going heavy on it where acrysil was on my radar in compare to this company.

Now the situation is even if they split their business, i am not seeing its going more than 2x. So, it arise new question for me is that much research and patientce worth 2x. I think not.

I may have waited alot in edelweiss but just bcz i lost some time here, I am not gonna be victim of sunk cost fallacy.

Their insurance business is yet not seem to be profitable soon, ARC business is not giving profit like it used to give in their prime time.

mutual fund is yet to become substantial.

This is exactly what i used to think, turn around story is the toughest and financial business is not really business to make money.

I think to really reap the fruit it will take 4-5 years management also mention it in the concall they optimistic to maximize the value for shareholders in 4-5 years It can be a multi special situation opportunity

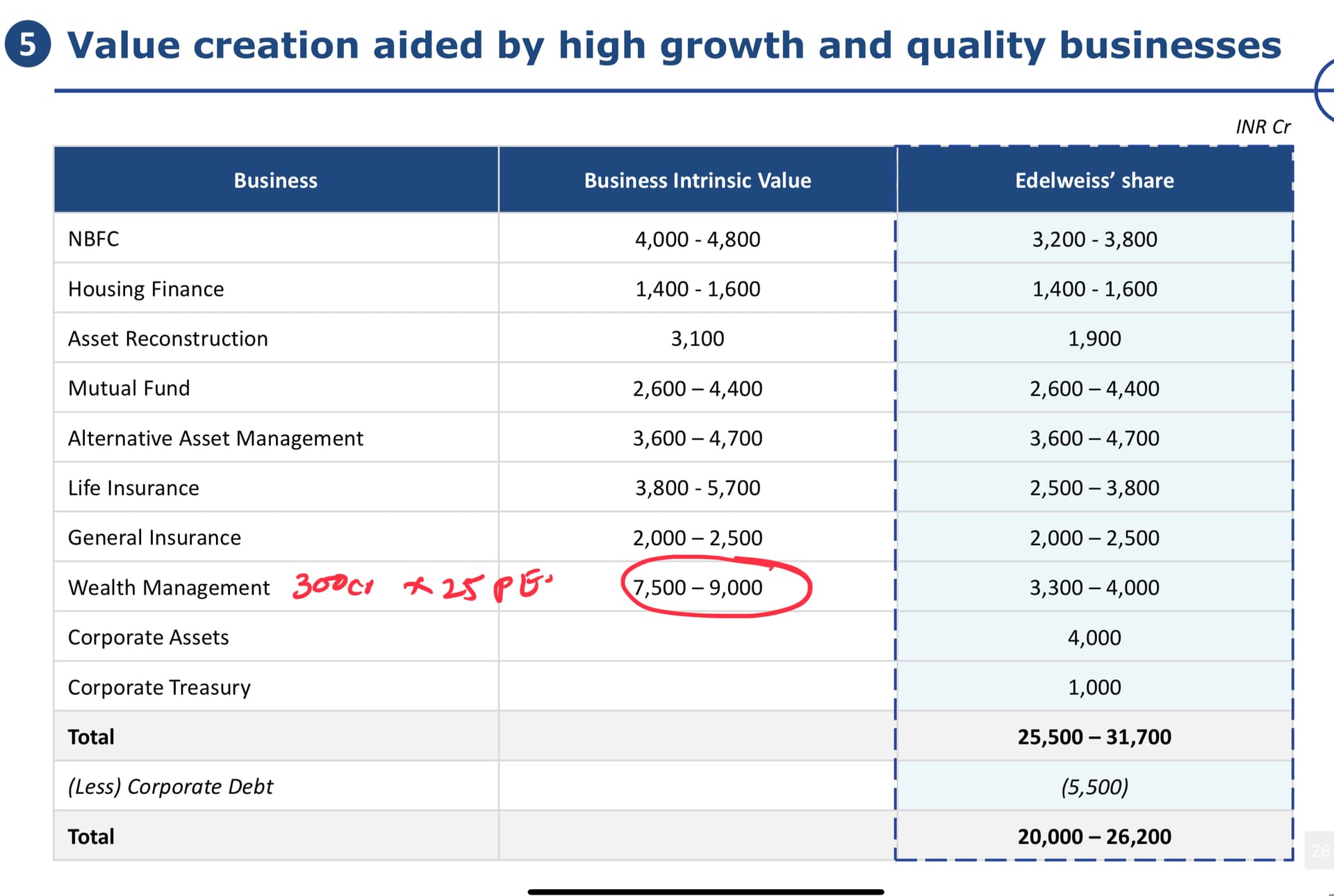

Current SOTP valuation

Nbfc business - 3900cr equity 0.8<1×p/b

1)Currently I don’t think they have started to lend still in the process to do tie ups

2)don’t know the capital allocation strategy the equity of nbfc is rising management was telling they will use this capital for other businesses now they have taken debt(135cr) for alternatives.

3) demerging their nbfc business can be a good option after wealth management business like the piramal did with it’s nbfc and pharma business but I think management want to show they can also create value in credit business too this will take time FY26 (guys tell your views on it)

For ARC Business

2511cr equity cdpq valued this business at ×5 p/b can be 12500cr

For asset management business- mutual fund/AIF currently AUM 124500cr 4% of Aum comes 4500 to 5000 cr so they have to earn 250cr to justify 20pe AIF carry income should add to it after march FY23 I think they will look to demerger or ipo this business in 2 years as carry income starts coming

For life insurance business

Current EV is 1550cr so to be conservative ×2.5 3800-3900cr 66% of edelweiss - 2500cr

It’s been 10+ years and only 2 Bancassurance partners fincare and CSB banks they really need more partners according to their investor relation they have focus to keep balance between profitability and growth

VNB margins and protection products to decide the valuations

Should focus on to create trustable brand and touchpoints

For general insurance

It is 1200 to 1500 cr business

In future they will partner with some other insurer as every general insurance company has done

it has started in 2018 but just 1 year before go digit have started their GP is 5200cr for FY 22 and edelweiss GP is if we go by current quarter GP 117cr so 117×4 468cr we can see insurance needs lot of capital to scale …in the news go digit ipo can come at a valuation of 30000 to 35000 cr at ×6 GP market leader ICICI Gl trades around ×3.7 edelweiss management should use the nbfc capital in insurance businesses and asset management to scale and ring fence their businesses they can create more value in this businesses credit business is not good option

For wealth management business - its approx valuation

March fy 23 demerger estimated 2200cr equity by then so 30% to public shareholders 14% to edelweiss group 56% promoter …2200cr -30% = 660cr ×4 p/b= 2600cr …in my opinion every shareholder can get 1 share for 6 to 8 EFSL (at face value 10rs of EFSL)

I think new management has start to make business predictable focus on recurring revenues like distribution income and management fees we can see scaling up like IIFL wealth as earlier PAT suddenly down due to market and shareholders were not aware why bcz of limited disclosures wealth management should do PAT 400cr not combine with securities business like IIFL WEALTH AND IIFL SECURITIES PAT is different

Housing finance 800cr equity 1>1.5 ×p/b can’t say much

Conclusion

Sometimes it feels like management is not aggressive and focus to scale multiple businesses insurance business as last bank partnership was done in 2019 Bancassurance gives presence can not be dependent on agents and digital and top insurers have started to sell direct leveraging their brands

Limited concalls, limited information guidance, disclosures for a company with 5 different businesses give much discomfort as investors are unaware what going to happen next quarter eg wealth management ( unaware of revenue mix and profit mix)

NBFC capital will be use for debt reduction suddenly FY 22 standalone balance sheet there is a debt

Management goes for growth but quality of growth and earnings are poor

Opportunity cost for reducing the wholesale book like they can use the capital to scale insurance business like go digit (feeling jealous 30000cr valuation😪)

Can management think to demerge the credit business? Imo market can reward this decision

Guys share your views

tracking from 1 year

Questions we should ask to management in AGM and concalls

Guys Any other questions pls suggest

for life insurance business

Data is from the annual reports from 2019 to 2022

they have limited themselves to 81000 policies and need to do at least a 10% increase every year

customers are in the same range not able to acquire new customers

persistency ratio is decreasing means miss selling is increasing

increase in advisors /agents not helping and not giving enough business they should try partnerships with banks and nbfcs and focus on creating their trustable brand and marketing

we should ask management about this

Edelweiss released AGM PPT today.

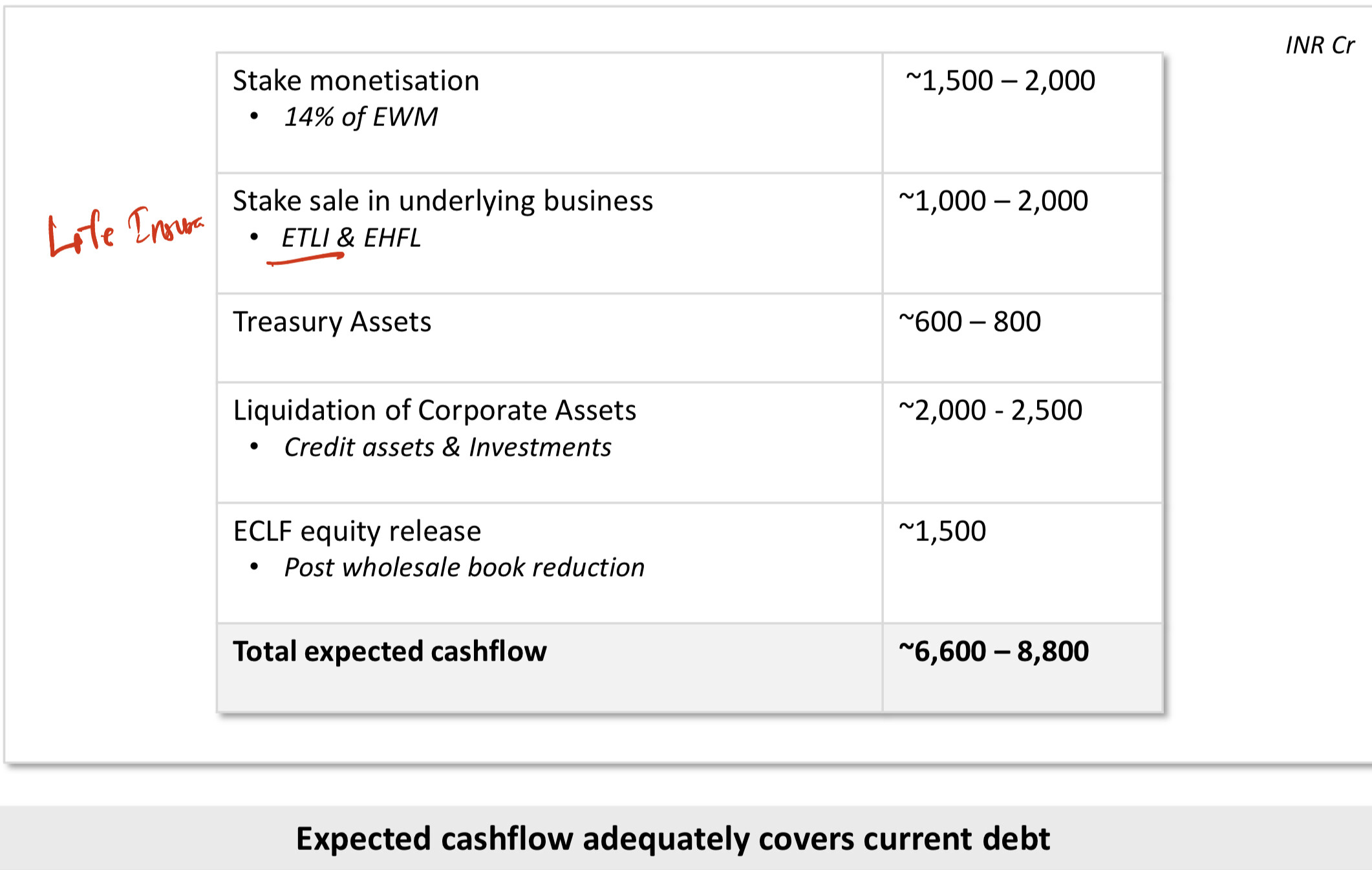

Looking to reduce debt as per this plan. They are massively deleveraging. They are talking about reducing debt and no mention about growth in the ppt.

Valuing Weath management business at 7500+ cr.

Market cap is 5600cr, and they say Intrinsic Value is 20-26k cr - they should be walking the talk and buying back stock hand over fist.

Interesting to see they will be selling stakes in Housing Finance and Life Insurance as well.

Is this the first time they’ve said this?

Someone asked them the same question in 2/3 con calls back, they said focus in on growth first and then buy back.

Currently they have two business which are loss making- Life Insurnace and GI. Combinely they generate loss of 300 cr. On top of that they need capital of around 250 cr per year.

Edelweiss does not have a excess cash. Also if they raised money and do a buy back, it will further strain their balance sheet. Their core business (all in total) are generating enough profit to float over on a consolidated basis, so they cannot afford to make any more mistake or they need bit of strenght for a rainy day. So I guess they would shy away from Buy back for a considerable amount of time.

I am glad that they are not thinking of selling a stake in AIF, which is ready to deliver good results going forward IMO.

Its becoming too complicated.

1)Yes the gave guidance why they wouldnt be buying back their share, main reason of it that they dont have money. They barely recovered 2 quarter back they were full of surprised expense.

I attended the AGM but as I was not preregister to ask questions( any one know how to preregister pls reply )

Speakers in the AGM we’re only praising the management and few with minor questions

Yes @gaurav_vimal it is looking complicated and some surprises

In may they disclosed they want to be debt free approx 2500cr by FY24 now the debt is 5500cr I don’t understand does anyone have knowledge above it pls explain

In 2016 cdpq buys stake in ARC at ×5 p/b valuations now they are giving it ×1.2 p/b valuation

Closing the ECFL think so look at IP and no info on retail credit business

Selling stake in Life insurance is not good they should not as growing 10+ years

Imo Showing the intrinsic value in IP they really want to show the market so they can get value push in valuation and raise some capital or QIP

I can be wrong but Imo they should look to demerge the credit business as market is giving the valuation for credit business there is a possibility market will rerate and then raise capital but (can’t be the option as they are degrowing and closing it )

Company need new DNA or professional management now

Thanks @Omkar11 for sharing your view. I think it is sad that you could not ask question in AGM. Based on what you described, it looks people were only praising them, which is not dissimlar to what happens to other AGM. I am not sure what someone should praise them. I doubt if any investor got any return if he has invested in the business for over a decade.

I think you should attend their con call (as you have very valid and pointed questions) for next quarters whenever it happens. There they would have to allow you to ask question. Ask due to what is happening with them, there is ample time to ask question as last 2 con calls finished within 45 min (they could go around 60 min if there are enough particiapant in the call).

Yes @paragbharambe looking forward to it currently asked same questions to investor relations team (keeping them busy for a while ![]() )let’s see not expecting good answers as always

)let’s see not expecting good answers as always

as far as I know they dont allow retail investors, you have to be atleast fund manager of any fun so they can take you seriously. Operator will put you on hold but you wouldnt be given a chance to ask questions.

Arent they about to zero their wholesale loan by 2022?