On a side note - what do people think of the change of name to Nuvama for the WM unit?

Did PAG want to avoid the Edelweiss tag?

3 Likes

Edelweiss has good value in Asset mgmt and Wealth mgmt…credit biz is an equity destroyer. ARC is avg economic characteristics. LI / GI biz are vanity businesses with no serious competitive advantages. Edelweiss as a group generates very poor return on equity so will not be highly valued anytime soon.

Trading 30% discount to its net worth.

Disc: Invested from lower levels. Planning to hold for 3 years till value discovery

2 Likes

In the 6/7 months of the year AUM has grown from 30,000 to 42300 cr with this money raise. Also looking at the announcement they seems to have deployed few hundred cr already, which is good news for AIF fee paying AUM.

Earlier they said they want to increase AUM 3X (from 30,000k) in next 5 year. They are already halfway mark there in 7 months, so they are likely to overshoot their earlier target hopefully sooner.

Note: Invested

2 Likes

Good state on ARC market expert.

They are raising money with higher interest. Dont know whether they will earn above the interest or not. This is concerning.

I do not think they have any alternatives. Core profitability is not improving, and they have increased their stake in loss making subsidiaries. Until NBFC profitability improves, which is unlikely to happen in hurry, their credit rating wont improve, which in turn will not reduce their borrowing cost.

In next 4 to 6 quarter, they can sell 25% stake in life insurance or general insurance as they mentioned in the con call. This may give them some respite, but overall market is weary about the uncertainty

1 Like

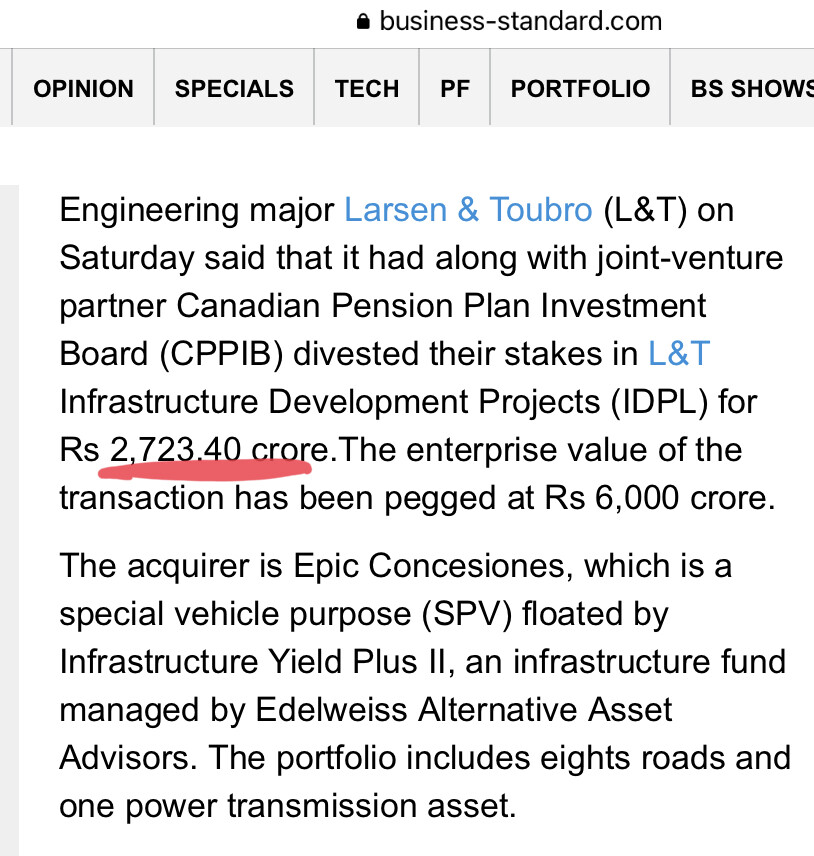

Edelweiss Alternatives backed platform signs agreement to acquire L&T Infrastructure

Development Projects Limited for 6000Cr. L&T Infrastructure Development Projects is not profitable and 1775Cr debt and 6327Cr borrowings.

IDPL annual report: https://corpwebstorage.blob.core.windows.net/media/47131/idpl-annual-report-2022.pdf [Page 44 - Assets]

2 Likes

Edelweiss is paying around 2700 cr for this transaction as per this report.

Rest of the money shall be part of debt. This amount shall bring in around 45 cr of additional revenue to EAA (AIF fund with management fee of 1.5%) from next year onwards (assuming this transaction closes in FY23).

Will Edelweiss take more debt to pay this amount?

No, as per BSE report 2,700Cr is the total revenue. “Following this acquisition, the infrastructure platform will scale up to 26 assets with cumulative annual revenue of nearly INR 2,700 cr.”

1 Like

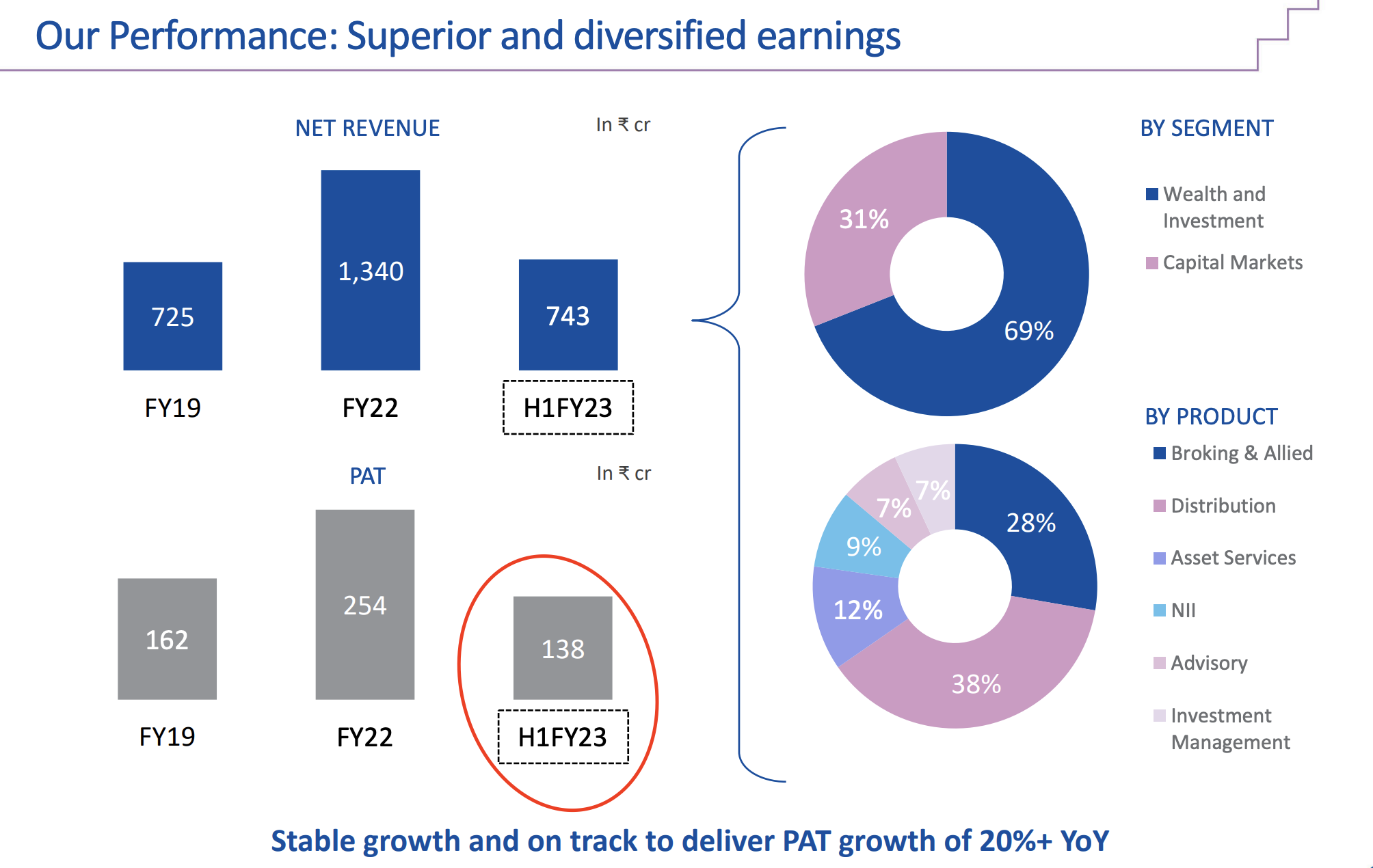

- Personal AUM growth from 60,000 to 1 lakh cr.

- Branch footprint to expand from 69 to 100 by FY24 (next 15 months)

- Current wealth manager 900. Plans to add 300/400 wealth manager every year

2 Likes

Any update on demerger date?

https://www.nuvamawealth.com/ web is ready

1 Like

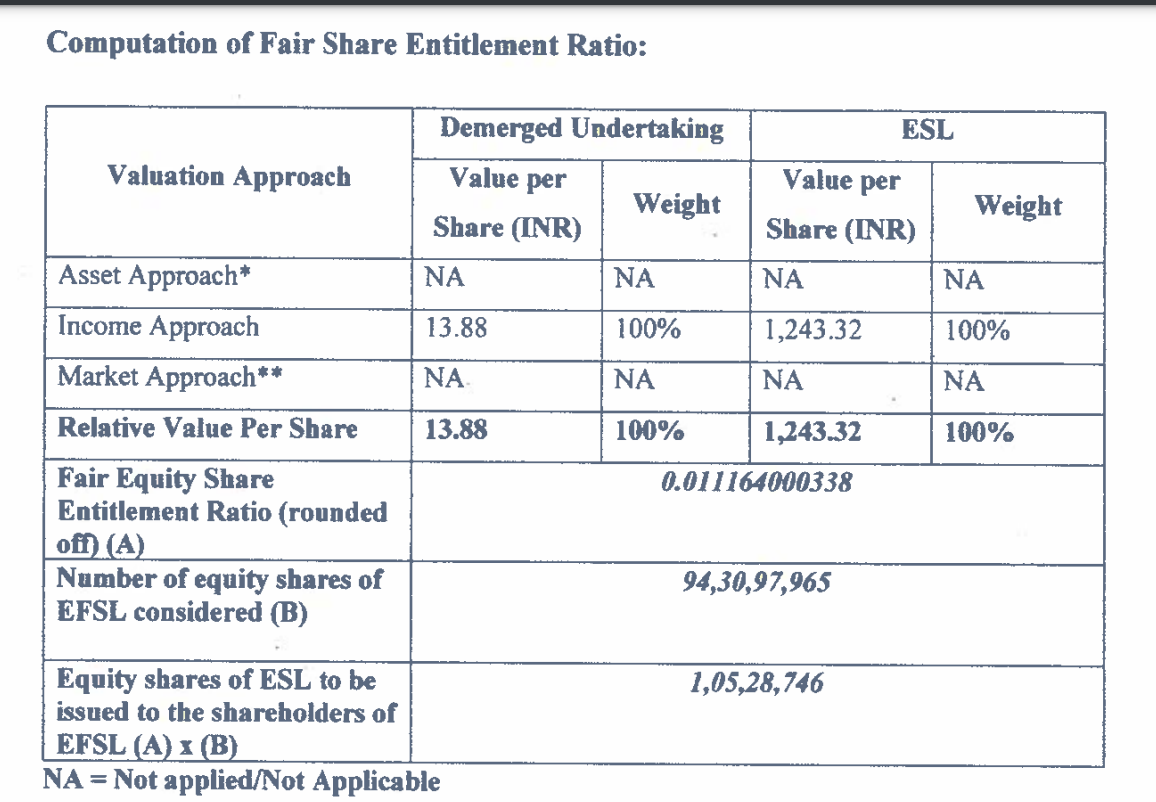

Demerged Company Details:

How will be the share entitlement ratio?

Hear is the calculation of listing price with 2021 Mar valuation:

PAG acquired 61.5% stake in Edelweiss Wealth Management(EWM) for ₹2,366Cr

In 2021 Mar EWM valuation was : 2366Cr*100/61.5 = 3847Cr

Total number of Nuvama(EWM) shares: 3,50,48,208

3847Cr/3,50,48,208 = 1097Rs

Total public shares in Edelweiss: 63,54,16,725

Total public shares in Nuvama: 65,92,528

Nuvama share per each Edelweiss share = 65,92,528/63,54,16,725 = 0.01

Edelweiss still hold 13.75 Nuvama after delisting through:

Edel Finance Company: 5.23%

ECap Equities: 8.52%

Check page 36 in: https://www.bseindia.com/xml-data/corpfiling/AttachLive/9e5bcf5e-8b5c-404c-b2a2-29cb3586d1d6.pdf

1 Like

Thanks @maulik_dadhania for sharing the link.

As per the documents, I am not able to tie the loose end.

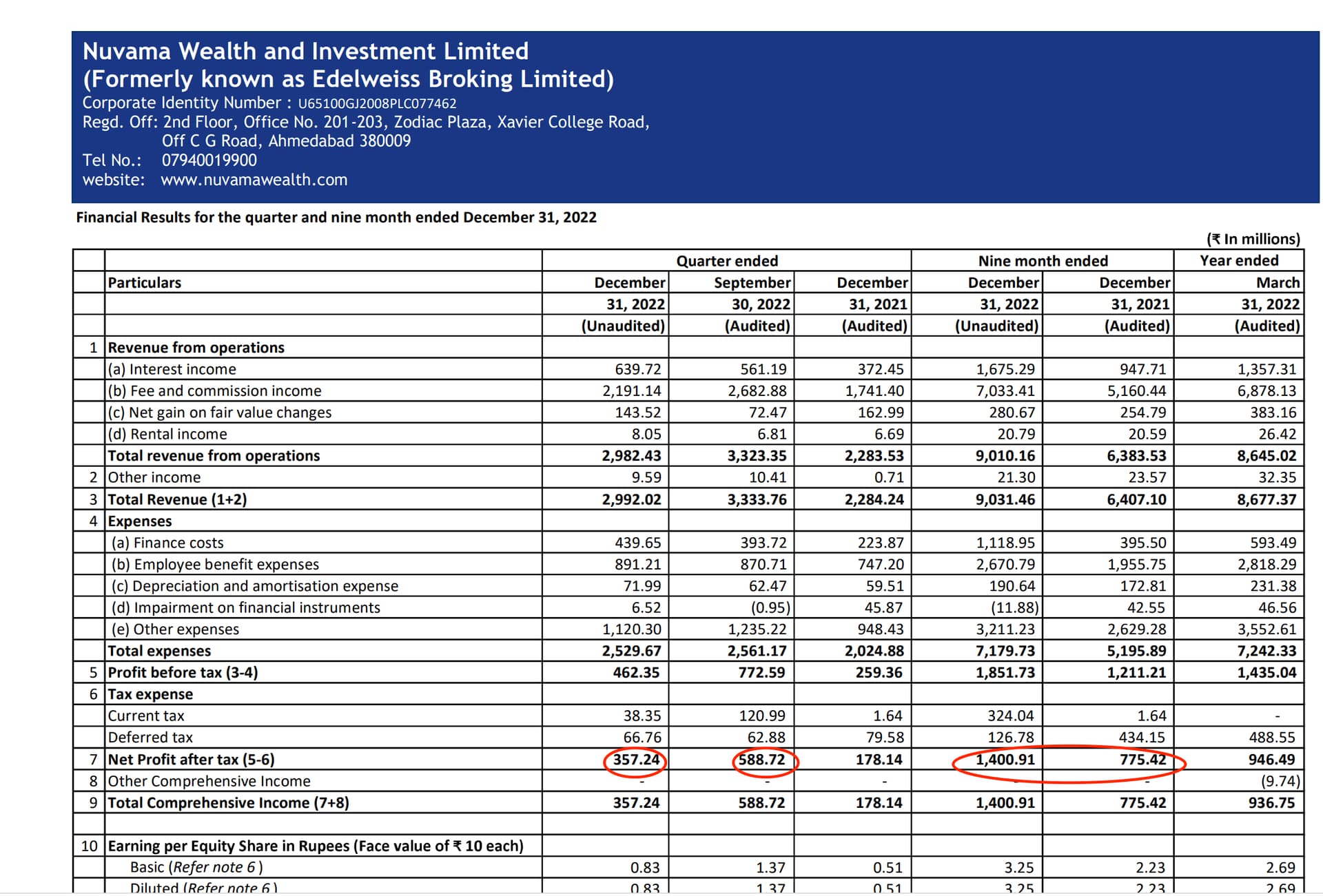

As per this document 9 months PAT is 140.

But as per Q2 PPT of wealth management H1 PAT is 138 cr.

Not sure what I am missing…

Same here. I am also confused. But as per PAG valuation, I don’t think they have paid 2366Cr only for 100Cr revenue and 15Cr profit. Also, debt-equity ratio is 3.24.

If we consider listing price of 980₹ then mcap will be around = 1031.8 Cr which is quite less as compare to PAG stake acquisition.

Nuvama Wealth Management Limited.pdf (398.8 KB)

1 Like