very well put @investor12321.

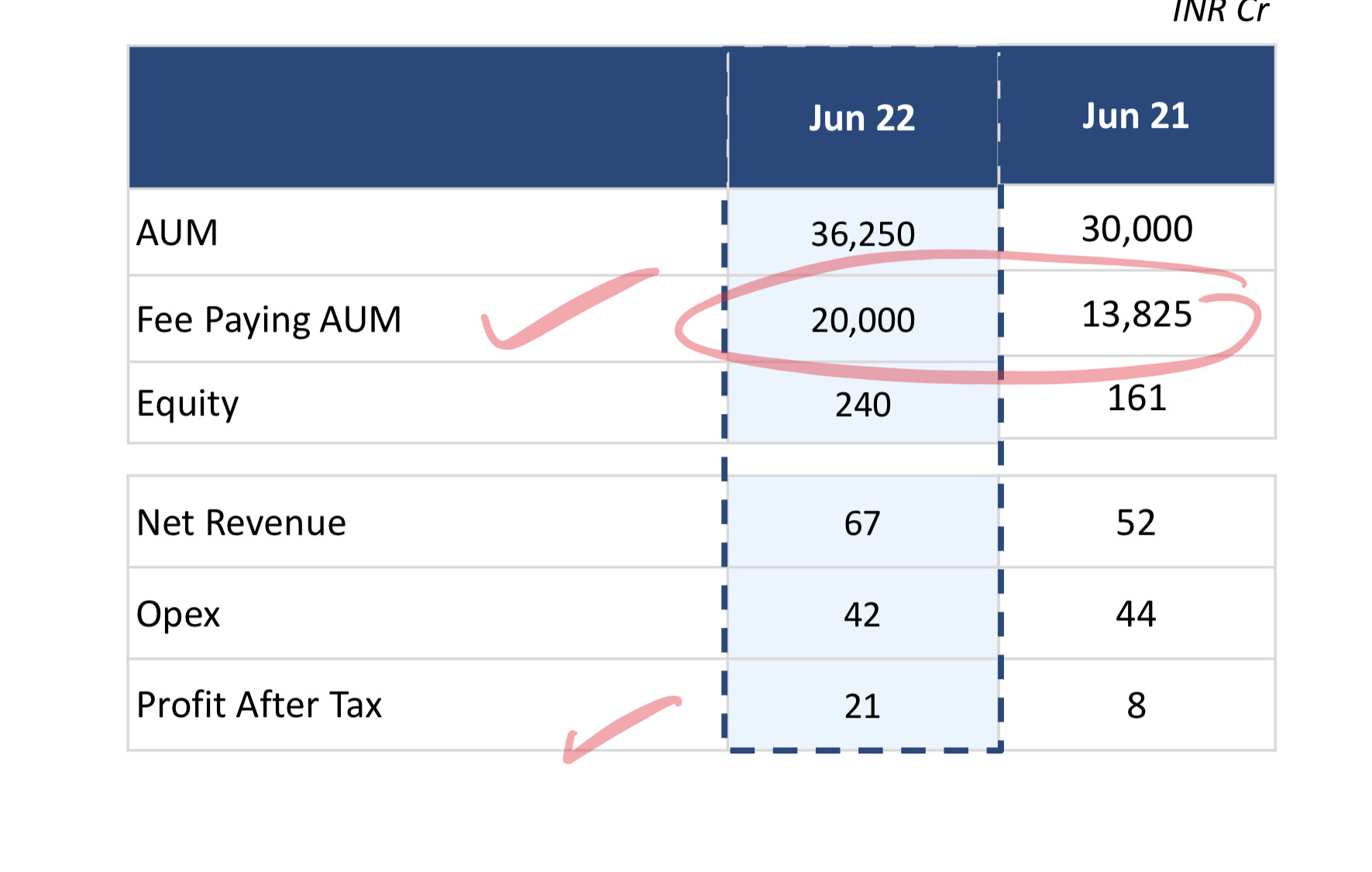

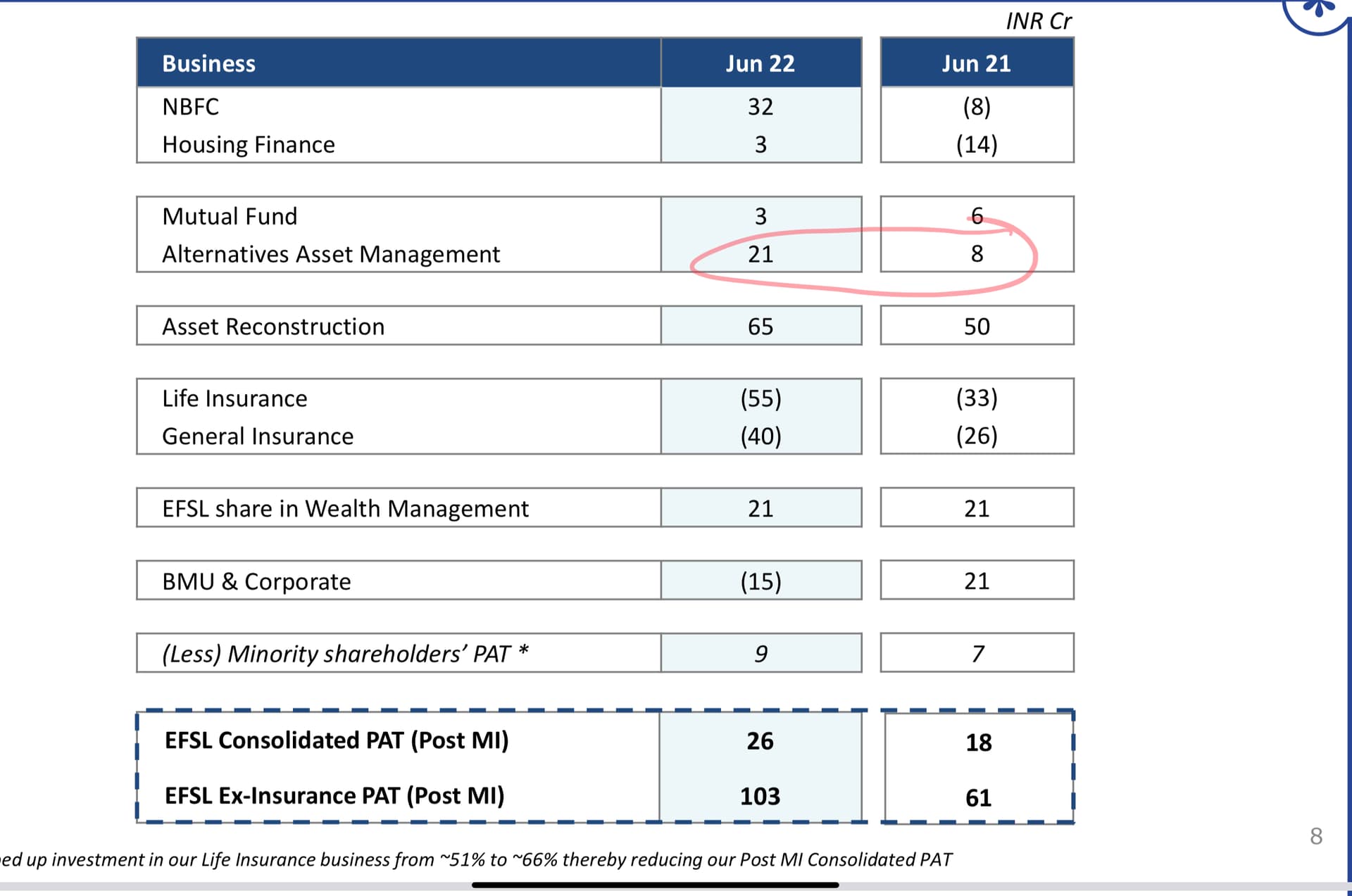

The star of the Q1 results is AIF and they are one of the leader in the segment in India. AIF needs lot of experience and it takes time to develop and needs track record to demonstrate it. The fact that their AUM (committed not deployed) is showing rapid growth auger well for the AIF business.

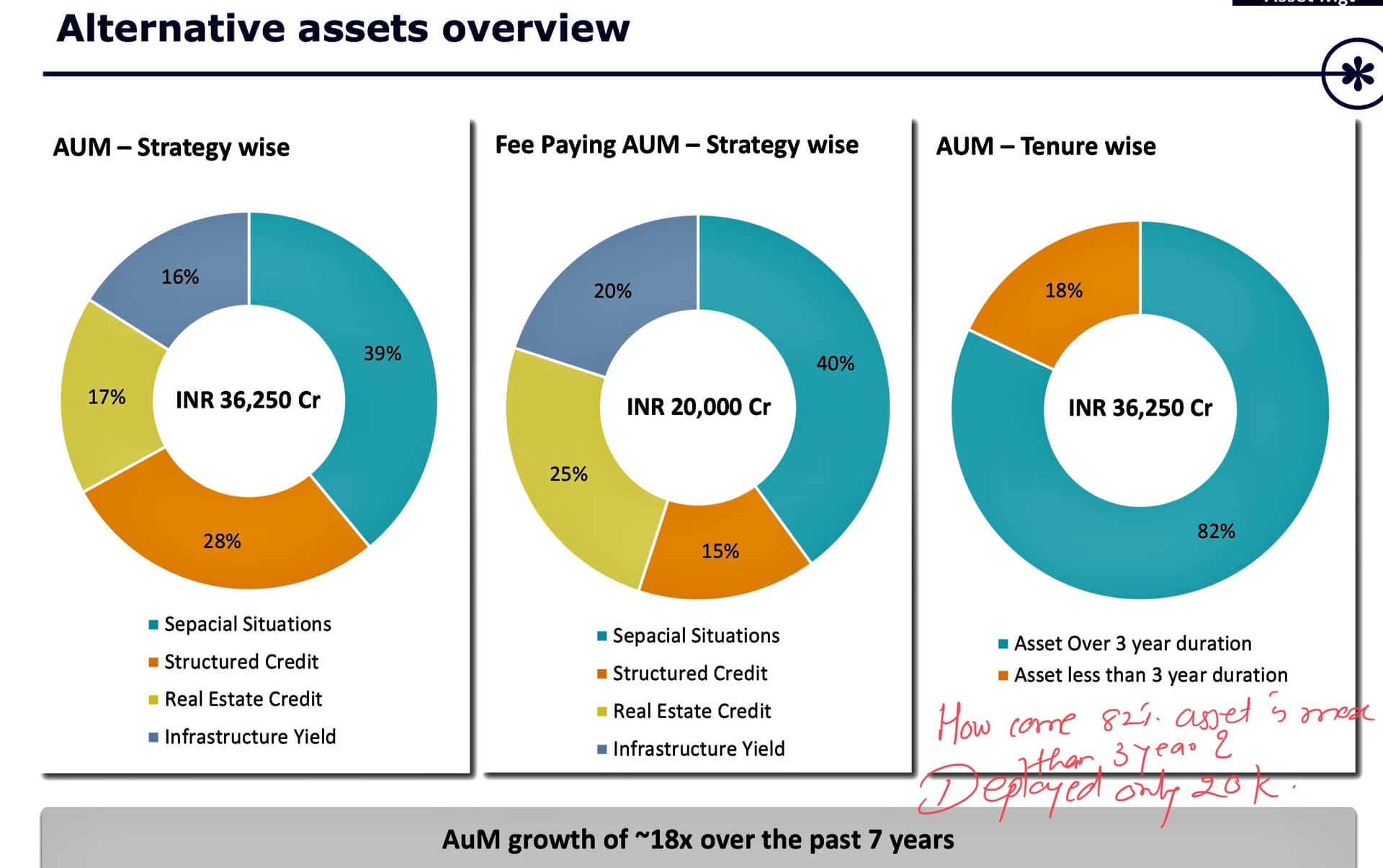

They have deployed 20k cr so far and in last 2 quarters they have deployed around 2800-3000 cr. So if they continue their earlier momentum, fee paying AUM will cross more than 25k in next four quarters. Currently AIF is showing 21 cr PAT, so by next June, it is likely to be around 30cr and that is only fee paying income.

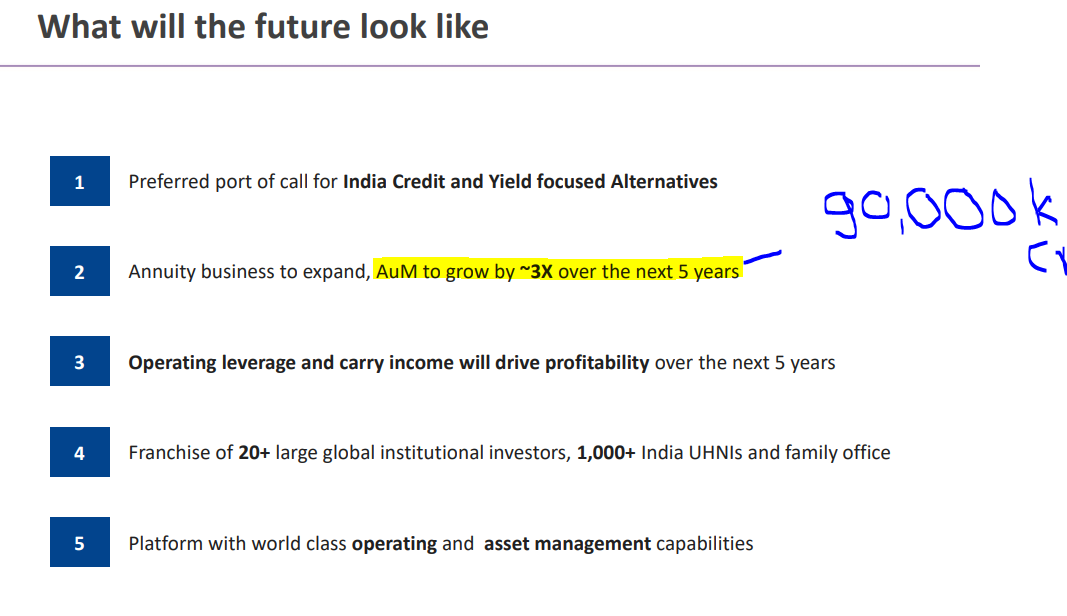

The management (Mr Shah) said, that once they start exiting the investment there will be decent carry income. In last 2/3 quarts they have saying they have existed investment but they have not said how much is the carry income, neither they mentioned what is IRR for these investments. This is very basis things one would have expected them to report, so it looks like they may not have earned decent returns.

Having said, I think this business shall report 100cr PAT + going forward (with consistently and stability) in their fee income. Once they start receiving carry income, the PAT could double, but it shall take another couple of years to materialise once they start existing their investment. Untill then, fee income will be keep the momentum going.

As per this document in early 2022

Also the good part is they own 100% of it. I wish and hope that they do not dispose it the way they dispose the Wealth management business at depress price.

Rest of the business are more or less same as Q4-Fy22, with same profitability, except insurance which is reporting higher losses because they have increased their shareholding in life insurance business from 51 to 66%.

Also they have been talking about co-lending since ages, but it is yet to show in their results. Looks like others NBFC (e.g. IIFL, Capri) are firing on all cylinders as far as co-lending is concerned, but Edel is happy to just talk about it now leaving the execution for some other day.

So in nutshell, pretty ordinary Q1 result, with nothing more to talk about it.

I found this info very helpful if one wants to know little bit more about AIF business of Blackstone, the biggest alternative asset manager in the world with AUM around $1 trillion.

Note- Invested and biased.