I have seen employee selling their shares in Intellect design around 120 just before March-20 Crash but now stock price is around 700…

1 Like

I just had a look at your excel file. If you filter simply the Insider Trades, then you’ll find there are some purchases as well. If I look from the beginnning of 2021, then net selling qty is 49 lakh shares which is 0.5% of company’s equity capital. That is not alarming.

Disc: Tracking, not invested.

You’re right that it is still undervalued. But the kind of risk that the stock comes with you gotta expect at least 3X kinda return to make the risk worth it.

Edelweiss Wealth Management listing will be happened by end of this year and expected price per share ~20Rs.

Wealth management business price Rs 4356.1 crore

Edelweiss holding 44%

Total no of shares: 95Cr

4356*0.44/95 = ~20Rs per share

Edelweiss share price : ~55

All other business price = 55-20 = 35Rs

Is it worth to own remaining business @35Rs price? It would be grate if someone provides actual valuation(not estimated by management) for other business.

Comparing business valuation between Dec 2020 and Dec 2021.

Don’t see much growth in other businesses. Any comments?

Dec 2020

Dec 2021

There shall be a considerable difference between the valuation of wealth business between June 2020 and now.

In June 2020, no one knew how the Covid situation would unfold, but there was a belief that the real estate sector would be badly affected. Edelweiss is indirectly exposed to the real estate gloom. Also, their other business, such as ARC, might have needed more equity; hence they needed to embrace the worst-case situation around March 2020. In that situation, they could only sell a Wealth Management business and get a decent amount, which they did. It gave them 2200 cr, and helped them retain their rating. Without that, they would have suffered a rating downgrade.

In hindsight, they sold is for a bargain price (or they could have got a much better price even six months down the line), so I think it won’t be appropriate to use March-June 2020 valuation to the wealth management business.

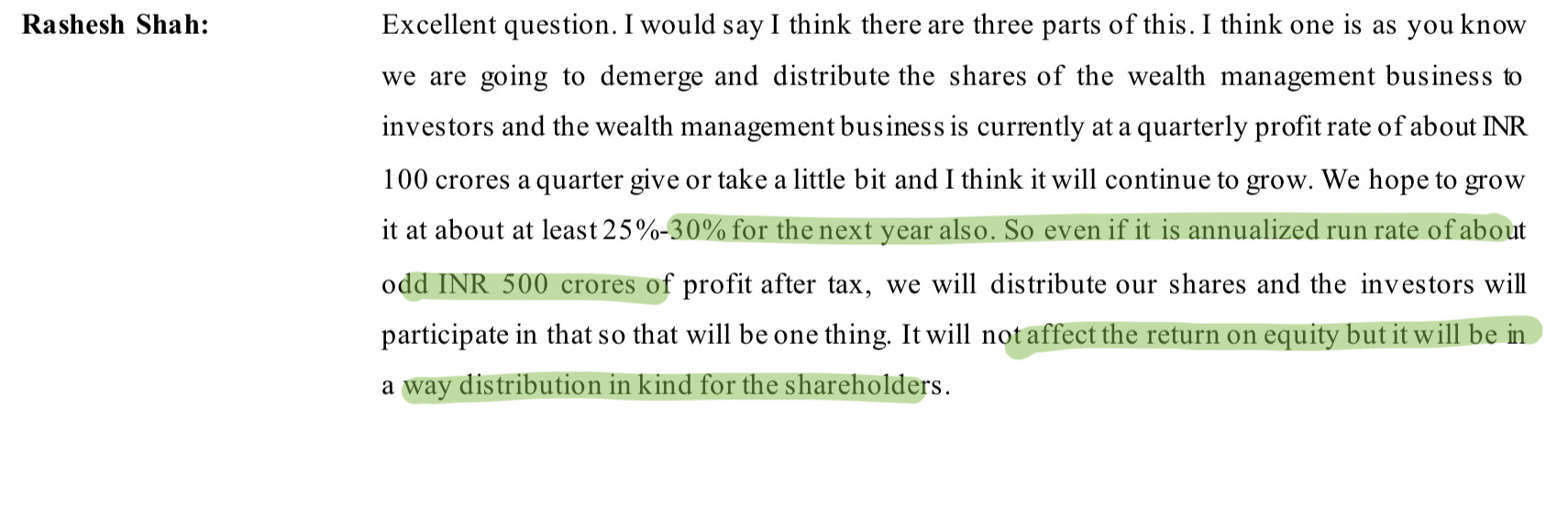

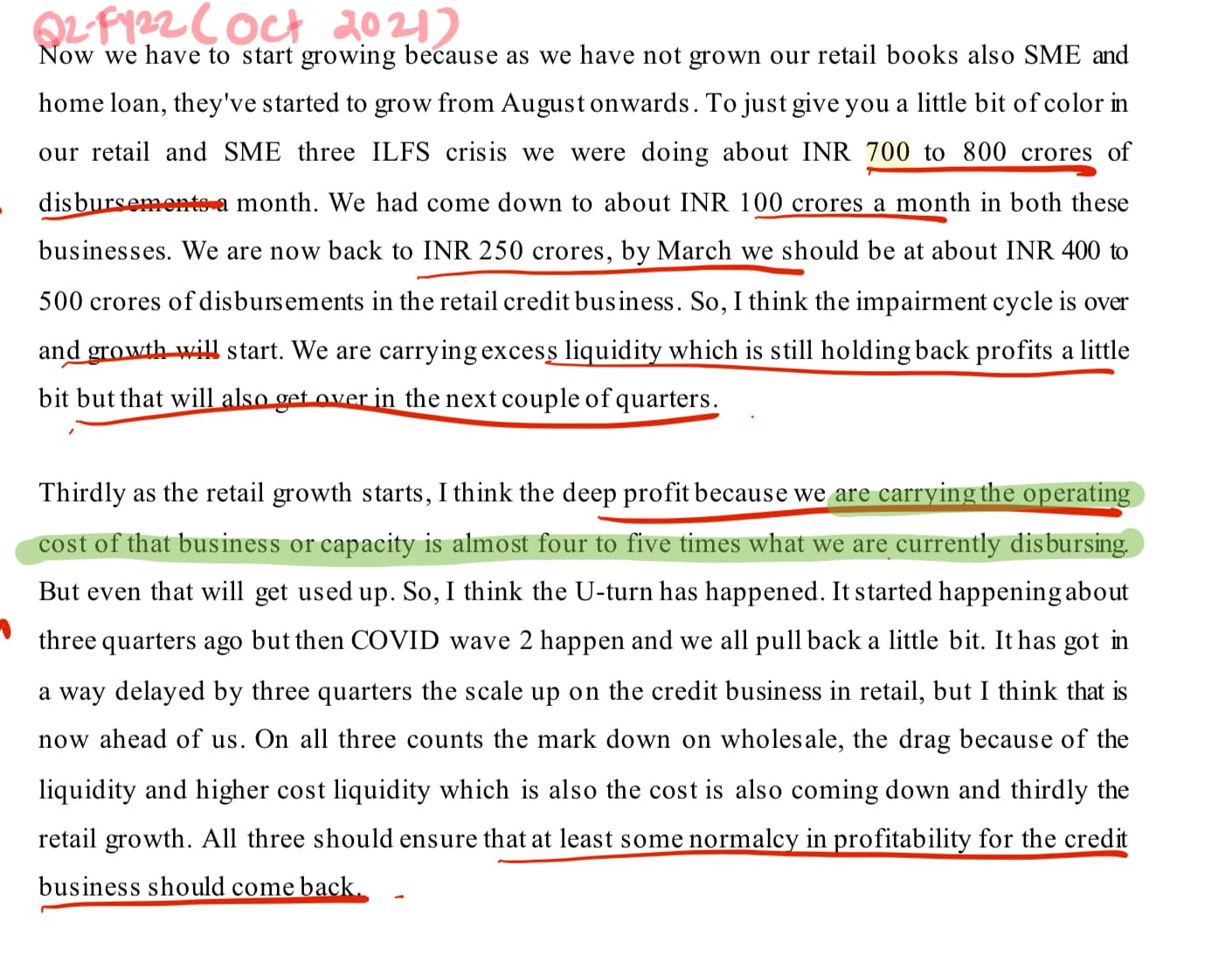

After PAG acquired the business, PAGss have invested around 400 cr of equity in wealth business (as per con call). As per Rasesh Shah, in FY23, wealth management is likely to make around 500 cr PAT and the business valuation of wealth management can be 20-30 PE. This is from Q2-FY22 con call.

… and valuation wise

So conservatively, if one assumes FY23 PAT will be 400 cr and give 20 PE, wealth management’s business itself it valued at 8000cr, and Edelweiss 44% stake can be valued around 3500 cr.

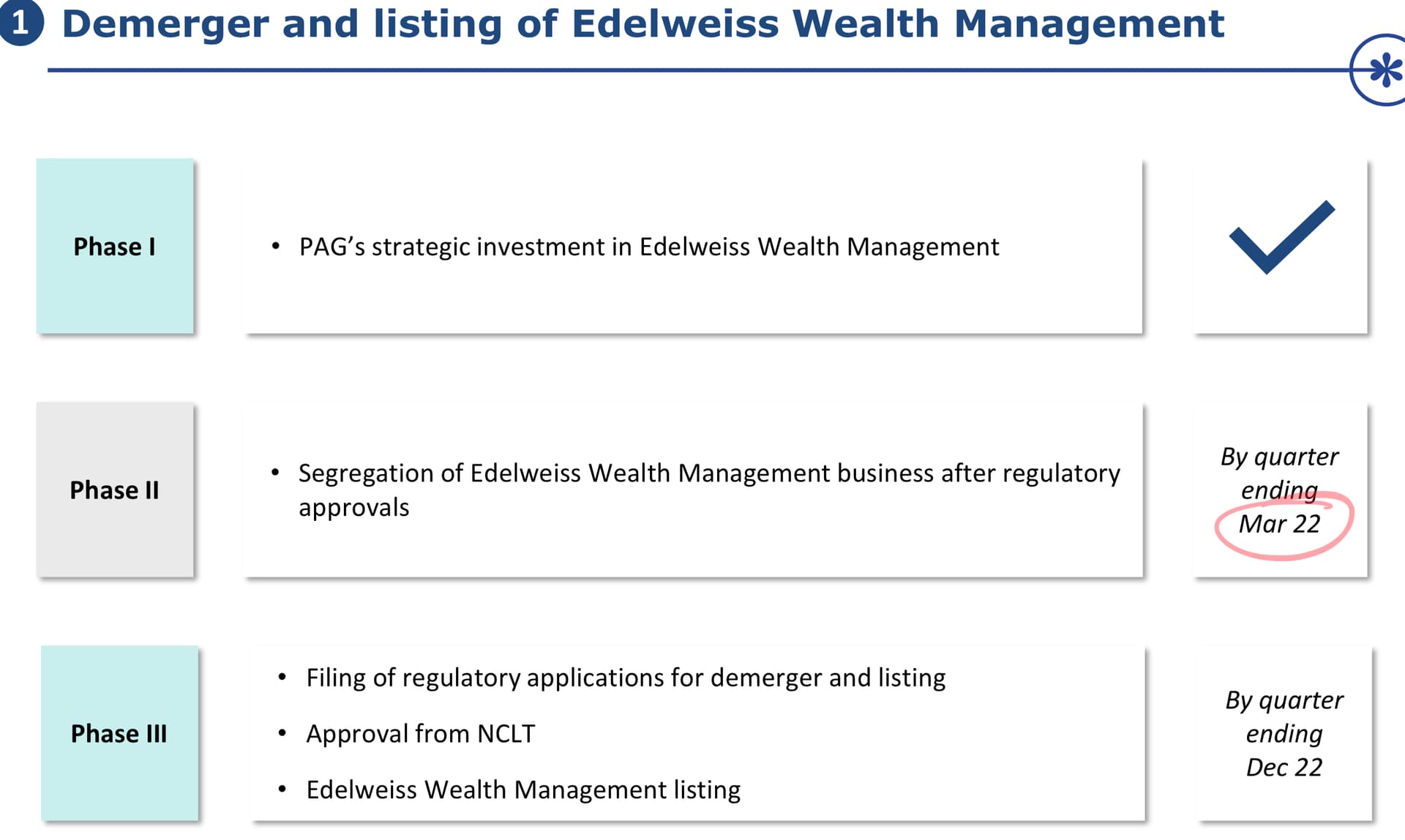

The bigger question is when this happens. They initially said it would be completed by March 22, and the timeline was extended a few times. As of now, it stands at Dec end, but when it happens is a question. They needed to complete the formalities but have not completed it yet. It had to happen by March-end, can it happen in next two weeks? If it does not, then another timeline extension on the card.

Overall, I think this is a deep value opportunity but when it realise it to be seen.

Note- Invested.

8 Likes

Thanks for the detail description ![]()

In your screenshot, management claim that they are currently getting 100Cr profit per quarter but I can see PAT is only 55Cr in last quarter:

Am i missing anything?

You are not missing anything and they have never reported 100 cr quarterly profit. However, last quarter was around 93 cr.

Sometimes what management saying does not match with results. It means one of the two things IMO.

1- PAG has invested an additional 400 cr. Q3 could be their first or second quarters of full control. So they are doing additional investment or revamping operations, resulting in more expenses or delayed profit. Hence, instead of reporting higher profit, they prefer to invest now and reap reward bit later.

2- Business is generating that much profit, and management just overhyped it. If you hear management call, it is clear that they tend to paint things most optimistically, and this could be another example.

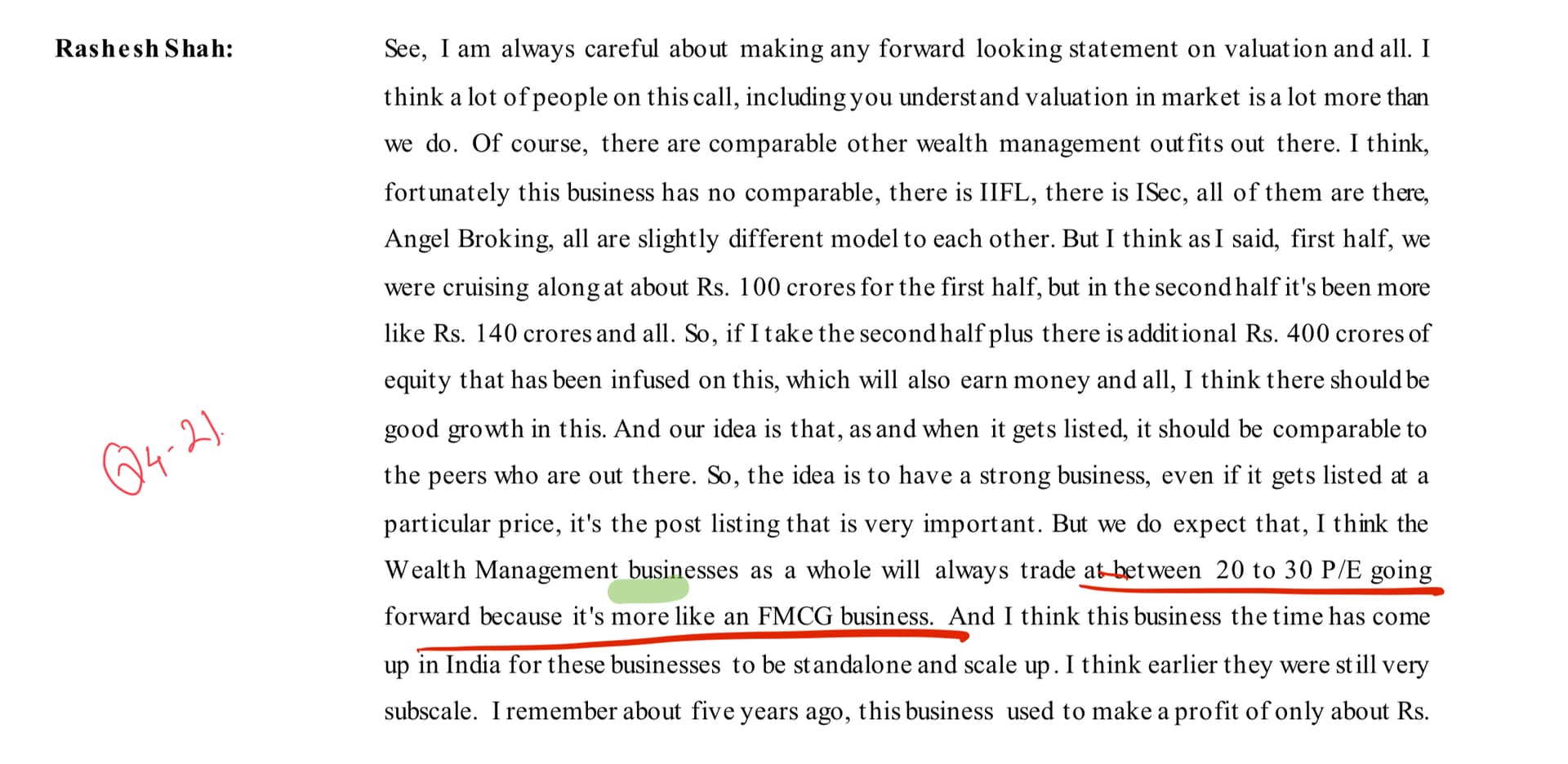

I am not sure if they can report 500 cr PAT for FY23, but I think they can report a profit of 375-400 cr and hence I assumed a lower multiple of 20 while calculating its valuation.

Even at 20 PE, it would be the cheapest listed wealth management company as compared to IIFL Wealth (27 PE) and Anand Rathi (55 PE). And we are talking about just one of the 7/8 businesses of Edelweiss.

Hope it helps.

6 Likes

Yes thats totally true.

Thanks again for detail clarification.

2 Likes

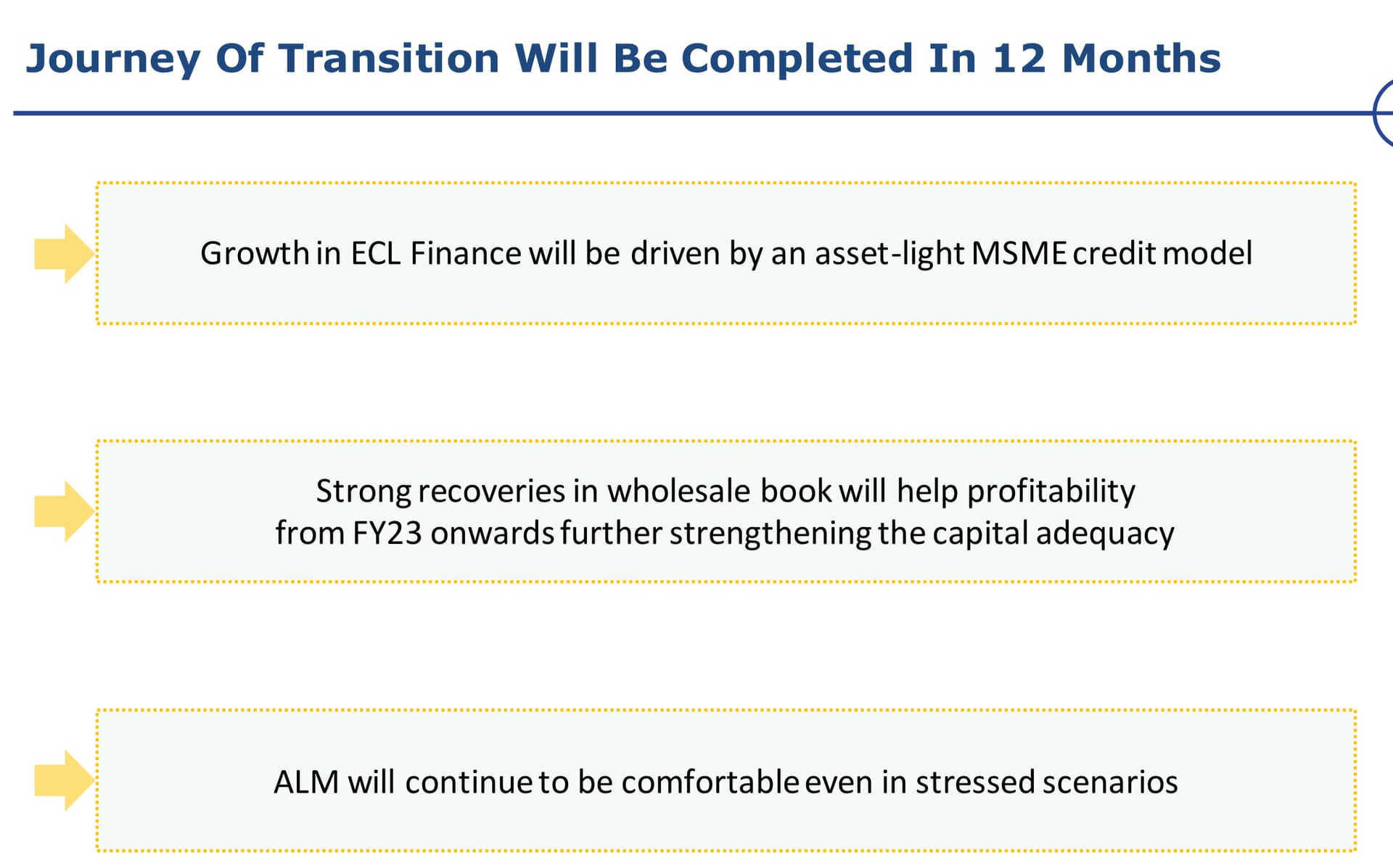

The fortune of overall Edelweiss is dependent on ECL Finance to a large extent. However, most non-ECL Finance businesses are still in the investment phase (e.g. Mutual/AIF/Insurance), and the ARC business is a transition from wholesale to retail. So these businesses are unlikely to report significant profitability in FY23, although management is very optimistic about each of them from FY24 onwards.

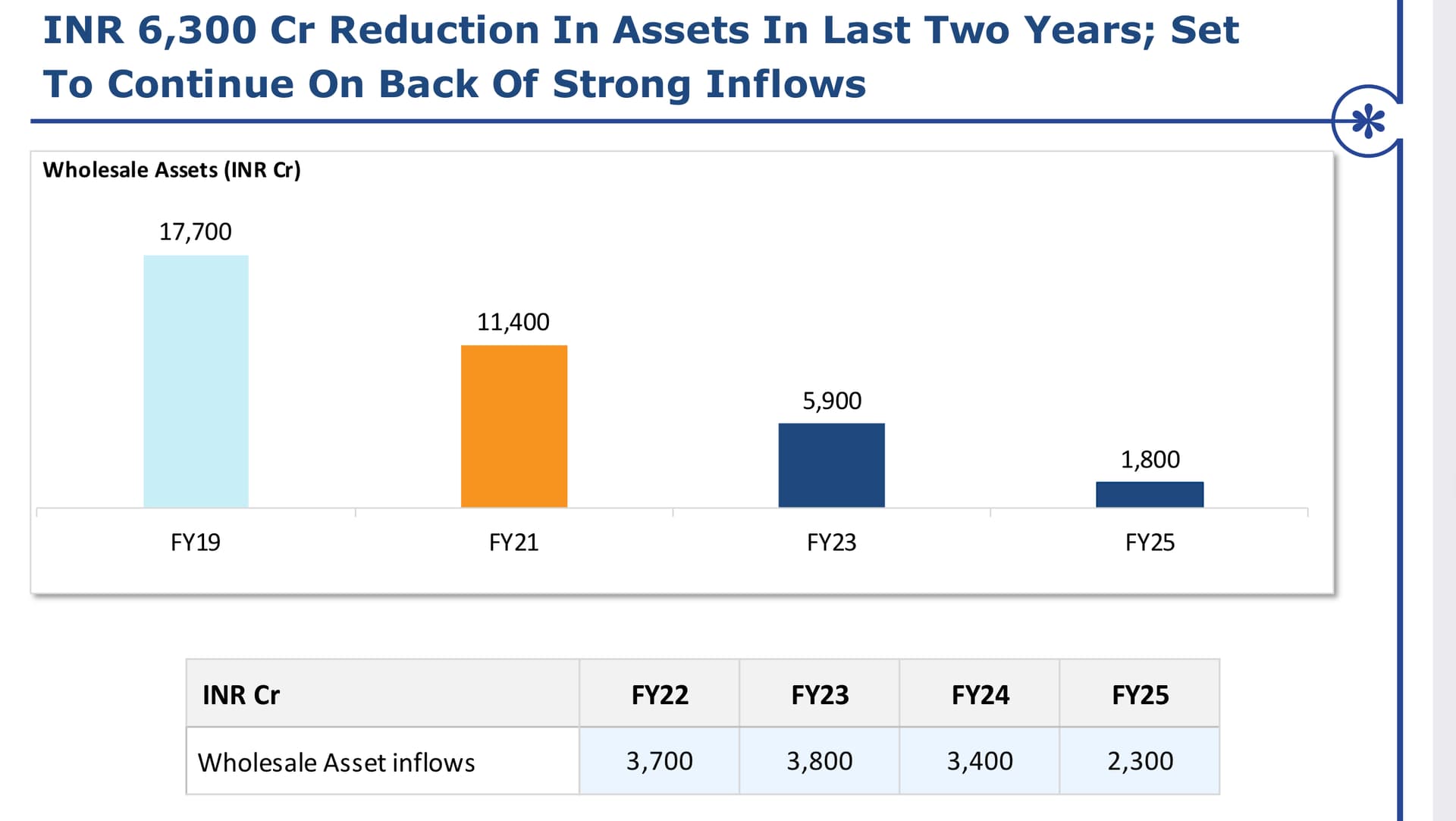

ECL is a dark house that is transitioning from wholesale to retail.

Currently, they have a loan book of 8500 cr, and they are reducing it by around 700 cr per quarter (actually, it is less, but consider this amount for simplicity). As a result, their wholesale assets are reducing by 700 cr per quarter, but their retail business is not growing enough to compensate for the corresponding reduction.

.

I know they are talking about co-lending, so the whole loan book won’t be reflected on ECL’s book anyway. So far, co-lending is more of a talk and less of a substance. They have been talking about co-lending for the last 2-3 years, but they have not shown significant traction on it so far. When analysts ask the reason for slow growth in co-lending, they always have a reason to provide for not generating revenue from co-lending, but at the same time, they always show huge potential. Maybe there are transitioning from wholesale to retail. Hence we do not see that in number. Hopefully, co-lending materialises sooner or later, and it shows in number.

In Q1 FY22, retails (MSME+ Housing Finance) increased their AUM by 300 cr, in Q3- 400, it shall reach a pre-covid level of 700 cr.

Although the Q3 con call refers to 700 cr per month, when I read earlier call, I presume this is 700 cr per quarter.

I will be happy if it is 700 cr per month, but I still think they are aiming for 700 cr per quarter.

Barring any unforeseen circumstance, I presume by Q2/Q3 of FY23 (Sept/Dec 22), their retail loan growth shall exceed the reduction in the wholesale business. As a result, their total AUM for ECL shall again start inching upward. This shall change the fortune of ECL.

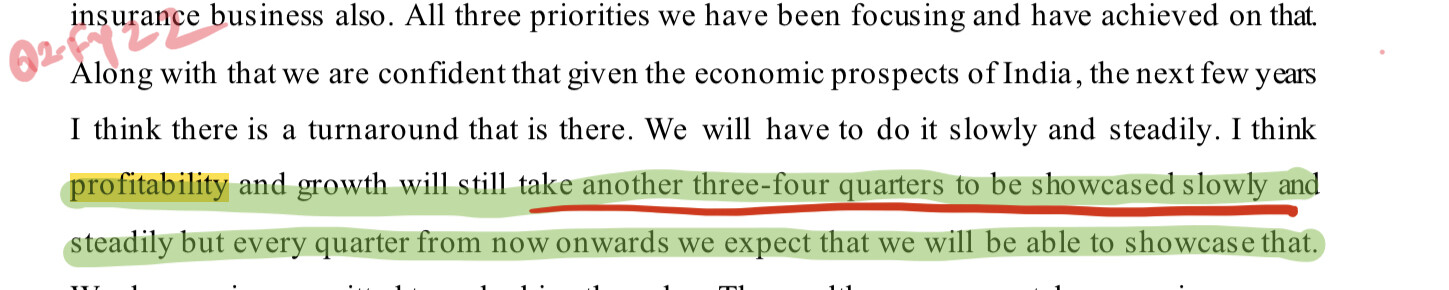

Management has indicated that they are looking to turn around this and improve it in earlier calls. I think FY 23 shall be a turnaround year for it. Even if it does not grow, I believe it will lay the foundation for further growth in FY23. They have said that it will be returning to profitability in 3/4 quarters, which will be around Q2/Q3 of FY23—one more hope.

note- invested

4 Likes

The date seems to be pushed further to April as per this

“We expect the hive-off to be done by December. There are two stages — first gets over in April and the second stage starts immediately,” he said.

Further takeaway from this article

EWM, which operates across client segments from affluent to ultra high net worth, is eyeing 22-25 per cent CAGR in client assets over 4-5 year period, Kehair said. As on date, EWM has client assets of about ₹2 lakh crore, he added.

Currently, EWM has 2,500-3,000 HNI families and 8 lakh ‘affluent’ clients. “We hope to effectively grow our overall client base by 30-40 per cent every year. We have a strong multi-product digital offering for our clients. We will not go mass-retail. We think banks are well positioned to be in that area (mass-retail)”, Kehair said.

EWM is also open to inorganic expansion to grow its business in the coming years, he added. This firm, which operates in wealth, asset management and capital market space, aspires to significantly grow its asset management pie from ₹3,500 crore now to ₹50,000-60,000 crore in the next four years, Kehair added.

2 Likes

We will get more idea in this quarter AGM.

Also, Hemant Daga is reducing his stack which is reported in insider treading. I think it is because of he leaving company.

1 Like

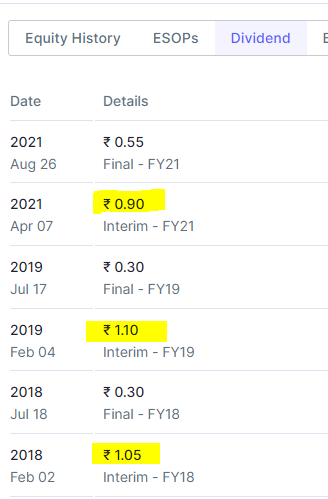

Edelweiss has scheduled a board meeting to declare Interim dividend

Based on the earlier dividend announcement, they are likely to declare around Rs 1 per share.

I think they would do well NOT to give dividend (and increase net worth), but seems promoters are in need for this cash.

2 Likes

@paragbharambe Did Mohnish ever talk about Edelweiss anywhere like his other investments Micron, Rain Industries, Sunteck Realty.

Just want to look at his breakdown.

True. Agree with your take. Reinvesting in growth is the preferred way to go for Edelweiss as of now rather than taking the dividend out of share value.

@karuturi2050 Nope… I have not seen/heard Monish Parbari talking about Edelweiss. But I have read Amit Wadhwani talking about it. Please refer link from the post above

@paragbharambe I did a quick search and it seems Moerus funds(Amit Wadhwani) sold all its Edelweiss stake on 11/30/2021

3 Likes

There was reddit leak of his letters to his investors in his fund addressing why he invested in edelweiss ,it was posted somewhere here in this forum but soon taken down .You can search it on reddit and find it out there.

3 Likes

Thanks for sharing this good finding. It seems he lost patienece with Edelweiss in term of growth.

If you want to search for reason to buy Edelweiss now- they are hard to find (other than value). It has been value stock for some time, but at the same time it is going lower and lower.

Key event which will re-rate the stock is Wealth management demerger, but it is not likely to happen in next 10-12 months. If you are investor (PMS/MF), it is very hard for them calculate where the share will be in next few quarters, hence they must be hesitant to buy into it.

Monish is saying that other then ECL Finance, Edelweiss have collection of good business that are well placed to capture financialization theme for India in next few year (may be decade). I think it is hard to argue with that, but the market is overly focused on it’s wholesale lending portfolio, and depressing the price.

3 Likes

Co-Lending is becoming a buzz word. Here is another one with SBI

… and ARC more business.

2 Likes