This qtr wealth management business opex too high because of which np is low…was expecting much higher np from wealth business

Life insurance they increased stake so now from next qtrs we could see higher losses on edelweiss share on life business

Without one time other income on insurance broking business they would have posted a loss

Any one else if could share there opinion

Really difficult to understand there domestic amc + alternatives have aum of 1.10 lakh crore there wealth management business can easily generate pat of 350 to 400 crore yearly with edelweiss share of 44%, there arc business is giving good profits…only drag is life and general insurance…only hope is wealth management demerger…management even avoided concall this qtr…

The company has disclosure/governance issues. Even after discounting all, the valuation seems out of tune with intrinsic value- Even assigning all their funded/leveraged biz to 0, Walth Mgmt, AMC and Insurance and ARC biz together seems to be valued quite low at ~6k cr. Also the enormous amount of shareholding by reputed institutions give some leeway for corp gov concerns. Disc: Adding at current price

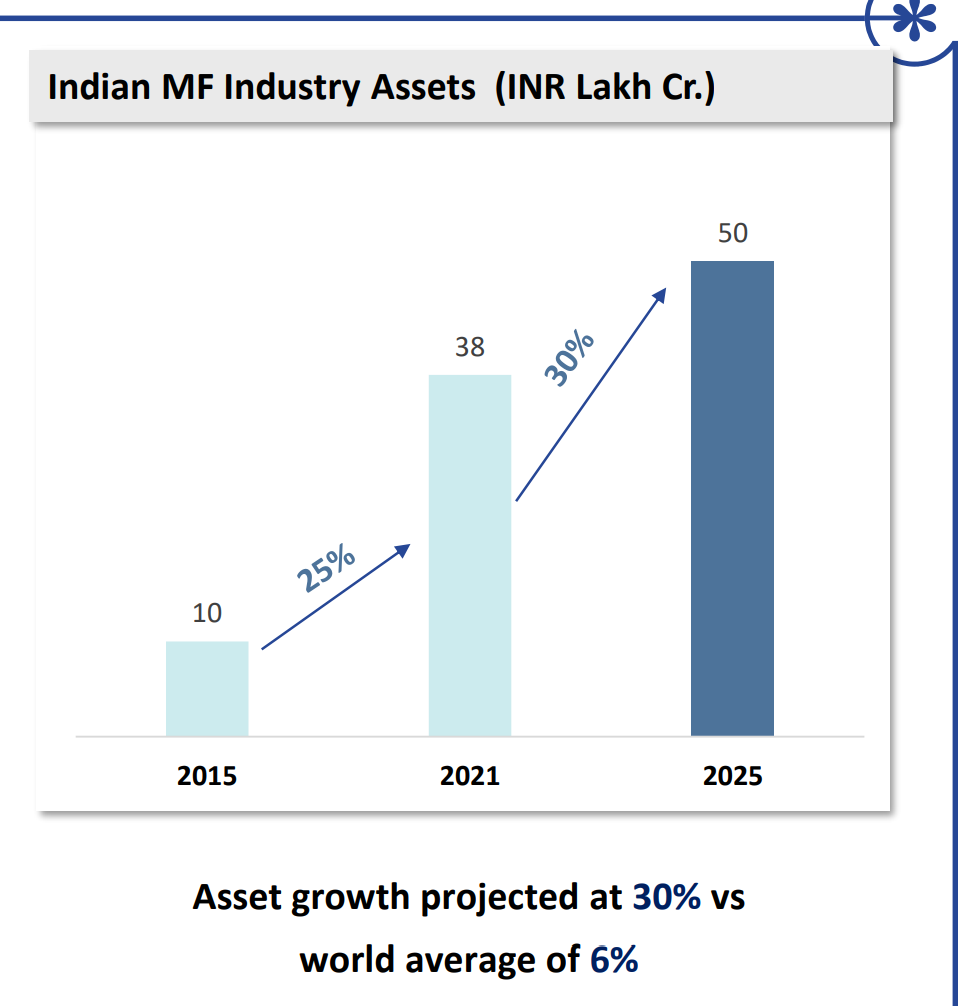

between 2015 to 2021 i.e. over 6 years they grew by 25% i.e 4.25% p.a. where as from 2021 to 2025 over 4 years they are showing a growth rate of 30% i.e. 7.5% p.a., no idea about whether they are comparing world averages over the same period…

From 2015 to 2021, they did grow at a CAGR of 25% - hence the 10Lcr to 38Lcr

From 2021 to 2025, they expect to grow by an absolute % of 30% from 38Lcr to 50Lcr. Not CAGR.

Showing CAGR and absolute % for different periods in the same graph should be a punishable offense.

Spot on enigmaak, you are right, sorry i missed the point that they are mixing CAGR with absolute growth (if the same is translated into CAGR it would be around 7% only compared with 25% in previous years).

Edelweiss available at 5k crore market cap…dont know what is going on? Anyone has any idea on todays 8% fall with volumes?

Amc + wealth + arc + life + general + nbfc all available at 5k crore market cap…this valuation is not justifiable its only because of managements not so good reputation in market

It is undervalued relative sum of parts intrinsic value. NBFC is zero networth (may be little -ve). It is undervalued and they have to improve corp goovernance. Edelweiss should focus only on non-leveraged biz and improving corp governance- valuation will follow

The stock seems to be grossly undervalued. Its mutual fund AUM as on Dec 21 is 70400 cr worth 3000 cr @ 4%. Wealth management business likely to be listed separately. Arc business is also doing ok. Mohnish Pabrai and RJ has invested heavily in the stock. Hope rating improves in the future.

If management is clean and valuation is cheap then they should buy at this valuation. Insiders are continues selling and don’t see any single buy entry(Market purchase).

One of the question asked in AGM meeting (3 quarters back) related to buy back stock at premium value so that investors trust increase. Still they didn’t declared any buyback.

I think this is normal with the current status of the company, there is not much positivity in the market because As in last two year company have not shown the result as shown by its pairs and also moving away from big ticket (i.e. wholesale) loans taking a toll on company earnings which i think is a good move as company does not have any deep capital backup.

There are two things to look forward in future:

Wealth and Asset management

Low capital required

Providing an alternative vehicle for investment directly into the projects (with the current economic condition of India is very favorable for development).

Insurance:

If managed properly can given a low cost capital, which can act as a fuel for wealth and asset management business.

Where, there both business vertical need good forward looking management, i think edelweiss already have this kind of management in place.

This is what i have understood while going through the companies annual reports and do comment if i missed or miss interpret.

The key concerns are probably the ARC and Credit business.

They still have Rs. 8200 cr of wholesale book, and one doesn’t know how much of it could be dirty. Besides that, they don’t have any edge in the credit business especially in Retail as their cost of fund would be really high (Wonder why they don’t disclose their yield and CoF in PPTs). The credit business combined have net worth of Rs. 4,700 cr which the Street doesn’t want to value given that their RoEs have also fallen below 3%.

The ARC business have also gone no where, and the recoveries have fallen from Rs. 11,300 cr to Rs. 2,500 cr in last 3 years. Co. has equity investment of Rs. 2,400 cr in this division as well.

So, how do you value these two businesses which has combined networth of Rs. 7,100 cr and no knowledge about what kind of assets is the company holding? Especially, given that they had to provide for/write off loans worth Rs. 5,500 cr in last 3 years (FY19-21). This part is the joker in the pack, if these division turn around you make good money as Street is not giving much value to it.

On positive side, the Wealth Management could be a value unlocker given the valuation at which other Cos. are trading, but here Edelweiss has only 44% stake in the business.

Investors already consider Credit biz to be worthless (0 and likely to destroy some more value). Wealth advisory, AMC and Securities are the only plays-insurance biz at best valued @ equity. Considering only these 3 + equity in insurance - still undervalued. Low downside with decent upside