Instead of buying in Ncd issue of edelweiss , better to buy 8.80 % monthly edelweiss debentures from market wich is available at 10 % discount

Ncd of 8.8% is raised for their NBFC and HFC right?

The interest rate seems high, how can they give competitive loans then?

Q2 result is out.

Looks like the ship is beginning to stablise. Rashesh Shah has said “ Our Performance this quarter has been strong across all businesses and the positive trend will continue hereon.”

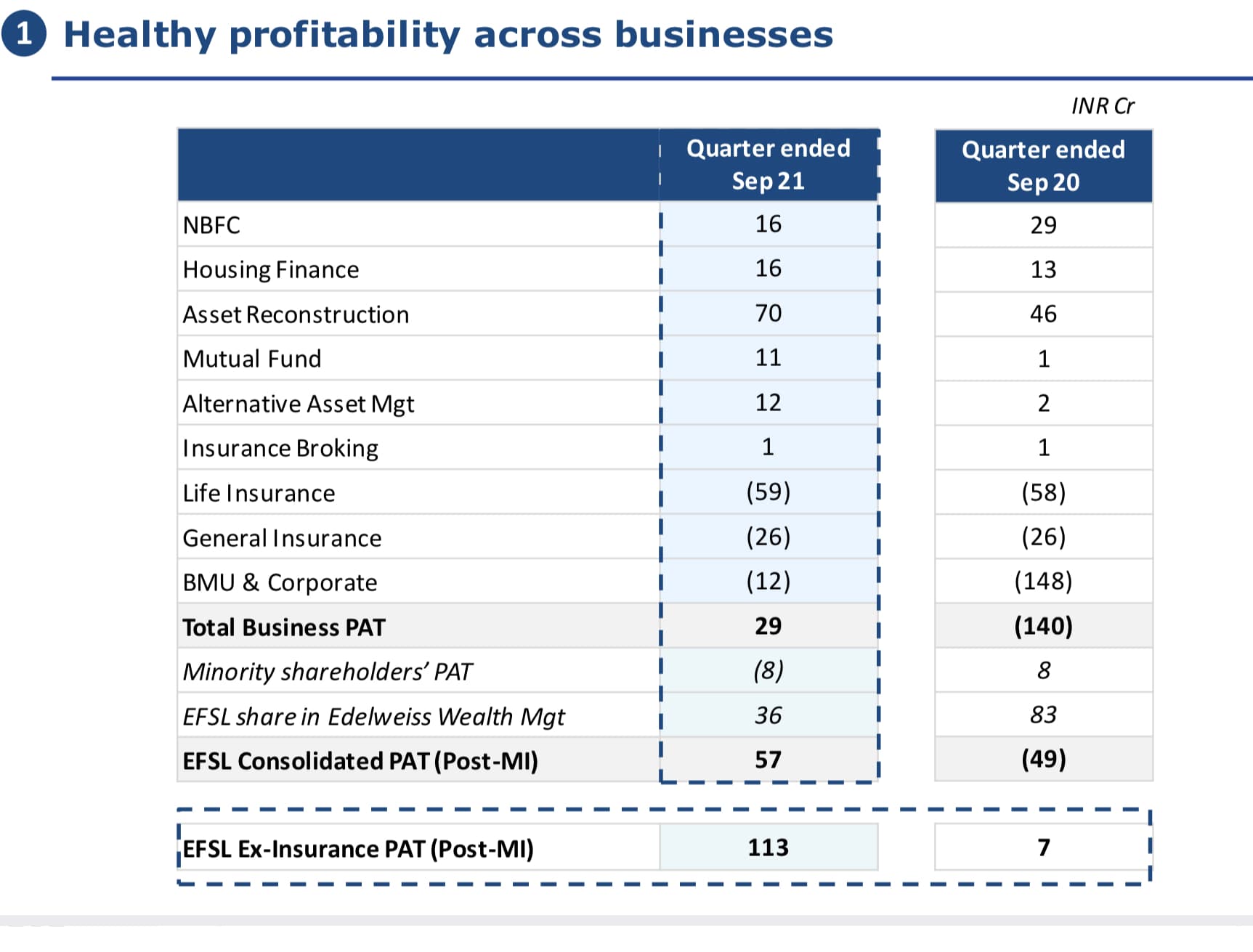

Consolidated Result

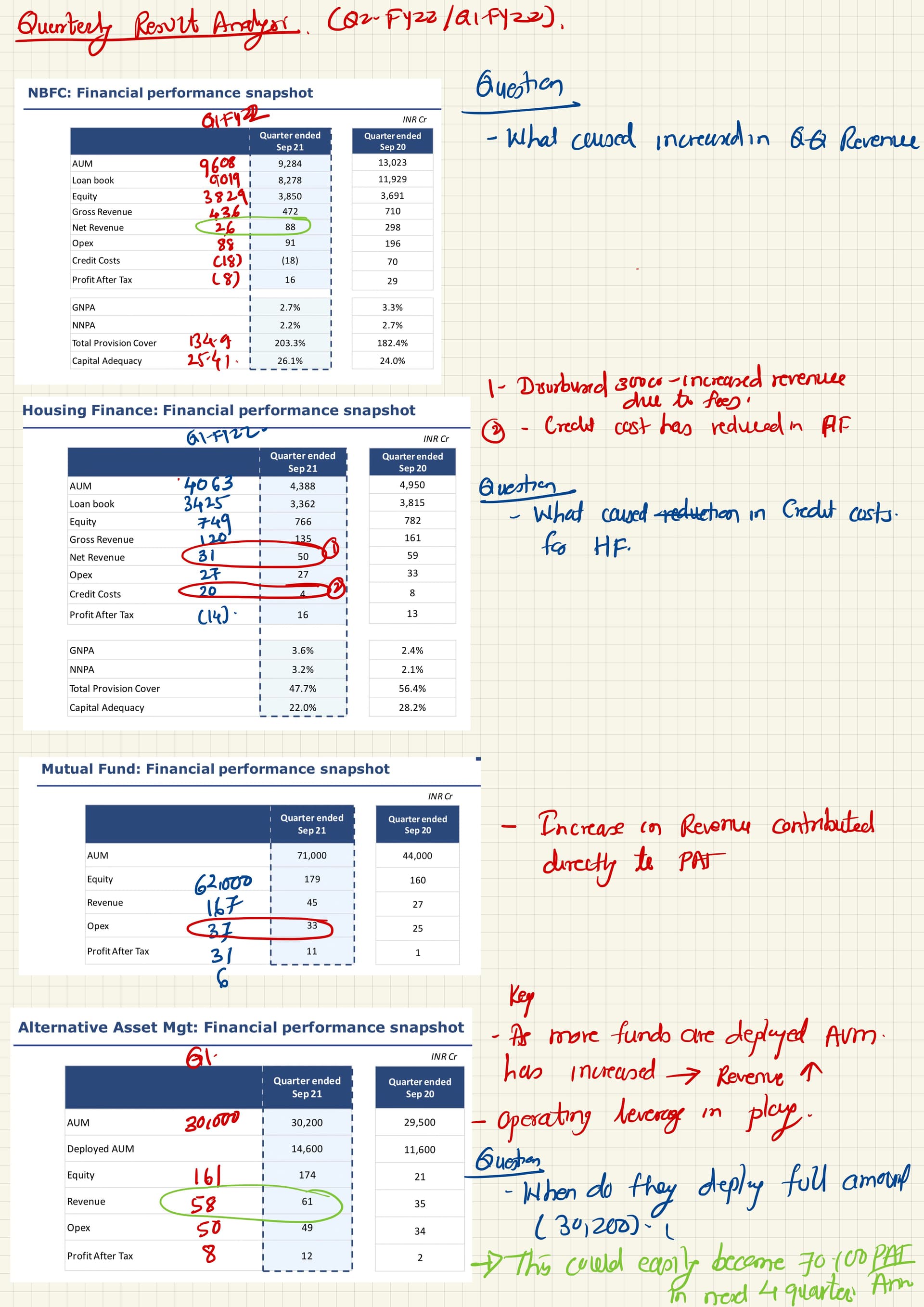

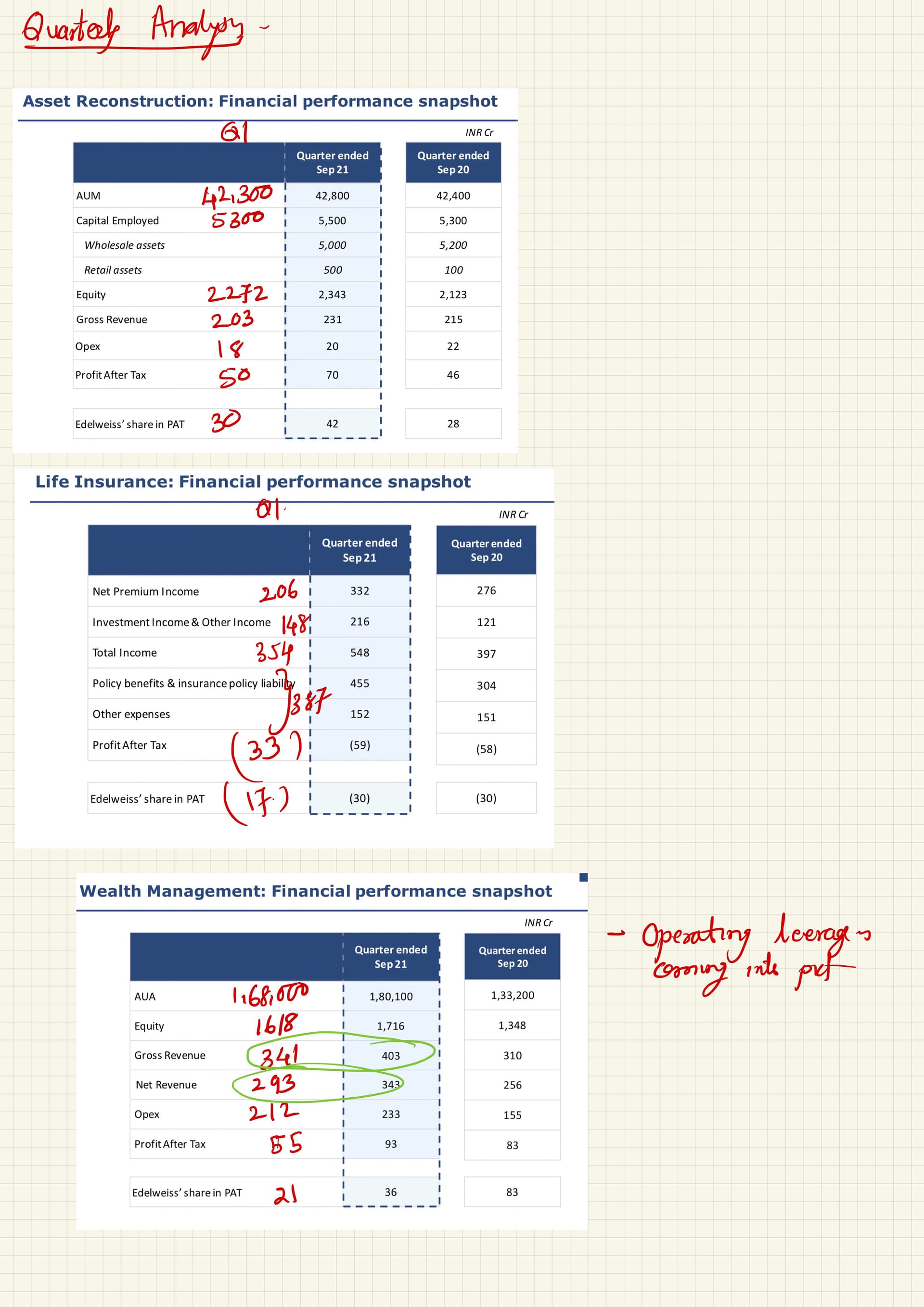

I scribbled some notes and compared Q2 with Q1 of this year. They gave big ppt but did not give Q to Q comparison. So I spent some time noting the difference of Q2 over Q1. The number I mentioned are from Q1-FY22. I am attaching it here as other may find it useful and do not have to spend hours comparing Q-Q.

Page 2

Please refer to the ppt for details.

Q2- FY 22 Con Call notes.

I scribbled some notes from con call.

-

By March 2023 we are hoping to build fortress balance sheet.

-

From now to March 2023 focus will be growth and profitability.

-

It will take 3/4 quarters to really show the growth.

-

Key focus - Realisation of out customers.

-

Worst in term of impairment is over. Now reversal will start. We should get back 700cr over next 4year. That means around 120 to 150 cr shall come back per annum over next 4 years. We are in reversal cycle.

-

Retail- 700cr/per month disbursement before Covid, but it had slowed down to 100 cr/month. Next few months we shall bounce back to 700cr.month. This shall improve profitability as most of the cost are incurred.

-

Wealth 100cr/quarters…. PAT of 500cr/annul- Distribution.

-

ROE target-

- Credit 14-15% ROE

- Aim for 20 ROE for consolidated… (without Wealth management and Insurance).

-

Share buyback- We would rather use funds to growth. Focus is on growth. If we have excess capital we will look in buyback.

-

Hurdle rate (own Intrinsic value) of 18 IRR

Insurance

- Life insurance-Should be worth 4000-5,000 cr at intrinsic value. We own half of that. Share around 2000-2500. Invested around 500 cr so far. Need 500 cr in next 3/4 years which are already allocated.

- Non Life- Shall value around 2000-2500cr. Need 100 cr/annum. It is already allocated.

- Break even in 2025/26.

- Value should double from here.

Whole sale book reduction- Repayment and resale of assets

- Focus on reduction of 2000- 2500 cr per annum.

- In next 3/4 quarters we shall reduce whole sale at 1000 cr/annum.

- Focus on project getting completed.

- Earlier workout- Sell project. Now we can do it organically as last mile funding is available to builder. Earlier we were not giving last mile funding so workout was not there.

- No more impairment for NPA this year.

- Get this book to zero by 2025.

Total AUM- 100,000cr.

- Profitability is 10 points now but shall go to 20 point

AIF

- Carry income will start coming from 2023/24 onwards. It could be 800 to 1000 (Edel share) cr per annum.

- Currently deployed only half of 30,000 cr. As we deploy, we get more return and this shall add to PAT as most of the cost are already incurred.

Hearing this for the last 2 quarters.

Promoters are selling stocks in the market for the last 4-5 months. I dont think they will byback.

Promoters are not selling the management is selling and they can sell because they were given the shares under ESOP hence they don’t care that much.

Edelweiss Tokio Life Insurance Company (ETLI), a subsidiary of Edelweiss

Financial Services Limited, was launched as a partnership between Edelweiss

Financial Services and Tokio Marine. The agreement that was entered into between

the two shareholders in 2009 was valid until November 2021. Both shareholders

are engaged in discussions on a new arrangement that works in the best interest of

the business and the stakeholders.

ETLI, which completed a decade in business this year, is well-capitalized with a

healthy solvency ratio of 200% and on a high growth trajectory. It has a strong

portfolio of insurance products and a well-diversified distribution platform. The

shareholders have infused approximately INR 2200 crore into ETLI till date and

EFSL continues to hold a majority stake. The performance of this business even in

the face of crisis like the pandemic has been promising and strengthens our belief

and commitment to its long-term growth.

Question:

1- Why both partied left to the last moment to negotiate? Is all is not well?

don’t read too much into it. JV partners do try to increase respective stake when one of them sees opportunity and believe in the long term value of the business. it is largely a positive indicator that both JV partners are positive about the long term outlook.

Good move and looks like the transaction is done at the same valuation as PAG got last year.

Last week there were news of IT department raided 4 arc companies…any idea which 4 companies were raided?

Quick question for anyone who is actually invested in edelweiss.

What do you think the intrinsic value of edelweiss should be in next say 3-5 years. ( With thesis )

My take on edelweiss

Edelweiss in 3 yrs should trade atleast 3x from here

By next yearend wealth managmenet business will be demerged and as per management stated guidance of 500 cr profit, wealth business at a mere 20 times earnings should trade at 10000 cr market cap and 44% is held by edelweiss so 4400 crore edelweiss share…however iifl wealth and anandrathi are trading above 25 times.

Mutualfund along with alternatives can be valued anywhere between 3500-4000 crore… i am expecting by 2024-25 even mutual fund business could be demerged and looking at the fast growth in the sector i feel the value of mutualfund business alone could be more then the current market cap.

Life and general insurance currently can be valued at 4000 crore and 2000 crore however edelweiss share on life insurance will be 2000 crore.

Apart from this businesses we still have arc, nbfc, housing left…

Added positives : Pabrai funds holding 7.7% is an added advantage…normally mohnish pabrai invest only if he sees 5x 10x potential.

Only issue i feel is promoters name in market is not very clean and so not getting the desired valuation but once wealth business is demerged it will start the process of creating value for shareholders.

I am invested in Edel for more than three yrs. This post is not a direct answer to your question. I am also a buyer at CMP; I have attempted to explain why I feel there is a divergence between the present MCap and fair market value.

I understand Edel as a HoldCo with five verticals.

- Wealth Management

- Life Insurance

- General Insurance

- Lending

- Edelweiss Global Investment Advisors (EGIA)

Management likely to dismantle the holding structure in the coming years.

- Wealth: Edel holds around 44%. Assuming 3% AUA as the value of this asset-light business where the company is among the top 3 players. Edel’s stake: Rs. 2K Cr.

2&3. Insurance: Edel holds 51% in LI and all of the GI business. I am valuing each of these at Rs. 2K Cr. This is, of course, a management estimate as discussed in the last concall.

This gives me around Rs. 6K Cr. for the first three businesses.

-

Lending: Eventually, this will be ECL Finance and a housing finance subsidiary. Edel holds around 85% of this.

-

EGIA: MF + Alternates + ARC. This, imho, is the least understood. Both Alternates and ARC tend to have back-ended cash flows; these consist of a management fee and carry / profit share. However, Edel – being the investment manager - will receive these amounts only when that particular fund / SPV / LLP / trust is wound down. Same with the ARC: Edel will get cash ONLY after all SRs have redeemed. Kora and Sanaka are equity partners. In addition, 40% of the ARC is held by others.

Given impairments in the lending business and the ARC, I have conservatively estimated the value of 4 & 5 at Rs. 6K Cr.

Valuation

This brings me to a SOTP value of 12K Cr. Assuming a MoS of one-third this number, any price below 8K Cr. presents an undemanding valuation (MCap at CMP: around Rs 6.5K Cr.)

Now can we please have people come forward ( who dont own the stock/thinks its a bad investment) and tell the reasons as to why they think edelweiss is going to flop ?

Edelweiss has signed co lending pact with Indian Bank.

Mumbai, January 10, 2022: Edelweiss Housing Finance Limited (EHFL) and ECL Finance

Limited (ECLF), today announced a strategic co-lending agreement for Priority Sector Lending

with Indian Bank, one of the largest public sector banks in the country. The lenders recently

signed a MoU under RBI’s CLM, significantly expanding the portfolio of lending products

available to the target customers, increasing their access to credit.