WHat will happen in FUTURE is anyone guess / projection and monitorable but one thing that clearly emerged out of this results is even Rashesh Shah have least/no idea of what is going on.

From last 3-4 qtrs and every concall he kept on assuring that provisions will never hit P&L and it can be absorbed from operating profit. Every quarter he kept on reassuring the ceiling on provision that can hit earning. In Fact he started talking of growth from FY21. Covid provision to any extent is understandable but in matter of 1-2 months just see the provision spike from what was communicated and what actually came out. Disappointing. A person at the helm just showed he himself has no idea of the business or clearly he is not a man of words.

Secondly , He keeps on selling assets and stakes of good subsidiary every quarter for fixing bad.

Agan , earning hit and misses are part of business life cycle but the aspect that was most embarrassing is “Management NOT walking the talk” …

Forget Rashesh I don’t think anyone has any clue what lies ahead. I have not seen any real estate financier to be overly negative on the sector but mr. market knew better. Similarly any recovery will be swift and equally sharp when mr. sees no mortality risk. Have you not seen most folks saying real estate market has bottomed and yet prices are inching downwards still. There is no crash for financiers to be worried about but crash is visible in sales velocity which has created fear driven negative feedback loop. Folks with lack of own cheap funds got caught in a very bad cycle but this could be about to turn when you see that mortgage rates hitting 7% in the medium term. Suddenly it would be wise to own houses rather than rent them and this was clearly articulated by our PM. So govt. will let prices fall and interest rate fall for it to be affordable.

The total loan book of Edelweiss has shrunk from 32kcr to 19kcr. Rashesh on BQ said they have moved wholesale to AIF based and a few has been sold off(4kcr last week).

Anyone has details on approximate amount moved to AIF ??

I think all bondholders should be positive… He mentioned in the call today that when he has free cash over the next one year, they could initiate bond buyback. I think all bondholders should stop worrying about cash crunch from now onwards. Most of pain in wholesale and retail portfolios is already taken.

Honestly this measured approach by Edelweiss is reassuring. Its like the devil is now known. I see the street rewarding conservativeness in these tough times over the next few months

As a bondholder, I would still worry about credit costs ballooning way beyond expectations going ahead (unlikely, but possible).

But I take comfort from the fact that the other businesses seem to be doing ok, and hence can somehow help the credit business meet its obligations in an extreme event. I know Rashesh Shah did mention in the call that all the entities are ring-fenced, but still…

I still wouldn’t buy equity just yet, at least as long as debt is selling at good yields. Maybe some day I will switch…

I have never seen any positive environment in Edel call over the last two years but he sounded positive today and growth would be back from December onwards barring any new macro event. Secondly there will be demerger of valuable wealth and asset management biz in the next 12-18 months. Honestly, it has given me enough sleepless nights but it is time to stop doing that now. Wholesale book is down to 8k cr on 31st March and now 4k cr of sale in H1 would plug the minefields. He also said that there will be recoveries from these impairments 2 yrs down the line. It is time worry about growth going forward,IMO.

Impairment of ~2300 crore on a loan book of ~13000 crores is very big, the model of financing under-construction real estate has failed badly. Wholesale lending in itself is a risky business model with very little margin for error. It’s good that the company is trying to go for an asset-light model which in hindsight should have been done earlier (like MAS Financial). Will have to watch how the story of this transition unfolds.

Their wealth management business has been doing fine, they should try something on the likes of IIFL ONE to get their transactional assets under managed assets to get a continuous stream of annuities. Assets under their mutual fund business have been showing low growth (not counting Bharat Bond ETF), looks like everyone is investing in Axis MF schemes these days. ARC is a good business and can be scaled up given the amount of NPA in the banking system.

Life Insurance business has been making losses and is a sub-scale business, most of the incremental market share is being taken up by the top 3 insurers, may need more banca partnerships to grow. General insurance is a very small part right now.

Overall, the management has under-delivered over the last 5 years and many have been doubting their capability to actually scale up the business, need to see how they build from here on.

RJ increased his holding in Edelweiss to 1.19% from 1% while long term insider Jatin reduced it below 1% or exited. Overall retail holding has increased too while FIIs reduced.

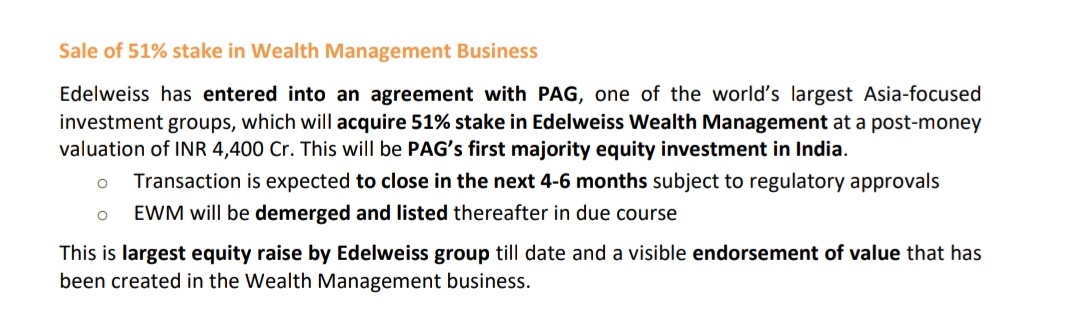

Let’s wait for announcement and actual valuation multiples. If the valuation being quoted is true it would make it clear that they are selling at distressed valuation to survive for the time being. A final blow to anyone who thought they could manage the wholesale biz and avoid mortal blow. May be this is the final deep operation but would also make investors long term patients. The whole recovery was based on asset light model of advisory biz and it is game over if that goes.

Now that ARC business has been made as a separate entity as per last quarter concall for the reason being as you mentioned , making EGIA an asset light model.

Based on the investment by Kora last year , the combined value of Asset,Wealth,ARC stood at 8000c.

Now if PAG is paying 2500crs for 51% stake in EGIA seems reasonable, considering ARC business made a separate entity.

My point was that it would become very difficult to recover from huge slump if you part with family silver like this. Holding company would be left with ARC, NBFC and Insurance. It would be long road to recovery from here in that case since they won’t be making profits in the near term.