They have been able to sell 1000 crore of these loans to the fund. I believe they had been speaking about starting a real estate fund for sometimes now and should have sold these loans to them

Edelweiss Q3 Results!

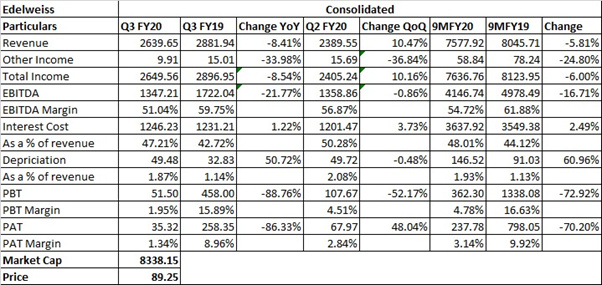

Q3 FY20 IP:

Q3 FY20 CC:

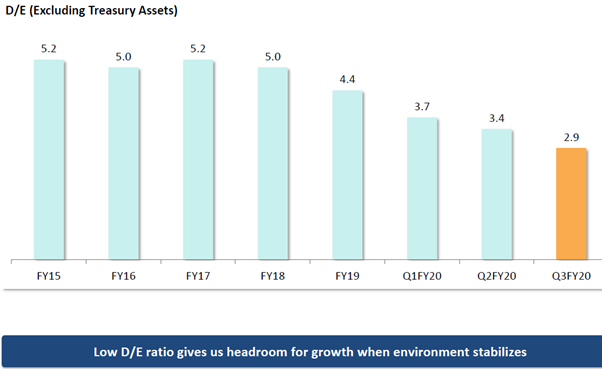

So in this current quarter, the quarter that got over, Q3, we had said that we will focus on strengthening balance sheet, managing liquidity and reducing the wholesale book. We’ve continued on that. On our balance sheet, we strengthened our equity base and now the DE ratio has come down to 2.9x, with a capital adequacy of 21.4%. This is largely due to some reduction in the assets, but also equity infusion from Kora and Sanaka in our advisory business, EGIA, which came in this quarter. We also in this quarter sold down part of our wholesale book to our South Korean partner, Mertiz, and that also brought down – reduced the debt-to-equity ratio.

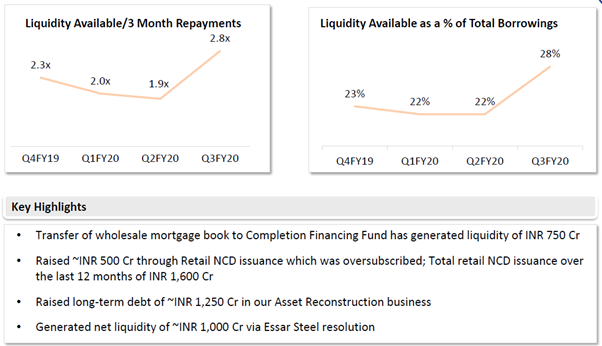

On the liquidity front, we have now more than INR 10,000 crores of liquidity, which is about 22% of our total balance sheet size. We’ve always said we want to be between 15% and 20%. And last quarter, we made repayments of about INR 5,000 crores. But overall, I think liquidity conditions have improved, but we have also strengthened our liquidity in the time.

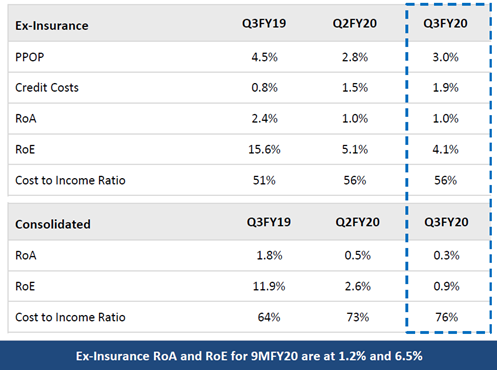

On the earnings front, this has been a muted quarter, which is there. We had ex-insurance profit after tax of about INR 74 crores, which has come down. Largely, this has been due to elevated credit costs, both implicit and explicit. And as we’ve been guiding, I think credit costs have remained higher, and I’ll speak about it as we go along. But I think, credit cost continue to eat into earnings as we go along.

Our wholesale books – reduction of the corporate book remains a key priority. And this quarter, we did INR 1,000 crores of sell down. We plan to do a lot more in the next 2 quarters. In fact, we have announced it. At the Board level, we have decided that we will pursue these opportunities more aggressively. We will do 2 to 3 transactions on various parts of our wholesale book to sell down because currently our wholesale-retail mix, which is about 50-50, we want to, in the next year, end up at about 70-30. For that, we will have to do aggressive sell down of the wholesale portfolios and we are having discussions with investors on that.

In order to do that, we have also announced that we will do a review of the ECL model and try and come up with a very transparent approach to this so that when we sell down the portfolios, we’ll be able to clearly demonstrate the pricing at which it’s sold down, what is the ECL on the residual book and all of that. Because one of the things that has happened in the last 1 year for all of us because an ECL regime is very different from an NPA regime. NPA regime is a lot more deterministic, that something is an NPA and you provide on a formula basis. In ECL, there is a lot of judgment, forward-looking, that is there, and what we have found is largely ECL calculations have been impacted by liquidity environment. Even today, whatever delta on ECL has been there, 80% of that can be explained away with liquidity. And by selling down this wholesale book, we are also planning to generate liquidity, which itself will allow us to make sure that we allocate liquidity for projects to be completed and manage ECL as a result of that, because the ECL is largely getting impacted by whether you can provide liquidity to complete the projects or not, especially in real estate. And that is what our approach is going to be, that we constantly make estimates of how much liquidity we’ll be able to generate, we’ll give, we’ll be able to originate for those projects. And based on that, what the ECL is going to be.

So we plan to do this in the next couple of months and then do the portfolio sales of wholesale book on that basis so that there is very transparent pricing. Because we will always ask that when you sell down your books, are you selling down the good book? Are you selling down the NPA book? And at what price you’re selling down? So by doing this ECL model review and [yearly] showing the pricing in a transparent manner, we hope that we’ll be able to give comfort to all stakeholders, not only on the sell down, but also on the ensuing book after that. So we expect to do this in this quarter. And our hypothesis on liquidity has improved in the last 3, 4 months, but it’s still a lot tighter in the environment, and we are seeing more and more projects getting affected, more by liquidity. The government has announced the last mile completion financing scheme, which has been a fairly good development. We are hoping that by March, a lot of disbursements on those start also happening. By selling down the wholesale book, we will do multiple things. We’ll change the composition of our credit business. We will generate liquidity to pump into completion of some of the projects. That’s what we did in the Meritz deal. Out of the total money we raised, we kept part of it for completing those projects out there. So we transferred about 7 projects into that fund. And for those 7 projects, whatever last mile completion financing was required, also came from the fund. So that allowed us to ensure that we could have clear visibility on last-mile financing fund. And thirdly, it allows us to step up our disbursements on retail, which we remain very excited about.

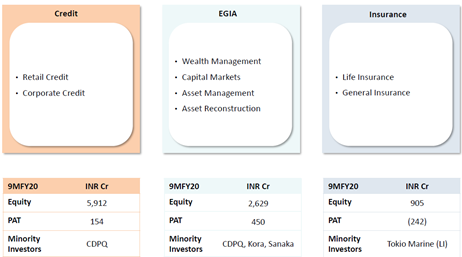

Group Structure: We have raised equity from various partners. And the way – our ambition is to run Edelweiss as 3 businesses, Credit, EGIA and Insurance. Insurance, we only have a partner that’s stand-alone. I think in EGIA, we have investors now. And Credit, we have investors. We would like to make these 3 as independent and reduce any other things underneath that. Now the ARC is the legacy issue because, as you remember, when we started the ARC, RBI rule said that you can only own 49% of that. So that’s a legacy element that is still there. But outside of that, our idea would be to streamline everything under EGIA and make EGIA as a well-capitalized, independently governed, strong entity. And the same thing about Credit and the same thing about Insurance.

Disclaimer: Invested

4 Likes

Anyone still tracking this? CMP around 30!

What is the probability that the company will not survive a couple of years from now? Will the credit vertical losses put the other businesses at risk? How can they navigate this? Sell stake in insurance/wealth management/etc if needed to shore up liquidity?

I am invested here for more than a year; yes, Edel is being priced for default.

- Even assuming significant losses in the credit, ARC & LI (the General Insurance business is just starting out), I do not think survival is an issue.

- There have been multiple allegations – Kohinoor and Capstone are well-known examples. Nothing materially adverse has come out of these.

- They have the benefit of counter-cyclical diversification – the ARC and the various funds managed under the Alternate Assets (AA) business.

- They have brought in outside investors in both ECL Finance and EGIA in the last year or so.

- They have been selling down the Corporate Credit book to funds managed by the AA business.

- The last two measures have significantly reduced the DE ratio and have ensured ample liquidity.

Disc: Invested and adding; views biased.

5 Likes

1 Like

Hello guys, I’m new to this group. I’ve invested in Edelweiss before the bull run and missed cashing out. I continue to hold the stock with losses (@ 86). Now the stock is trading at 0.5 times the book ( there is no clarity on the quality of the book, this quarter there could be some clarity post the ECL method). The GNPA’s have reduced in Q3 vs Q2 FY20 (marginal), due to selling down of corporate book. Management’s actions seems to be in this directions and they hope to ramp it down in 2/3 dealings. These are being put under AA vertical. So, in the coming quarters , I expect the credit cost to reduce in FY 22 and lot of profits are back ended in AA vertical. I’m not able to quantify these numbers.

In Retail credit, they’ve put EI’s for DHFL retail assets bid. Its difficult to say, whether the deal goes to Edelweiss or not. They would continue to grow Retail book, probably in H2 FY21.

In Distressed credit, its a good business with good ROA & ROE. I think , we could not expect steady stream of income every quarter ,but to see it a YOY business.

In insurance, Management expects it to breakeven by FY22. I’m little pessimistic on this business, there are no operational improvements I could see. I feel ,its better Management sell this business ,if they get a good valuation.

In Asset management business , there is no issue as such.

These are some of my thoughts . Hoping for fellow members inputs…

3 Likes

2 Likes

Rashesh Shah On Impact Of Covid-19 On NBFC Sector:

5 Likes

Hello,

Can someone please explain this board meeting resolution passed today.

d85396cd-fee8-4dc3-a0f3-eb4ba9dbd211.pdf (90.4 KB)

What is the purpose of this.

Thanks

1 Like

They are increasing borrowing limits so as to allow them to issue more debt.

In this case they have to meet obligations of their redemptions and they may have had to give a majority of customers moratorium while they may or may not have got the same from their lenders,any way they have to maintain adequate buffers to meet redemptions on their other existing debt like NCD’s until normalcy is restored.

Regarding the Divestment proposal,if you listen to the above interview,Mr Shah is talking about raising equity by selling some stake,so the board has approved that proposal which will be be voted on by shareholders via postal ballot.

(a) to increase the limit to make loans to any person or other bodies corporate; give any

guarantee or provide security in connection with a loan to any other body corporate or

person; and acquire by way of subscription, purchase or otherwise securities of anybody

corporate, from Rs. 10,000 crores to Rs. 20,000 crores, under Section 186 of the

Companies Act, 2013; and

(b) divestment/ pledge or creation of lien on / dilution / disposal of the Company’s

investment(s) / asset(s) /undertaking(s).

@sarthakkumar19_ My take on this is - due to Covid and its cascading impacts on the customers of Edelweiss ( both prospect and currently active ) - increase the opportunity to lend more, so that they can sail through this turbulent times & at the same time make opportunistic bets by taking a stake in the company of the customer if they are not able to repay (more like collateral conversion/liquidation) their installments/ principal. This is the positive spin on it… the negative spin on it is, there is pain in reality out there in the market, given all the lockdowns, shutdown of factories, businesses thus impacting sales, etc. -they are providing higher coverage/loan capacity extension etc - since repayment on time might be harder for their clients. Please check the above link interview of Mr.Rashesh Shah - explaining the 4000cr payback and loan extension on their (Edelweiss) supply side (i.e., their liability) v/s the moratorium application on their asset side. (NBFC space). How many % of their clients have asked for the mortarium …

on the second point (b): i think its regarding their ability to create liquidity from their current investments & assets on their balance sheet by divesting, pledging, disposal etc. & also selling some stake in their company for equity.

Also note that with the govt trying to pump in money to NBFCs, you heard Mr.Shah say that - they will have to wait and see how much of it will come down to the NBFCs and how effective it will be.

Since, Edelweiss is a diversified conglomerate, they might be able to survive this turbulence even if one of their vertical (credit/NBFC) is having headwinds.

1 Like

Crisil Ratings update posted for Edelweiss: (Reaffirmed) https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Edelweiss_Financial_Services_Limited_May_25_2020_RR.html

1 Like

Hello. Any idea that when will the company declare results for the quarter ended March 2020?

1 Like

The draft regulation is put up before RBI allowing the players other than FIs in the process of securitization of assets. Do we see more competition coming in ARC business??

Experts views invited.

Seems they are finally ready to put the past behind and move on. Wholesale book goes down substantially albeit at big haircut. It is better to take a big cut upfront rather than bleed every quarter. I think they have already taken substantial write down out of total 1k cr. The residual loan of 7k cr in the wholesale book could be closer to book value and should be manageable going forward.

3 Likes

Hi Sumit. Thanks for sharing this.

Is there a way to find out which developers and projects form the remaining 7,000 crores book?

They have stopped giving that number on the basis of developers. They had communicated that one third of their portfolio was supposed to get OC by fy20 and another one third by fy21. We will know clear picture in the Concall. My only contention is that this is a manageable figure. This will help them regain credit rating and set out on the growth path as liquidity is abundantly available both from banks and now RBI back stop in the form of 30k Cr liquidity facility. They have not been growing their loan book for the last two years. This will prove to be blessing in disguise when their book value remains largely intact.

3 Likes

FY 20 result announced, and reported losses for FY-20 are 2045 cr. Whatever they have earned in last 3 years, most of it given up in just one year (or mostly last quarter).

No wonder they are reporting results on Saturday.

2 Likes

They have taken 2600cr worth of impairments in Q4 and some of it is preemtive while other required to sell down their wholesale portfolio. I think their PPT suggests they would reduce wholesale portfolio substantially if not to zero during FY21. They will not grow their book before exiting this sticky loan assets. We can debate about it but the fact is that they got caught in a wrong cycle. You had quick punches in succession from demonetisation, RERA, economic slowdown, income tax related changes and now COVID to their highest allocation i.e real estate lending. One needs to traingulate it with no backing from any known business group to understand the pain. To be fair they have decided to take pain upfront and end the bleeding. I think by H1 FY21 it should be ready to move on from their biggest mistake and hopefully demerge to unlock the value. It was priced for default and extinction but that risk is rapidly reducing IMO.

8 Likes

Does anyone know what is the ‘Reduction in ESOP book’ outflow of Rs 1650 in H1FY21? Slide 60 in investor presentation (Liquidity & Cash Flow Plan for FY21).

Is the company obliged to buy ESOP shares from the employee trusts or something?

1 Like