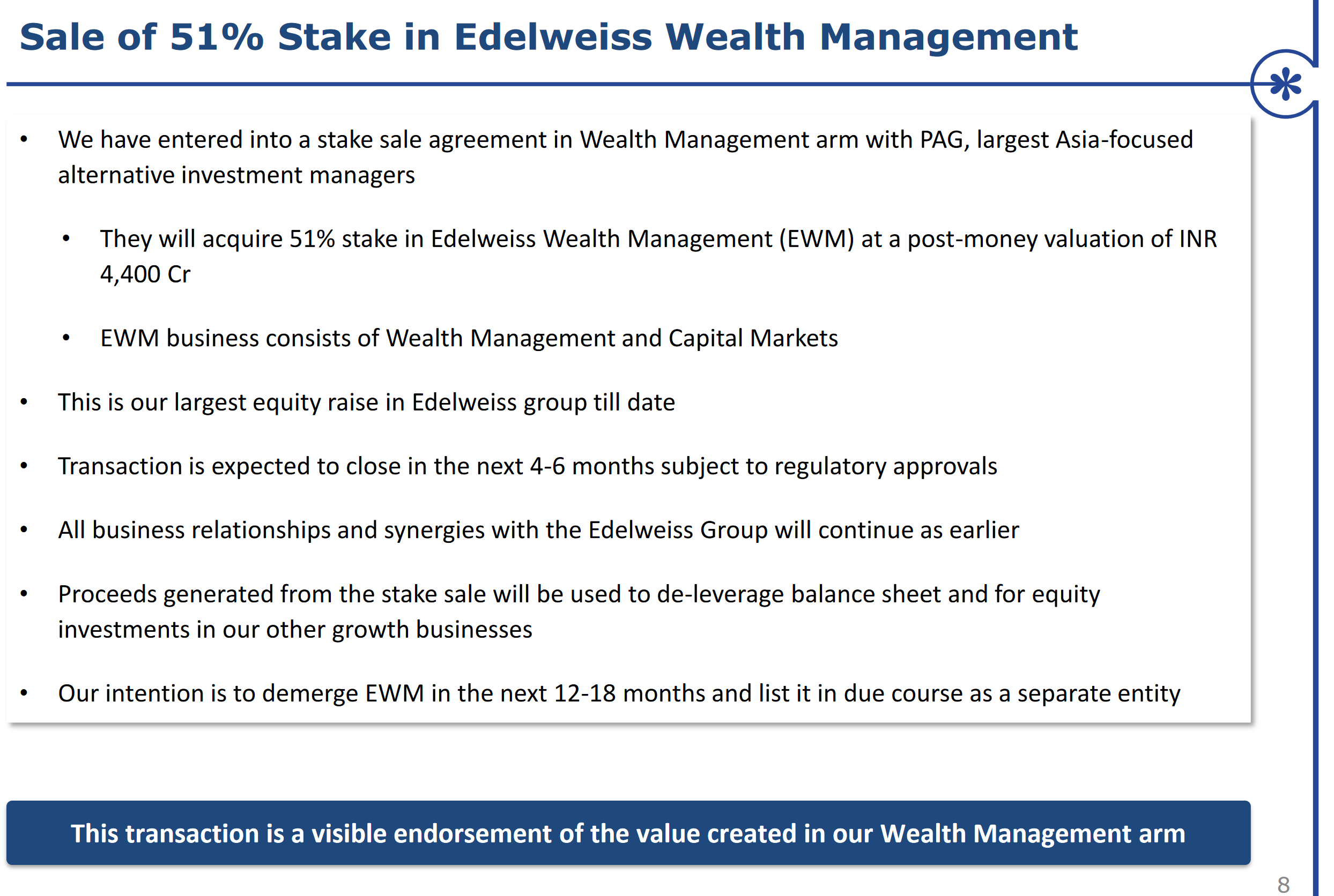

Please note that Asset Management, Private Equity, Private Debt, Mutual Fund and ARC businesses under Edelweiss are not part of the transaction with PAG. So Edelweiss is not diluting its stake from these profitable ventures.

There is a lot of great information and explanation especially around the holding, structures of deals with CDPQ, PAG, etc plans on Demeter, scaling of certain biz, impacts due to COVID, is clearly explained by rashesh shah on the conference call.

I would highly recommend to listen to the call…I have not had a chance to sit and take notes.

After PAG deal,The holding in wealth management will be ,51% by PAG, 40% - 41% with Edelweiss, and about 8% or so with Kora and Sanaka where only the first tranche has been taken and with this deal happening, our need for tranche two or tranche three have gone away,

We plan to list all 6 verticals of business separately going forward to unlock value ,In ARC we continue to own 60% and we own 100% of alternative asset and AMC business in asset management. Edelweiss Tokio Life we own 51% and general insurance we own 100%

On the valuation of the deal at 4400crs, we think the asset and wealth management business valued collectively at the benchmark of 8,000 crores based on Kora and Sanaka investments last year.

Out of the 2,000 crores that we are raising, we do expect that about 400-500 crores will be allocated for the next two years’ growth requirements for the asset management and insurance businesses.

We do not expect to invest in the credit business as the CAR is over 20%.

The balance part of it will go to the wealth management business

Another 800-900 crores will go towards repayment of debt at the group level.the group entity is more like a core investment company, it is like a CIC and we have a capital base of close to about 6,000 crores at that level and by RBI rules CIC can be geared 2.5 times, so on a 6,000 crore equity base, you can be up to 15,000 crores of borrowing. We currentlyhave the net borrowing of about 4,500 crores at the group level.

ARC business IRRs, as interest rates have come down, what was a 20% IRR earlier can come down to 18 or 19, but we have advantage of lower cost of funds also Current AUM is 45kcr

Retail credit business will be co-origination & securitization model with PSU banks and we wont be

leveraged for more than 3-4 times

Wholesale lending will be in AIF and asset management model.

The whole credit business will be based more on fee income model than on net interest income.

I was going through the valuation of HDFC asset management and Nippon asset management , both are trading at 13% & 8% of AUM respectively.

Considering the spin off Edelweiss Wealth management with an AUM of 1.25L and assigning a moderate valuation of 4% of AUM , we get a valuation of around 5000crs for Edelweis - PAG Wealth management entity.

I am just thinking loud here, would welcome views from others as well.

in my opinion, asset mgmt and wealth mgmt. are two different space.

you are valuing the asset mgmt. space of HDFC and Nippon with PAG’s stake in Edelweiss Wealth mgmt. You should probably compare this with something that does pure play wealth mgmt for apple’s to apple’s comparison. PS: I have not looked in to IIFL in detail, so please excuse me, but IIFL might be nearer comparision, but do note that IIFL does have an AMC with in it…

Would recommend a great presentation by Kedar @zygo23554 on this. You can read it here - VP Chintan Baithak Goa 2019 - Sector: Asset Management & Wealth Management

Thanks for mentioning IIFL wealth. Just went through IIFL presentation. They have 1.85L cr AUM along with 23k cr AMC business as you mentioned and PAT for FY20 is around 200cr. Mcap 8000crs

they sold part of wholesale lending book few months back after taking a big cut. what they have retained may be of worst quality with no takers

wealth management was their best business. And 60% of it is already sold out to Kora and PAG. And the money received is obviously disappearing into existing business in which not sure when value unlocking will happen

ARC book quality and valuations have deteriorated due to COVID-19 and so they over paid for this book in pre-COVID era

no clear path to unlocking for other businesses except wealth mgmnt. Wealth mgmnt on being listed will not benefit much to existing shareholders as they now own only 40 odd %

in the call mgmnt mentioned that they may do demerger or an IPO of wealth management. IPO will be not rewarding for existing Edelweiss shareholders

So net - net there is value but there is lot of uncertainty as well. And 60% of the best business the company has lost and the money so received is disappearing in existing businesses

Invested and recently sold out so my views can be biased/wrong!

Would like to know your views as you track edelweiss quite closely and prtty versed with details?

time and again they demonstrate that they can raise capital and on the other hand execution is an issue … your comments on how you see business shaping in next 2-3 years

There is absolute lack of interest in the stock and rightly so for almost blowing the whole biz model. The only thing that will work is demergers/spin off and listing. There is no doubt that there is good amount of value but the market would focus on earnings. At operating level they have created very good entities like ARC, Pvt Debt etc but some others are bleeding heavily. They need to come out better at an aggregate level. Analysts have downgrades and there have been few upgrades too.

Coming to this piece of news - this is surely positive and would potentially add 60cr worth of annual PAT for the period these funds get managed by Edel. I certainly think their real estate lending PF is past the pain but would wait till March 2021 to take a call.

60 odd cr would only be the management fees. There will also be a performance fees subject a particular hurdle rate. Interesting point here was that of faith of investors around the world in times such as this. Speaks for their ability.

In other news, Pabrai funds more than doubled their stake in the Jul-Sep qrtr from 1.4% in previous qrtr to little over 4%.

This is a mess created by regulators. They allowed this fraud to happen over a period of a decade or so. Now think about this - a thief steals gold and pledges it to a lender. Lender liquidates it after default and then police arrives. In place of catching thief, they catch the lender since it is easy to do so. Under no circumstances a custodial service and a gold lender could verify the ownership of shares/gold if it was pledged following due process. It is impossible to do due diligence for a gold lender but SEBI must have clamped down in case of brokers and they had means to do it.

I would say that this case will go upto the supreme court since the amount is large and there are multiple parties involved Edel, Axis, Bajaj in these types of cases.

No, I think there are some grey areas like the shares were owned by the investors who gave power of attorney to their fraud brokers unknowingly. Now the regulator must have intervened to stop the onward pledging activities. Since this is a larger public interest matter, it will be tough for any counterparty till it reaches to the supreme court. It will hit the credibility of institutions so now they are behaving differently to save the face.