Hello friends, In try to anslyse stocks , I often come across a metric called EVA( Economic Value added) . I have also seen the same in Pidilite’s anural report. Could some provide a writeup on it ? Is that worth exploring ?

1 Like

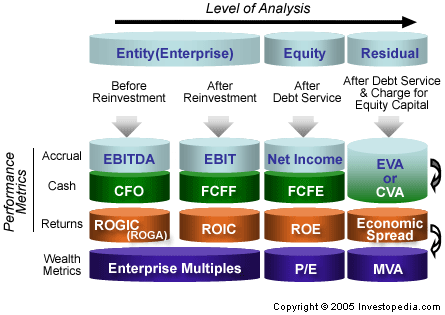

Hi Saurab, EVA is one of the two methods I use in valuing a company. I think it is among the best methods out there (After Modigliani Miller), the interesting thing with an EVA is that upon performing a discounted EVA valuation, you will (if done correctly) arrive at the exact same answer as that arrived at through a DCF.

A simple explanation of EVA as a concept - The main point here is that growth by itself does not add value. It is only valuable if its incremental returns are higher than it’s incremental cost of capital.

Example - Company XYZ has a cost of capital (WACC) of lets say 12%. It’s return on capital employed = 15% and it employs 1000cr of capital. the value added therefore = 3% (15 - 12) * 1000cr = 30cr.

An interesting point to note here is the same company XYZ, if it earns an incremental return of let’s say 11% on growth, that growth is actually value destroying. Why would companies do that, you may ask? Simple - because they are transfixed on EPS.

Example - Company XYZ can borrow at 9% (cost of debt let’s say) and can earn a return of 11% on that borrowed capital by investing it in the business. So if a company borrows let’s say 500 cr. their EBITDA will increase by 11% x 500cr & their net profit, EPS etc will also optically appear to grow at some % of that incremental 500cr.

So while optically their earnings look great, EPS growth, EBITDA growth etc. they are actually destroying shareholder value. You will be surprised how often this happens (In my reckoning nearly 30% of all companies in the NIFTY (Supposedly blue chip) companies) indulge in this, and their managements are hailed as great.

Take RIL or any other company of your choice as an example. They barely earn 9% on their capital employed. Clearly the cost of debt itself is itself 8 - 8.5% + the cost of equity (let’s say 15%) With a D/E ratio of 0.6 , WACC is approx 12 - 13% (All numbers are approximate)

So does it make sense for RIL to grow, by investing in expanding their current business if it only earns 9%? Sure their earnings will grow, their EPS will grow etc. But they aren’t even earning their cost of capital!!

That’s why people use EVA as a metric, because what shareholders care about (or should care about) is not earnings growth , but how much incremental value the company adds.

Hope this helps.

15 Likes

Omg rks. That was an awesome reply . I am indeed thanks to you. I did not expect a reply so early. I have collected some material on EVA and would love to share it here with you. With your efforts and if other join in we can make this EVA thread a great place to learn.

Yes , I too have read the arguments in favour of EVA and they are pretty impressive . we need to calculate EVA of Indian companies correctly . would you like to take the initiative. I will give whatever limited knowledge I have abt EVA.

Also thanks abt the miller approach . I am curently reading earnings power box and EVA

While EVA is the right way to measure things, it is really not as path breaking as it is made out to be.

EVA is better than EV/EBITDA or P/E or P/S or P/BV to value companies.

But it is just DCF in a new bottle. To be specific DCF after removing Opportunity cost in a new bottle.

Found a couple of good artcicles on EVA and DCF

http://www.valueadvisors.com/Attachments/OByrne-JACF122.pdf

do read

Yeah, sure. Would love to contribute in whatever way I can.

Sriram - True, As mentioned earlier a discounted EVA and DCF will yield the same result. and you’re right eva is nothing but a dcf that takes into account capital costs.

However EVA and dcf still share a common problem. They require one to make projections into the future, and discount future earnings to today. So the final answer therefore is highly sensitive to the assumptions made.

And to be honest how can someone (sell side equity research analysts) possibly claim to forecast a company’s capital structure 5 years from now? Or anticipate growth with a reasonable degree of accuracy 5 - 10 years out. In 2002 if someone told me that 5 years from now, even the most economically disadvantaged people in India would have a cell phone, I would have called them crazy. So if I were trying to do a DCF or an EVA analysis on Airtel, I would have been wrong by a lot.

My personal view on valuation is that no matter what one does / method one uses, their forecasts / valuation will be wrong. So i just use it as a go - no go filter.

Can’t agree more. Will summarize it in a different way for the benefit of future readers

- DCF / EVA / Any valuation measure is a scientific art. It is neither science nor art.

- No investor gets rewarded for estimating the value accurately. It is not like predicting scores.

- You get rewarded / penalized for the Go-No Go decision at a particular price.

- You get rewarded / penalized equally with a guy who values differently (read different assumptions and projections) the same stock for the same duration.

- The value you estimate just gives a rough idea of the margin of safety from the price. Nothing more than that.

3 Likes

DCF and EVA are future predicting models , but as u say that we need to know future for it , if i knew future then i wud have bought a truck load of stocks . But sadly that wud requide a boon from Gods after years of tapasya…

So what we do is try to predict the future and also know what factors are there that might affect my future projections negatively .

EVA and DCF are just models to do so

Hi seniors,

Does that mean EVA=ROCE-WACC. Can you share where can I get EVA data, quarterly or yearly for Indian companies. If I assume WACC to be flat 15% then any company having ROCE> 15% would generate +ve EVA. Is that correct way of thinking. Also why is it that cost of debt is 9-10% and cost of equity is 15-18%. This will encourage to take huge debt as co can show +EVA as WACC will be lower than ROCE.

I am a learner thus getting bit confused

Anupam,

I believe our current calculation of returns in India in automated software is not correct for the following reason. Hence the hurdle rate has to be corrected for this anomaly.

Take two companies having 100 crores profit - One with 20% dividend payout ratio (avg pvt sector) and another with 80% (good PSUs) have effective return of 96 and 84 crores after reducing their DDT of 4 and 16 respectively. ROCE calculations in US assumes dividend tax in the hands of the owner whereas in India it is different. Whether it is good or bad depends on your personal tax rate.

Then comes CSR of 2% on 3 year avg PBT. I am still not clear about its accounting. Can anyone help? Is it shown as an expense? Else it needs to be taken out of ROCE again.

Anupam,

You need to have right balance of debt and equity. Most Indian promoters and bankers prefer as less debt as possible. Higher debt also mean higher cost of debt as banks looks at previous debt and operating cash flows of company while deciding at which rate the loan should be provided. After a company reaches a particular threshold it tries to repay debt to increase PAT and Return ratios so increasing debt wont reduce WACC after a certain limit. Lastly cost of equity is also dependent (although indirectly) on how much debt company has as lesser the debt lesser would be the cost demanded by equityholders.

1 Like

RKS,

In the example, when co xyz borrows 500 cr @ 9%, then WACC will also come down. It will not remain at 12%…may be 10%. Then with 11% return, its still value adding. Then wheres the issue/problem ?

Would be great if you can share the calculation in excel… of ebitda growth, eps growth but EVA as negative…it will be helpful in understanding.![]()

BDW, found a conceptual framework to look at EVA.

3 Likes

Hi Anupam,

Thanks for keeping this thread alive. In response to your question -

A. I probably was not clear in my previous post, my bad. What i meant was lets say the initial state is a D/E of 1. i.e for the sake of example total debt = total equity = lets say 1,000 cr. and a cost of equity 15%, cost of debt 9%, tax rate 25%. (Again these numbers are just an example for illustration purposes) The WACC now would be 11%. If the said company now were to raise it debt by another 500 cr, the WACC would come down to almost 10.25%. Basically, what this means is, If i raise & deploy incremental capital at a cost of 9% and earn a return in excess of 9% (and less than WACC of 10.25% lets say 10%) my EPS will go up, while I am actually destroying wealth as I am not earning my cost of capital. Specific examples are in the link below.

http://www.publishingindia.com/GetBrochure.aspx?query=UERGQnJvY2h1cmVzfC8xNzE0LnBkZnwvMTcxNC5wZGY=

Please note that the links shared does not contain work done by me, nor have I reviewed it personally, but I am sharing it here as it may give some real world examples of Indian companies. Please note that the documents pertain to the time period of 2003 - 2012.

http://www.scribd.com/doc/51396384/Economic-Value-Added-EVA-of-Sample-Companies#scribd

B. Moving on to a much more interesting discussion though, about your statement - " when co xyz borrows 500 cr @ 9%, then WACC will also come down"

While you are right, that adding incremental debt will mathematically reduce WACC (or so we have been taught in B school & Accounting) as a student of economics I would dispute it.

Think about it, what is WACC in simple English? What does the cost of equity mean in simple English?

The cost of Equity - “is the rate of return required by the company’s ordinary shareholders in order for that investor to bear the risk of holding that company’s shares.” Source Investopedia.

Let’s break down what they mean by "investor to bear the risk of holding that company’s shares."

There are two kinds of risk, business risk (i.e. the business may do well or not) and the second is financial risk (associated with claims on the underlying business assets)

Does it make sense for the cost of equity to remain constant by increasing debt (and thereby financial risk) ? As a shareholder shouldn’t I be compensated higher because the business I own is taking on additional financial risk? Or another way to put it is, should the cost of equity for an unleveraged (debt free) business be the same as that for a highly indebted company? Most economists would think not. According to M&M, WACC would remain constant almost, as increased leverage would increase the cost of equity.

I might be highly biased because the B school I went to is highly influenced by the teachings of one of our former faculty members, Merton Miller. While the below wiki link does a huge injustice to what M&M really said it maybe a good starting point. Link below. Hope this helps.

2 Likes

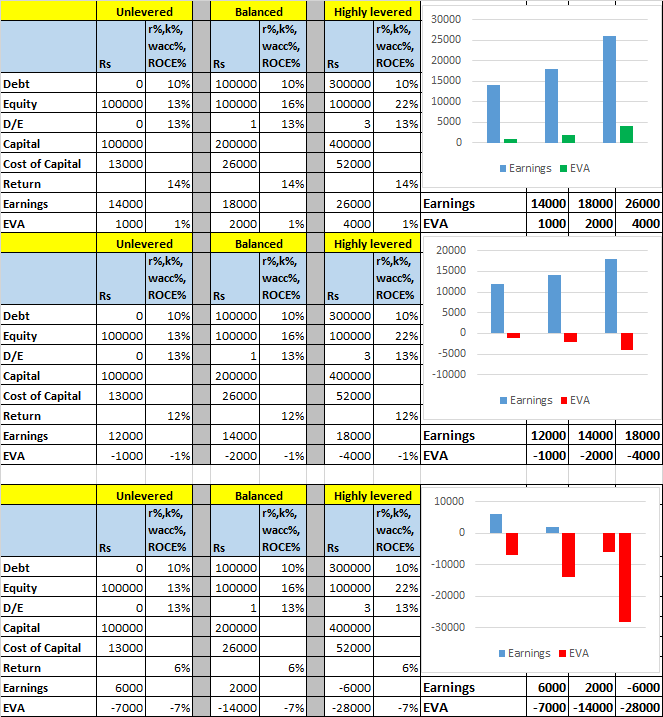

Tried to quickly simulate what it looks like…just for understanding

from unlevered to highly levered- wacc% doesnot change.

1st & 3rd scenario are easy to understand- clear Go & No-Go. But 2nd scenario is apparently enticing but ultimately value destroying. Most of the large companies like Reliance, Airtel, L&T, etc are in 2nd category.

2 Likes

Great stuff Anupam! And you’re right, a lot of apparently “blue chips” fall In the second category. An earnings growth of 50% from unlevered to levered case (12,000 to 18,000) is still value destroying, but most analysts still only follow EPS. Thanks for the visual representation.

Hi Anupam,

Great insight, Could you share the Excel template you used for investors benefit.Thanks.

in EVA, what we are doing is EVA , the equity is not considered free , it has a cost attached to it. Just like a company pays interest to a bank , similarly it should ( though it does not ) pay to the equity holders. Reason:- people have put money in the company to earn profits more than they cud have got in the banks FD and so on.

So it like this. A companies PROFIT should be large enough to pay the banks and equity holders .

NOW profit in EVA terms is a bit different :- it should not include extra ordinarary , etc . There can be around 160 adjustments to the profit ( called NOPAT :- net operating profit after taxes) as per stern stewart in his book called quest for value. anyways in indian companies we do not need more than 5-8 as more than that wud just be fine tuning .

eva= EVA = Net Operating Profit After Tax - (Capital Invested x WACC)

we can further break it up . but that we wud do as a step 2 as to which components are contributing or destroying the end result

1 Like

since many items from the profit generating side wud be eliminated so corresponding entries as to capital required to generate those profit items will also be eliminated from the capital invested portion

So how do you calculate the WACC or do you take it as 12 or 13%?