No i normally compute it, but since we are talking of being strict here, so , if someone is not keen to calculate , we can take a standard value depending on the companies debt to equity

saurabhkurichh

Can you show a sample EVA calculation of a live company- lets say Bharti Airtel / TCS etc

I tried - but my accounting knowledge is not good enough. Please correct, better help us with a demo calculation.

Assumptions

- Operating Profit- tax= NOPAT

- total Liabilities= Capital employed

- Debt Equity of nearly 1, so (10%+ 18%)/2= 14% is the WACC

- NOPAT- WACC%*(Capital Employed)= EVA

Yes wud definately show and bring forward. I am not an expert in EVA too, wud be nice to learn from all of you. Its a exicting topic though

I would request all to go through this site

https://www.stock-analysis-on.net/

here they analyse one company daily . So on weekends can break our heads together. today they are on to walt disney

2 Likes

template creating wud be very easy.I am sure @amishra would do it for us . in the mean time we need to set the basics right

EVA is towards the ending portion

https://www.stock-analysis-on.net/NYSE/Company/Walt-Disney-Co

Team !!

I will create a basic template to calculate EVA in excel and share. It would have formula linked.

However I need all of your inputs on the correctness of formula. NOPAT, WACC, D/E, capital employed etc has to be correctly calculated- need help from guys with good knowledge on financial statements and terms.

I believe EVA though looks theoretical approach. But I am convinced in the real long term 5 years or 7 years plus horizon a stock value won’t compound if the co. is not EVA+ and EVA growing. Short term is anybody’s guess.

1 Like

May be you guys want to look at the discussion on Economic Profit Added in the Art of valuation thread

http://forum.valuepickr.com/t/the-art-of-valuation/?source_topic_id=3332

1 Like

The most commonly used simplified Capital Employed = Total Assets - Current Liabilities

yes but in EVA capital employed is a bit different .

thanks @akbarkhan … wud have a go through

Wonderful to work as a team

wud be sharing the eva resources that i have

EVA-basic. printed.pdf (484.5 KB)eva (2).pdf (287.1 KB)EVA Example.xls (166.5 KB)EVA_Frank_Pinto.doc (64 KB)

eva.pdf (108.0 KB)evaspres.pdf (42.5 KB)

EVA-basic. printed.pdf (484.5 KB)

eva3.pdf (237.4 KB)EVA-runko32 esitys_e.ppt (1.2 MB)

2 Likes

HI Saurabh,

Thanks for the links. I had the privilege of studying under Joel Stern a few years back, he taught us Finance in B school. Will share my notes from class soon. Incredibly eye opening stuff! In the process of moving to Tampa from Pittsburgh so please excuse the delay. Thanks again Saurabh, appreciate it!

2 Likes

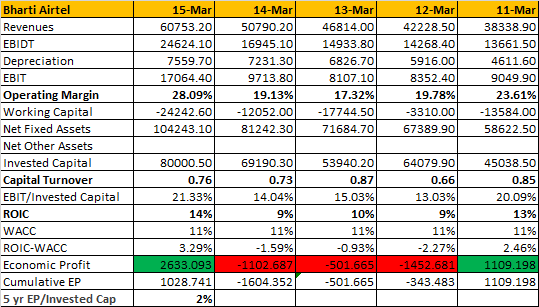

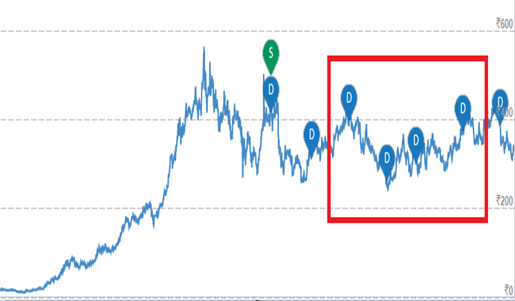

Hi,

EVA calculation & correlation with stock price from 2011 to 2015. Its for bharti airtel. It shows low EVA results stagnant stock price. Would be great if similar correlation between EVA & CMP (+ve or -ve) can be sampled across few large/mid/small cap stocks from various sectors.

2 Likes

Just found this thread while searching for something else. I thought I’d leave my two cents on this.

How would you treat a company with lots of liquid cash in its Balance Sheet? No, not the Operating Cash items (Loans given to employees, Deposits with the Tax Department, Cash blocked for purchase of Inventory etc), but I mean the really liquid cash like Cash/Bank/Bonds and Mutual Fund/Equity Investments.

If the company is prudent with accounting, the gains from these will not show up in the Operating Profits of the company. More often than not, these show up as ‘Other Income’ and so on, which should ideally not be considered while trying to Value a company.

I personally define ‘Capital Invested’ as (Total Fixed Assets + (Current Assets - Cash - Cash Equivalents) - (Current Liabilities - Deferred Tax Liabilities)). In essence, I remove Cash & Cash Equivalents from the “Capital” of the company and add it back separately once I’m done Valuing the company (While being careful not to include the gains/income from these in the profit of the company). This boosts the company’s capital turnover, at the downside of these additional Assets treated at face value and nothing more.

I’d love to hear the thoughts on this from some of the seniors in this forum.

Edit: Found an old blog post from Prof. Damodaran on the topic

Also a paper on the same (Impact of Cash and Cross Holdings on Equity Investors):

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=841485

This will be an interesting discussion.

My view about this is that one should study the track record of the co in deploying cash. In some cases excluding cash is a better way to value the co but in most cases cash is just capital invested earning ok returns for the time being. Keeping excess cash or equivalents for an elongated period of time and piling it up depresses the value of the co. Some cos like thyrocare, goodyear, HMVL etc come to mind.

In India, cos have a tough time scaling up because of our large, ingenious and flexible unorganized sector and often grow upto a point and then stagnate. Its much more difficult to grow a business in india than is commonly thought and after a point cash reserves tend to pile up as opportunities to grow dry up.

India is made up of a lot of small opportunity sizes which can absorb only so much capital and the rest is either destroyed in cyclical turns or sits on the balance sheet or is employed in some non productive fashion by the business. Returning it to the shareholder is the last thought that occurs , if it does at all.

For this reason, i view cash as risk capital until is transferred to the investor.

2 Likes

Interesting. So do you mean that you will also demand the Required Rate / Cost of Capital on Excess Cash?

Say, the company has Rs. 100 Cr in Cash. In the regular sense, it earns at the RfR (Say 7%) and being liquid, we demand the RfR, so it remains at face value in the Valuation i.e. 100*0.07/0.07.

Do you say that the Rs. 100 Cr earns the RfR, but you demand the Cost of Capital? Does that mean that, if Kc is 12%, you will Value it at Rs. 58 (100*0.07/0.12) Cr?

Yes, the required rate of return is 15% across the entire capital invested stack

Thank you for your inputs. One final thing then… how do you view Mutual Fund / Bond investments? They may already earn close to the Kc. So does it make sense to mark them down or retain them at face value?

Itna kaun dimaag lagayega. Technically one can mark them up or down as you suggest but itna deep i dont go.

From your posts i gather you follow Damodaran closely. He would certainly do something like this and technically he and his students would be correct. I just lagao 15% and if things look good i dig further.

2 Likes