A personal experience with ClearTrip vs others for flight bookings. ClearTrip was running promotion of fully refundable flight cancellations at 99 per person per ticket. This is very helpful in post pandemic uncertainty. I personally made use of cancellations.

After couple of months they have increased cancellation option price to around 300 per ticket. MMT and Easmytrip are charging 500-800 for same facility. This is big advantage ClearTrip has got right now and it will surely drive sales away from other players.

See, one indisputable fact of this industry is that there is very high competition here. And this has probably already been baked into its valuations. If this company was in another tech based industry it would have got significantly better valuations, with the level of growth it has delivered.

What you and all its critics need to note is that it has grown to become the number two player without much funds and in a very planned manner. Here, you need to appreciate the capital allocation efficiency of the management.

As for market share gains, now they have started to aggressively advertise their brand. Before, they only focused on getting their name advertised on Google whenever someone searched for booking a ticket. I am not aware of the exact term for it, but I believe it is known as search engine optimization. They mentioned this in their latest Concall. Hence, now their brand is all getting propogated.

Now, their string of pearls method of acquisitions in non air segment, will help them not only to enter new segments but this attacks their competitors who get more revenues from non air segment.

Lastly, all other players are bases on outside funding, what do you think when this funding starts slowing down, which eventually happens. Then, these companies tend to go bust as they don’t have a sustainable business model. This is exactly what happened in the 2000 tech bubble burst.

I just checked. EMT still charges 300 per pax for cancellation.

Also @Chaitanya_Motani - thanks for your post. I did raise these questions earlier in the thread i.e. how easy it is for other cos (MMT etc) to simply turn themselves into a low cost model. There’s no clear verdict here but it surely cannot be as easy as turning off a switch. Companies do have an embedded culture they run on.

Lastly, EMT does few things differently which probably helps them i.e. different tech stack (dot net), which as per management limits their wage cost and in house support staff - better control / quality?

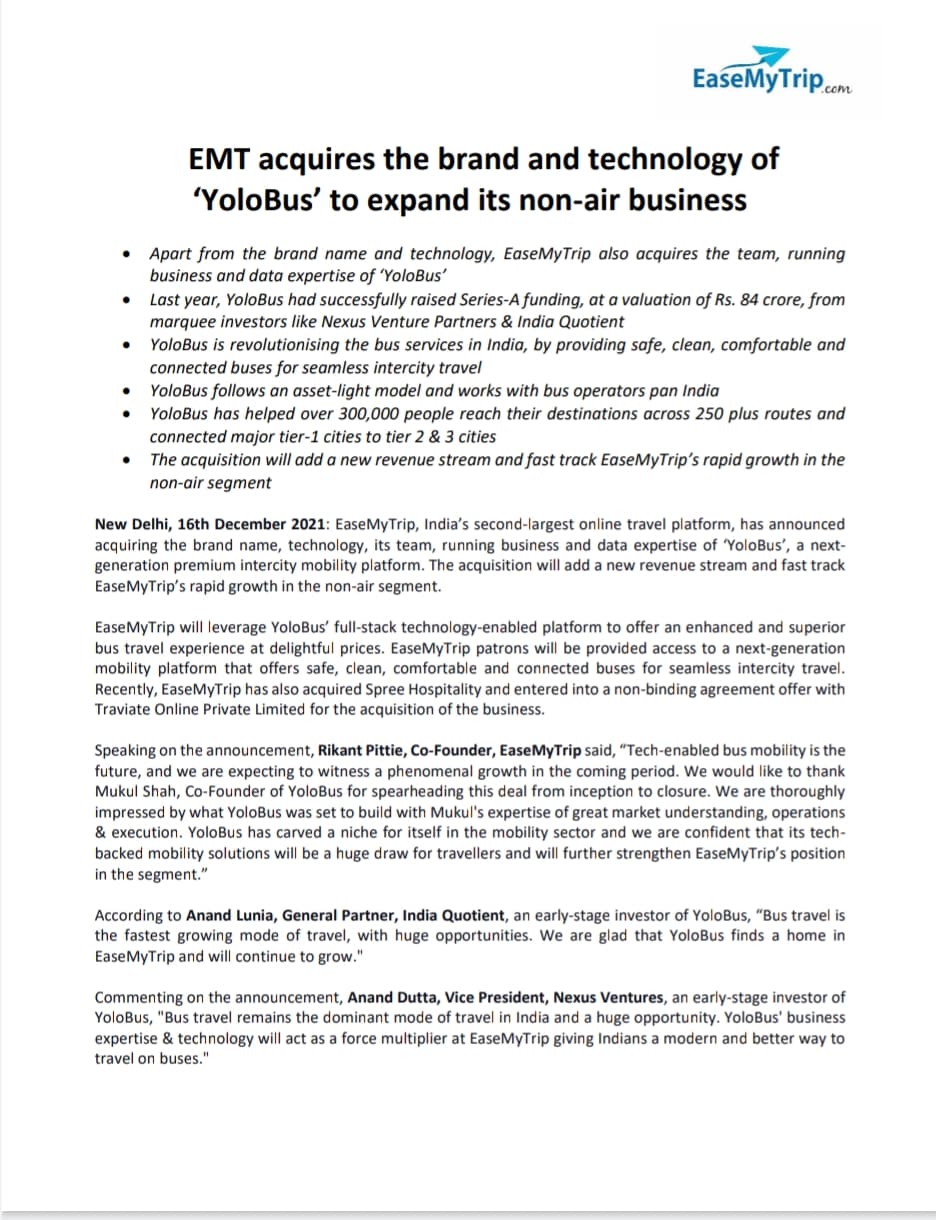

Another acquisition by EaseMyTrip. We need to appreciate the fact that the management has walked the talk. In their interviews and Concall in Q2 they had said that would acquire number of small companies in the non air segment and they have been doing that. This is the 3rd company that they have acquired in the last few months. This will not only increase competition on its competitors, whose major source of revenue comes from non-air segment but also decrease the company’s dependency on Air segment.

Whether these succeed or not, only time will tell, but I do have some confidence on the management’s commentary and promises. Will look to increase my allocation from 2% to 3%.

Maybe some engineer can comment on the tech stack difference of YoloBus and EMT and if at all, EMT can gain? Also would tech stack in itself prove to be an integration issue or does EMT plan to run the apps separately? What happens to the bus offering on EMT app then

Lots of questions. Also the revenue / booking data etc for YoloBus isn’t given, so I would be interested in that. Also on whether the senior management of YoloBus plans to stay on and function within EMT brand or I mean how does that work?

Why does this company not have a CTO when its peers have well distinguished CTOs.

Makemytrip : Sanjay Mohan, MS comp science from Uni of lousiana

Yatra : Manish Amin, head of IT ebookers, european OTA

Cleartrip :Manoj Sharma, NIT Kurukshetra

I don’t know if there is an official designation or not. But Prashant Pitti in his interview with Omkara Capital had said that- Rikant Pitti was in-charge of the tech. He had developed the initial tech.

This is very subjective. Appointment of CTO. It was mentioned in the Q2 concall in November though. Go through the transcript. Also Manoj looks very seasoned going by just his linkedin profile.

Board approves bonus at 1:1 ratio and spending approx 22 cr for this from reserves, per 31st march company has close to180+ cr reserves and completed 3 acquisition within this window …

India’s second-largest online travel platform has announced an exclusive partnership with Flybig, India’s newest regional airline. Under this partnership, EaseMyTrip will sell Flybig’s airline tickets. The partnership marks the first time that a Scheduled Commuter Airline (SCA) is exclusively partnering with an online travel platform, for flight bookings, making EaseMyTrip India’s first-ever online travel company become a general sales agent (GSA) for a domestic airline.

“Air travel is witnessing a major boom across Tier 2 and 3 cities, and we are delighted to partner with Flybig during such a critical juncture for the industry. Our unique range of services across the travel segment along with Flybig’s air connectivity across remote destinations will add immense value for both brands. Through this partnership, we aim to bring more destinations within the reach of our growing customer base, and we will be providing a hassle-free booking experience and the best-in-class services, for Flybig customers. We are excited about the opportunities that this opens up and we look forward to scaling greater heights in the segment with this partnership,” said Nishant Pitti, CEO & Co-Founder, EaseMyTrip.

FlyBig is a regional airline based in Indore, Madhya Pradesh, India.[3] It is promoted by Gurugram-based Big Charter Private Limited. The airline began operations in December 2020 and is focused on connecting tier-2 cities within India

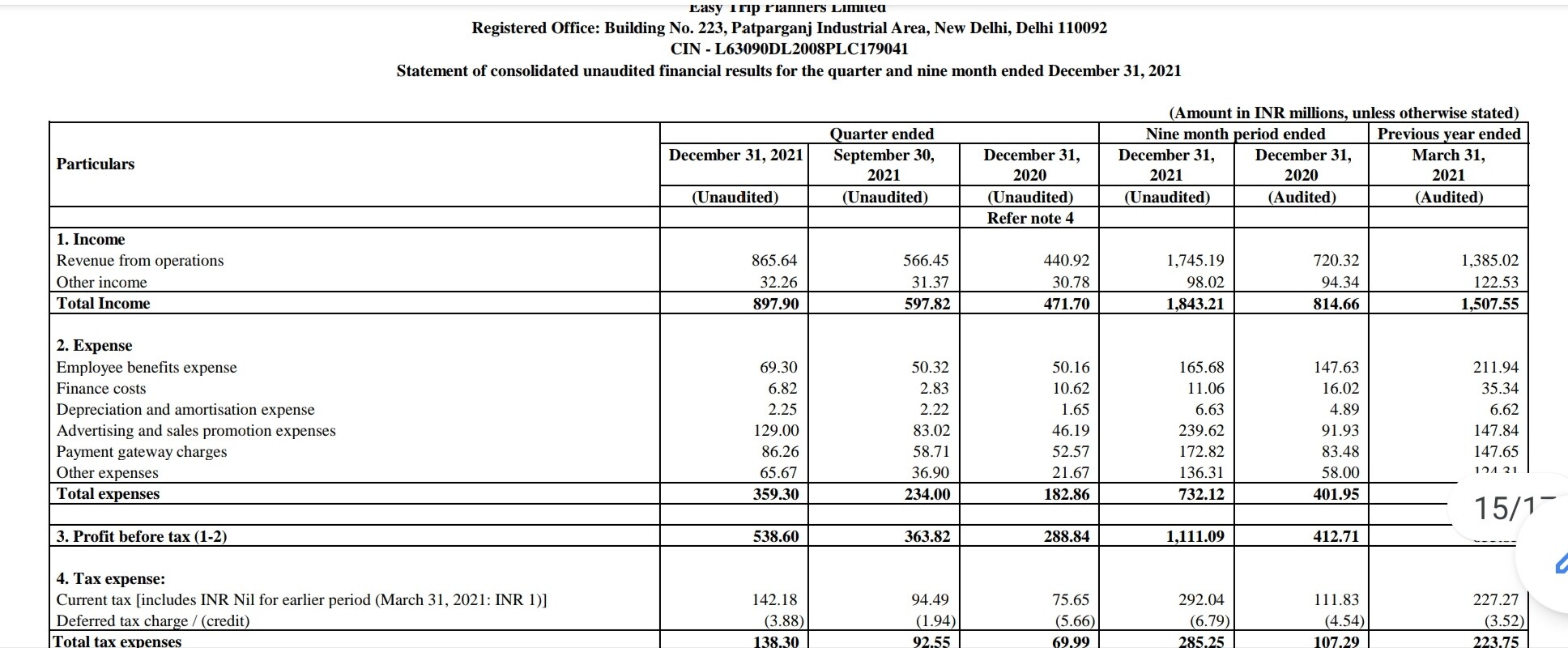

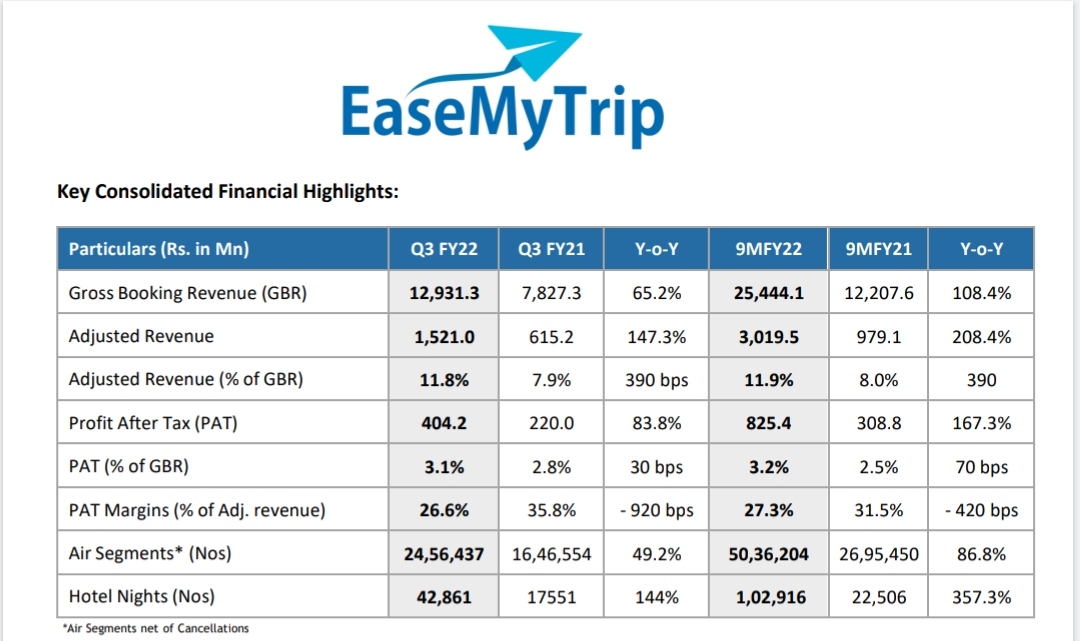

I was quite right in my estimates. Though I exited keeping in mind omicron led restrictions but given the solid performance - we can consider Q3 as the normal quarter. So annualising Q3 gives us 160cr profits on a GBR of around 5k cr. That means the stock is roughly at 36x normalised PAT.

What could be the GBR growth from here on? Industry growing at 10% CAGR and EMT is likely to see market share gains courtesy strong cash position and international expansion.

D - Exited in Jan. May relook to reinvest tomorrow if it doesn’t hit circuit.

PS - Hotel segment reduced losses in this quarter. +ve.

I still don’t think you can call this a normalized quarter. Air travel is still under 90% of pre-covid levels. International travel which has higher yields is way below the pre covid levels. I think they can do much better in a normalized situation. Their costs as % of revenue should keep on going down as after a particular inflection point, the costs will remain stable but the sales will keep rising.

I still think there is much more scope for this company.

I agree with you, Q3 was an amazing quarter for the company despite some challanges. With prashant getting more hold over the company it should do well. Cheers!

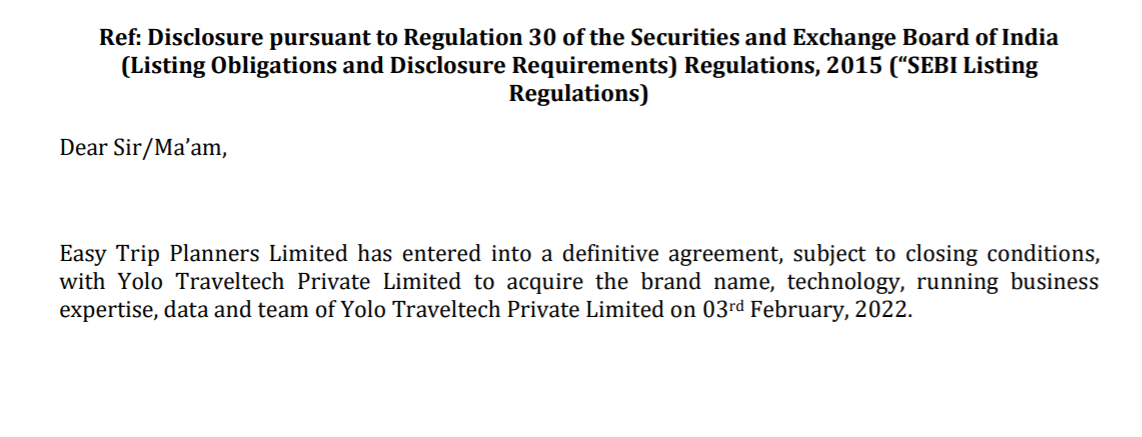

Definite agreement done! as per co, only the spree revenues, employee wages are added to balance sheet part of Q3 quarter, as the definite agreement deal is completed for YOLO tech today and this further adjust the balance sheet in the forthcoming quarters. Co, in talks to pick more acquisitions considering the asset light model business as the mandatory clause.

Some red flags :1. Loan on books despite cash on books & parked on lower earning FD 's . 2. Floating working capital as advance which has made operating working cashflow negative .3, Serial acquisitions .

4.low employee salary on the IT side . Average salary of 11 lakh in IT in current scenario doesn’t add up .

Need to do more detailed forensic audit before getting into this .