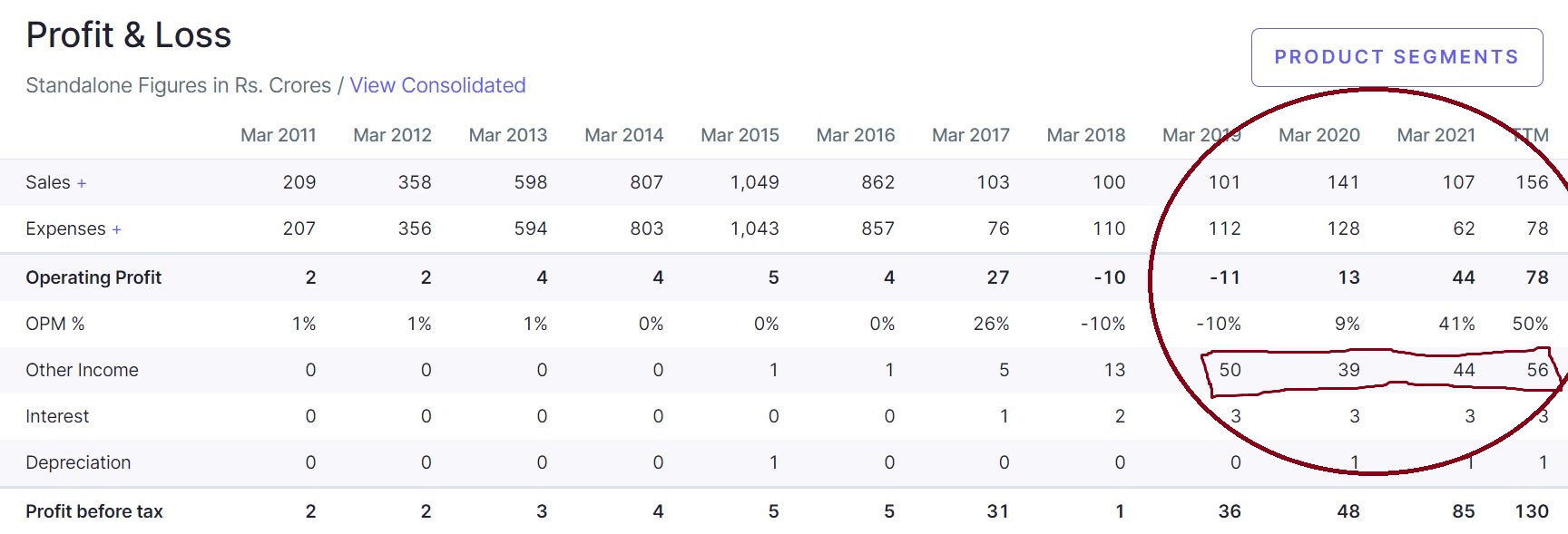

Let’s crack some stories about EaseMyTrip. Tons of people are doing comparisons with MakeMyTrip or others. Leave that behind… let’s focus on their own balance sheet and Profit and loss statement and let’s see what’s not changed in the last 2-3 years.

Notice something? look at other income for last 3 years. look at the other income which is EQUIVALENT of 30-35% of Gross sales, and contributes almost 50% of Profit Before TAX:)

did you find anything in any of the ANNUAL general report or quarterly statement what is the source of this other income which is half of the profit:) TCH TCH…

I tried finding it in 2021 Annual report but in the whole report, no mention:) Not even a single word how did 44 Crore of other income was earned:)

Yup:) writing more:) in due time:) while they have fixed these issues but there are so many glaring things… unsure what is retail customer looking into this with these obscene valuations:)

After listing the stock did well and Few brokerage came with their coverage…

As It’s a profitable business and management is initiating lot of things i thought of buying a tracking position in it after recent correction last week…

Buy order was not getting processed for last 5 days , Message shown was RSM Blocked…

When contacted my broker( SBI securities) they said SEBI has put this script on surveillance . N they stopped trading

Anyone else had these issues with their brokers?

Thought of sharing my experience, if not help feel free to Flag

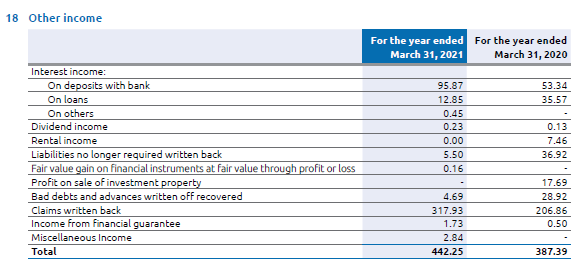

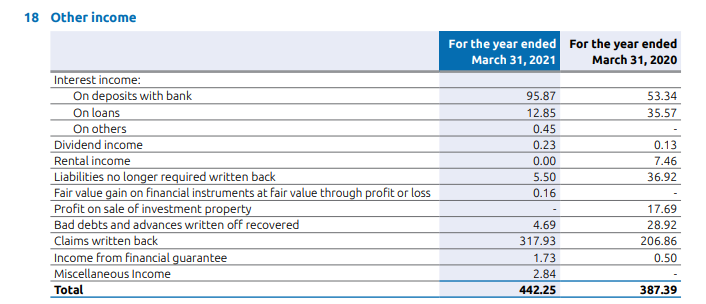

Here is the break-up of other income from Annual report.

Majority of this pertain to “Claims written back”, which is defined in the annual report as " The Company recognise an expected breakage amount as income in proportion to the pattern of rights exercised by the end-customer. Breakage amounts represents the amount of unexercised rights which are non refundable in nature as per Company policies."

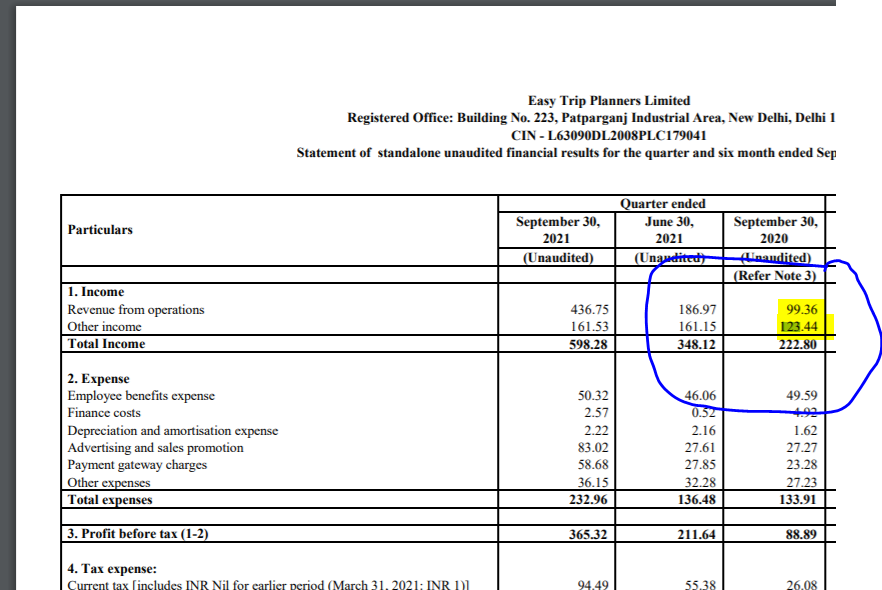

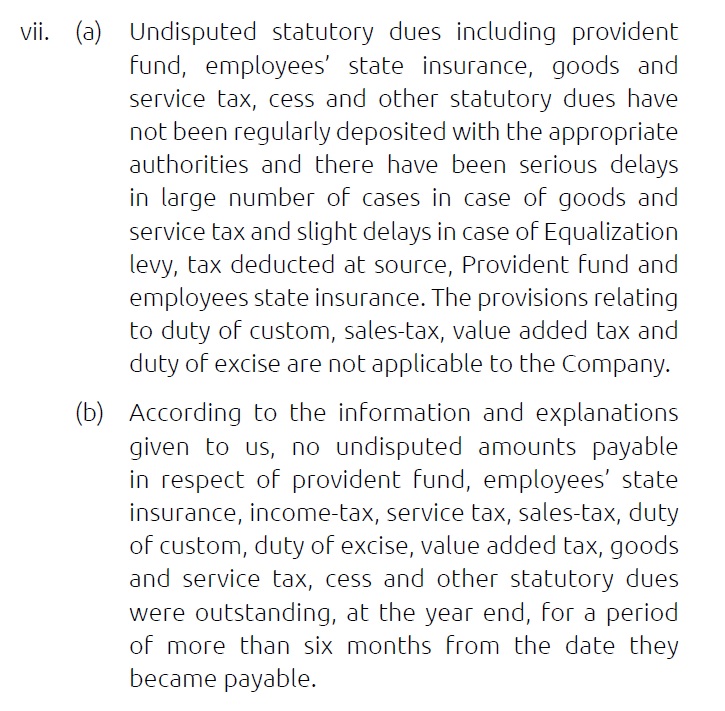

For me analysis ended at finding consistent track record of delayed statutory payments.

The biggest component in “Other Income” is claims written back, which is essentially the refund received from the airline to be transferred to customers (which doesn’t happen in some cases). Essentially, 30cr (out of total 40cr is the GBR that was supposed to be transferred to customers). That’s less than 1% of the GBR they’d have 2 years ago i.e. in 2018. They have a policy where they keep these charges in the balance sheet for 2 years before charging it to P&L.

The other major chunk is just interest income and they had 117crs of cash on March 31, 2020, which ballooned to 185cr as on March 31, 2021. Even if I do an average this comes to around 150cr of avg yearly balance and interest of 9cr gives around 6% yield. Doesn’t sound too improbable given 2020 also had slightly higher rates.

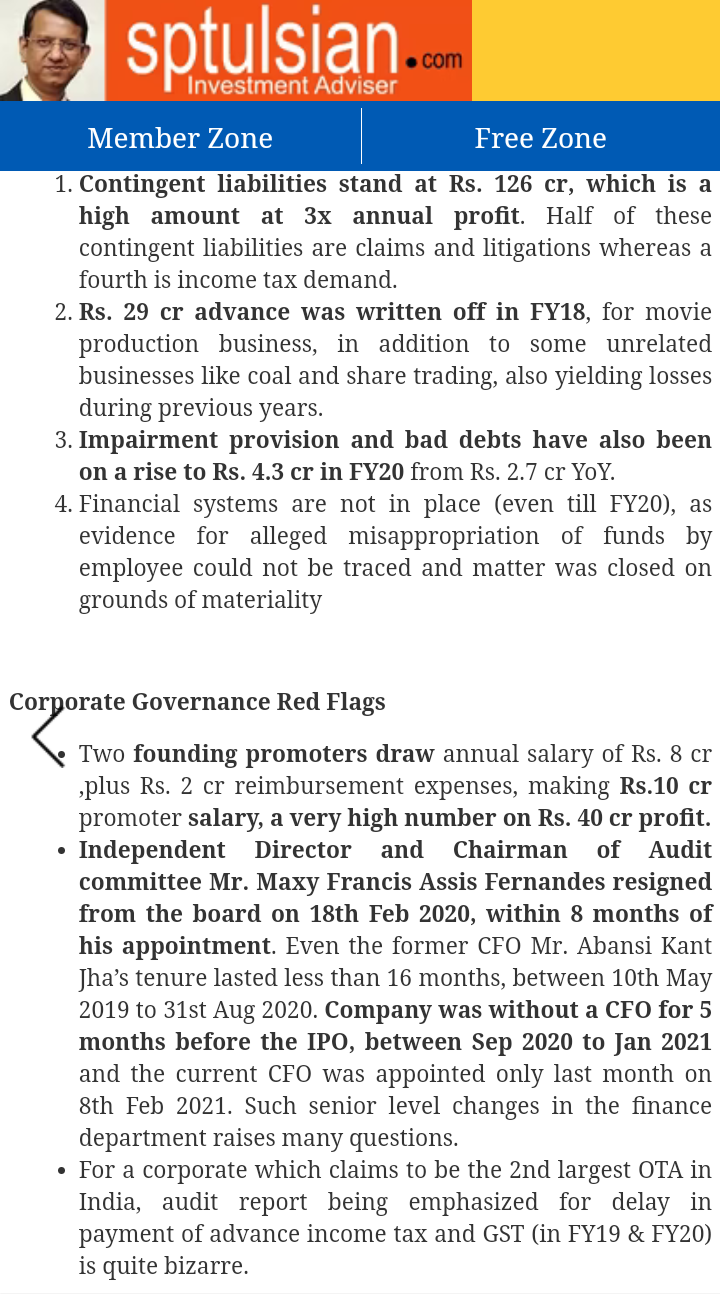

On the salary front, I agree. I did not like the fact that promoters are not taking a haircut but employees are. But that has been fixed in 2021-22 where promoters have taken a haircut (dip in employee benefit expenses is visible and this has also been clarified on con call).

Always believe that valuations are a function of how you see the business behaving in future. I estimate EMT’s normalised GBRs at 4k cr and with 4% of GBR as PBT, we get to around 160crs of PBT and around 120 crs of PAT ~ an EPS of roughly 20.

For a cash generating business that’s growing at 20%+ CAGR, existing stock price is under 30PE (on a normalised EPS basis), I don’t think the valuations are “obscene”. Need to watch out for their dividend policy too.

Some issues (delay in deposit of statutory dues, independent director etc) are of concern though.

If you see the conference call transcript of Q1FY22 Mr. Prashant has answered this question. They keep the amount for 2 years. If the customer does not come and ask the money then it gets recognized as Claims Written Back and gets mentioned in Other Income. For 2 years it remains as liability in the books. He also mentions that competitors give only 3 months to claim that money to the customers.

Yes. So statutory dues were deposited with delay but were deposited nonetheless. I still don’t understand why there were delays in depositing GST / TDS. Equalisation levy I can understand as a big4 guy since there’s a lot of ambiguity on this.

Air traffic at 8.8mn. Even at avg 8mn for 3rd quarter, it means 24mn pax in 3Q (Dec is travel heavy). OTA’s share ~ 60%. That gives us 14.4mn. EMT’s market share as per ixigo’s DRHP = 19%. Let’s take 15% and we’re looking at 2.16mn pax arrivals (or tickets) courtesy EMT

So approximately 20%+ rise in QoQ compared to Q2 (1.8mn)

GBR in Q2 = 895crs. Take your guess for GBR in Q3.

I had estimated a 8mn/month pax flow on avg for Q3. October figures are out and are at 8.8mn. Q3 is also the best time for air traffic. My guess is Q3 will have 8.5 to 9m/month traffic which translates to 25.5 to 27mn for Q3.

EMT might see a good jump in GBRs. ICICI Direct in its latest report had estimated 3300crs of GBR for EMT in FY22. My sense is EMT will end up doing around 3500crs of GBR for FY22.