This details about Hybrid cloud security gives more insights of what E2E networks is

2 Likes

I think we can simplify the business model into three categories.

A . Compute resource [ CPU, Memory, Storage] provision over the cloud has lot of competition, however many MNC like HP, HPE, Dell will eventually join the game so, I would say this is a low margin proposition.

B. Compute resource, backup and services related to IP address, domain address registration etc can be a package to customer, this is an interesting space to be in because switching cost is higher if they have customers. But we don’t have data on number of such customers.

C. GPU as a Service.

This space is a very niche area and requires a lot of computing resources, having one GPU per server is of less use so, companies buy a ton of GPUs so, that customer queries get answered very quickly. E.g. Computers use GPU to simulate Weather patterns, Predict the failure of the supply chain based on orders, anomaly detection in turbines, DNA analysis, Pharma etc

So, there are two variables in the GPU equation, Training an AI model using large Data set and building an output from the model, aka Inference which is intelligent enough to predict or do the required goal in the shortest time.

With more data, the training of AI model will be good but it requires lot of trail and error as AI world is very specific to the use case. There is no standard way of doing things in AI world because data is unique.

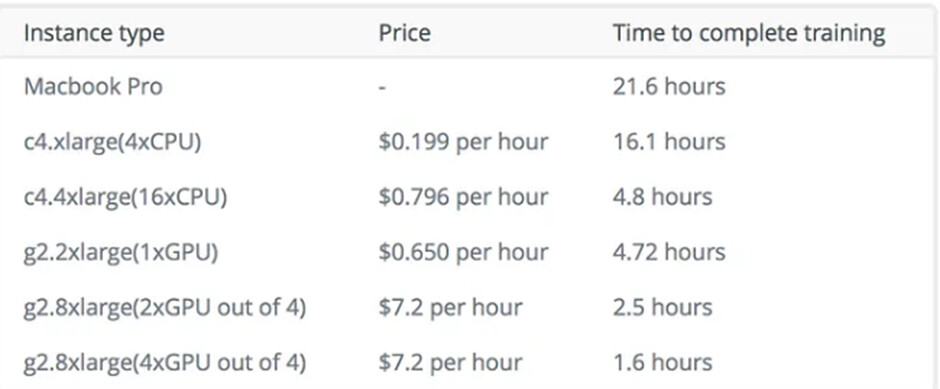

The below graph from link shows how much GPU is required for training. Now if we map it to the e2e client, what can a customer do with 1 GPU and a small machine? That too all the machines run with virtual CPU/KVM.

What can the customer achieve then?

- They can do a prototype of an AI/ML model and train the model with a limited amount of clean data.

- They can measure the model outcome but for better inference lot of data and bandwidth is required.

So, Once we have data on the below points, we can understand the exact usage of the infrastructure and the possibilities of scaling this to new frontiers.

- Client Categorization

- GPU usage with respect to clients

- Number of customers onboarded

- Retention of customers on their platform.

- Number of customers using 1 GPU vs 4 or X GPU

2 Likes

India’s Top Cloud GPU Providers for AI / ML .

Looks like a paid article. Towards the end, it mentions source as “PR Agency”!

E2E cannot compete with top 4 vendors on scale…they are massive and rightly are called hyper scalers…only area where E2E scores is based on their claim of a much lower pricing.

Just my opinion!

1 Like

Latest article on E2E networks

1 Like

Thanks vnkt

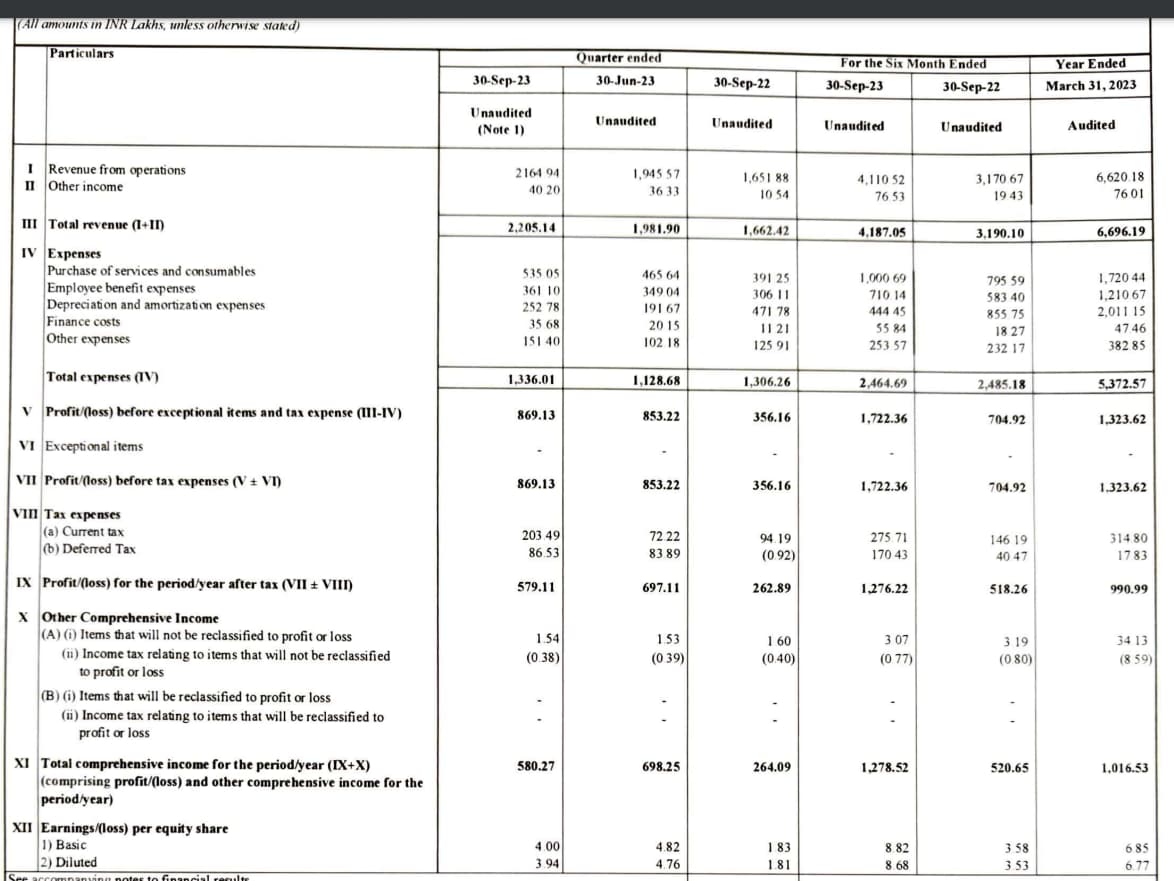

Quick thoughts - Given the change in depreciation policy, I am now evaluating the company on EV/EBITDA multiple for a fair like to like comparison over previous years.

- The liabilities seem to have suddenly increased in higher proportion to sales growth - 10+cr in lease liabilities in Sep’23 ( ~5 cr as of Mar’23 and 1 cr in Mar’22). Need to understand these

- QoQ rev growth is ~ 10% (good IMO), ~ 31% YoY (would have preferred more at this scale).

- Need to spend time and calculate GMs and GM trends in detail (hopefully they are stable).

Overall, the company is available (As of today CMP) at EV of ~ 750 cr (780 cr mcap, 17 cr debt and 41 cr cash). For a TTM Ebitda of 40 cr, the company is available at <20x which to me is a reasonable valuation. I will continue to track quarterly results and hold if the trends sustain. Profitable SaaS companies should command anywhere between 30-50x ebitda depending on multiple factors (market size, competition, moat, margins, cust retention etc).

Disc : Invested at below 200 rs, >5% portfolio size so views are very likely to be biased.

5 Likes

Anyone having link for management concall pls share

Have you compared it with net web technologies. Later management looks more transparent. Any competitive Advantage of E2E vs netweb

HI Grp,

Thanks for bringing the company to my notice, I was not aware of it before.

A quick look at the financials gives me the impression that its more of a trading business rather than a IaaS platform (which E2E is). The company does not look like having a large services business either as the margin profile (Gross margin of ~ 30%, Ebitda of sub-15%) reflects the business model to be more of Value added resller rather than providing any self developed IP. Also, the company seems to be trading at very high multiples (80+ times EV/Ebitda leaving very little margin of safety if something were to go wrong).

Such businesses are outside my area of competence hence I would not be in a position to provide any views/insights.

Hope this helps.

6 Likes

Thanks for the update but given that E2E is having upper circuit everyday doesn’t it looks like some thing fishy.

Also how one can buy in upper circuit…

Note : I bought it at 168 but not happy with upper circuit everyday sold at 400 something

This is the only Indian listed company in GPU cloud segment. Screenshots from company website is here oliw :

Please see the companies website where one can see the competitive edge what this company offer

4 Likes

I have mentioned it before as well…the only reason it hits upper circuit so easily is because of very low free float…just check the trade volumes for each day it has hit upper circuit in last 2-3 months…order volumes are in the range of 3k to 10k shares on average…

Just one suggestion - revisit your criteria of selling out due to this upper circuit thing…I made similar mistake during Covid and lost out on lot of gains in the euphoria…we need to find a way to ride the wave unless prices gets to ridiculously high zone…easier said then done as the risk of losing all the gains is always at the back of the mind…need to develop a good framework that can help get over anxiety and bring in some objective way of doing it…

6 Likes

Yes you are absolutely right.

Must listen to understand the prospects

2 Likes

Government plans for setting up AI computing infra, in public sector and also in partnership with private players.

Article available with premium subscription.

Disc: invested

6 Likes

Hi vikas

Could not get the full article as its paid one

Do you feel that the tie up with Govt companies will benefit E2E networks?

Thanks

1 Like

They are the only company offering compute which has greater than 50% Indian ownership. Why would the Govt not want them to scale up so that they become a good alternative to American cloud companies?

Think!

The only problem that E2E has right now is that not enough people know about them in the Indian developer ecosystem. Tie-ups like this help with that marketing problem even if it does not translate into immediate revenue increase.

3 Likes

To that point, I have seen them get quite active in the last 6 months. I have an account with them and get regular invites to webinars and articles. All communications aligned with AI. I had written it as a suggestion on this forum to get in touch with deva as eventually it is dev/architects who make platform suggestions to business teams. It seems either we are thinking alike or the company reads and values this discussion. Happy with either!

Wouldn’t be surprised if in some time we get an articles with “meet the indian aws” kind of titles.

Holding on for dear life!

8 Likes