Just had a thought based on yesterday’s fillings. For context, co. has passed board resolution (to be passed in September by shareholders) to raise equity and debt.

Equity : Equity will be raised from Rs. 16.5 cr (1.65 cr. shares of 10 Rs. each) to 25 cr. (2.5 cr. shares of 10 Rs. each). Therefore, 8.5 cr. shares @ CMP 363 = 8.5 X 363 = Rs. 3085 cr. could be raised.

Debt : Resolution passed to raise up to Rs. 1000 cr.

My thought is this:

The company is about raise money to expand infrastructure and team quite aggressively. It might also be thinking of doing more marketing to quickly capture larger market share. Two important notices in this context:

Changing the life of computer hardware from 3 years to 6 years: If large capex in infra was done in small time frame(within 1 FY), the hit because of the depreciation at the end of the first year would be have been quite large doing opposite of what happened this quarter with the sudden jump. So, 6 years instead of 3 will ease it out for the P&L. The bigger infra would obviously bring in larger income but utilization on the infra would be lagging behind the capex as marketing would slowly be ramped up.

Discussion with Param Capital (Mukul Agarwal): Possibility of equity being raised from him. The company is right up his lane.

Need more profit => Need more sales => Need more infra => Need more capital => Change depreciation to accommodate larger capex => Raise capital from equity/debt => Talking with investors including Mukul Agarwal.

Did the management disclose their GPU/CPU cloud utilization % anywhere?

On the website, it’s showing Claim your spot on the waitlist for NVIDIA H100 GPUs. Join waitlist? Does it mean that they don’t have enough infra with NVIDIA H100 for now. If not, I don’t think they can get H100 anytime soon considering the huge demand pipeline with Nvidia and pricing power($40K)

Yes the depreciation earlier was super aggressive. The new depreciation rate is the correct rate assets should be depreciated at. Hence the logic of looking at P/E. Alternative look at it P/CFO where CFO = Cash Flow from Operations. According to screener CFO was Rs36 crs last year. Stock is super cheap on that metric too…

Private cloud is more static in nature, which means that any changes to their cloud configuration would take days rather than minutes or seconds, but broadly, it’s very, very similar to the public cloud except that your scale ups and scale down happens in days and weeks rather than happening in a few seconds via an API call.

Company is not into contract modelling

There is not a massive difference between public and private except that the public is technically slightly ahead in terms of the time taken to do things on the public cloud is obviously shorter.

There is no relearning required to kind of migrate from one cloud platform to another

Migration : There are business constraints in terms of the proper project planning being required to migrate from the on-premises to a cloud or from one cloud to another

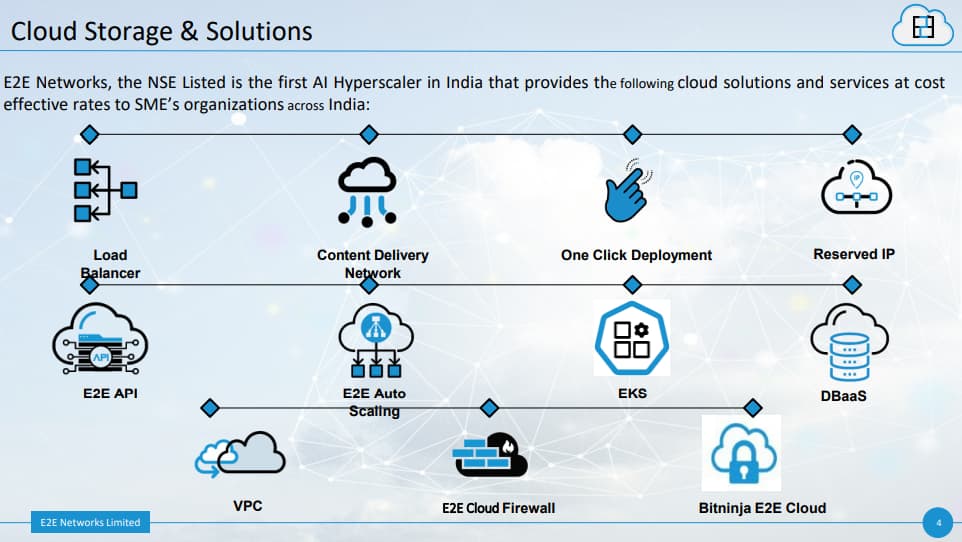

In the below article - most of ecommerce use E2E because of low cost and for managed services such as to tackle “upswings or downswings in traffic easily and cost-effectively". they use Google or AWS.

There is a cost associated to each, why it makes more sense to ecommerce because of hype scaling as when they need, load balancing & CDN.

So far E2E is the only company in India that I know of provides such decent good oriented services.

Now when it comes to the data these are relevant :

Data Theft

Data Leakage

Cloud Data Security

Cross-Border Data Transfer

Phishing and Social Engineering

Insider Threats

Data Encryption

Regular Backups

Incident Response Plan

Compliance and Regulations

Employee Training

Security Patching and Updates

Network Security

Mobile Device Security

Third-Party Risk Management

Data Retention Policies

Regular Audits and Penetration Testing

What’s more important is that : Government is very vigilant on CROSS BORDER DATA TRANSFER AND THIRD PART RISK - because the medium to store data out of the country is one big risk that country cannot afford.

Every government in countries has a regulatory framework to define the data movement

India has its own data center example E2E small listed, TATA COMMUNICATION.

Google, Microsoft is investing heavily in India for Data Center. This ticks one thing for sure that the Data Center will be good opportunity, players are establishing now but leaders will be decided in future

What is missing in your study is the information on free float available in the market. Just check that and you will know why price movements are so wild (upper circuits and lower circuits). Hope this helps.

E2E : I think this business has stickiness due to the fact that once a client is onboarded then changing back to any new private players becomes difficult reason being

Platform Cost - Private ones are expensive

Migration Cost - To move from E2E to Azure, Google, AWS - there is a cost associated to lift and shift - also they would need to pay engineers additional cost on doing so.

Uncertainties in business/data risk, if client proposes for shift.

Reskilling - In cloud the major issue is engineer cost - we can expect the structure of the cloud to be same however implementation/execution, platform skill are very different.

Time Factor

Other notices :

Company is planning for capex to scale

They don’t have long term contracts their clients pay them month on month basis

I am invested in this scrip. But I have a few observations/queries. Any thoughts on them would be helpful !

a) In recent times from the week of 17th July 2023 onwards the stock has witnessed an almost non stop vertical rise. Few days in between it did see corrections. But again turned around and started the vertical rise.

Interesting thing is prior to the week of 17th July 2023 and for quite an elongated period the price movement was almost flat.

Wonder what could have prompted this vertical rise when there were no triggers, atleast in public domain. Q1FY 24 results too werent declared ( atleast publicly) and were several days away.

b) The change in depreciation policy which coincided with the Q1FY24 results which all of a sudded made the PE look very attractive. Not sure again what was the trigger or the need to do it then. Could it not have been done earlier ? Or later ?

c) In the last couple of months or so, two of their Company Secretary & Compliance Officer left the company. Company Secretary is a senior resource and a KMP. Is this an usual development in micro sized companies like these ?

a) If a stock is undervalued, its price may rise before results. At that time, the PE was around 25. Particuarly in microcaps, it is a sad state of affairs that insiders almost always have more information about the actual value of the company.

Also, one of the long-term PE investors exited at this time and new investors took their place. The next quarter shareholding pattern will reveal more on this.

Correction was when the stock went into the ESM, similar to several other microcaps. Several microcaps have similarly recovered by now.

b) No idea. My guess is that older hardware was fully retired by this time.

c) Yes, this is a valid concern.

The corporate governance of the company does not seem to be the best. Earlier, they seem to have revealed to Valorem Advisors a lot of information that was not in the public domain. Hope they get their acts together soon.

Thanks for sharing your detailed views. I agree with you. Not all bits of investor related information are available out there formally and accessible to investors at large. Thats a challenge if one were to consider taking a long term view on this company,

Since public cloud what E2E has no complications in terms of scaling, there is little hiccup in the private cloud i.e. any changes to their cloud configuration would take days rather than minutes or seconds, but broadly, it’s very, very similar to the public cloud except that your scale ups and scale down happens in days and weeks rather than happening in a few seconds via an API call.

Secondly to move from one cloud to another i.e. lift and shift from AWS to E2E - this has a friction on engineer : which might takes again days, week to happen.

So private cloud is having no ease of use for now, they will improve this however one should note that large corporations use private server which in itself is secular and certain in nature for revenue.

There is also a cost factor when it comes to lift and shift

Even at current market cap of Rs702 crs the stock looks not too expensive trading at 25.0x conservatively extrapolated profits of Rs28crs on FY24. Surely there will be QoQ growth in profits…