Imo being listed/unlisted has very little importance. Point is who’s taking the market share and in this case it’s Yotta.

Hopefully E2e can gain some after Chennai center becoming operational completely.

Though, Yotta has big orders but there are only 2 orders with Yotta. I think, Yotta already had partnership with Sarvam. If you see number of orders, then E2E networks is clearly winning here. Though, orders are small.

3 Likes

It’s not a question of market share. While it’s true that E2E was the L1 bidder and naturally had a priority edge, one must understand that Sarvam’s requirement was for a large number of GPU clusters at a single location something E2E did not have at that point. Their GPU infrastructure was more distributed, and the clusters Sarvam needed weren’t available in one place.

Moreover, the recent capex on 2,000 GPUs was undertaken after E2E applied under the IndiaAI initiative, meaning those GPUs weren’t registered on the IndiaAI portal during the bidding process.

The management has consistently maintained that demand is not the issue, the constraint has been supply. If a large client comes in requiring 1,000–1,500 GPUs at one location, E2E was previously unable to fulfill that. The fresh capex was clearly in response to such demand signals, they had customer interest but lacked the inventory to deliver.

Now, it’s a matter of seeing how the ongoing PoCs convert into actual orders.

Disclaimer: Invested and heavily biased.

4 Likes

IMO, it will be all about tech -stack and softwares it will be providing.Bare metal compute with GPU’s may not mean much.

The two companies they are talking about can be VMware and Nutanix.

2 Likes

But Macro point of view all these companies VMware ,nutanix ,Rackspace are in bad shape . Everybody is intrested in hyperscalers .

1 Like

Nutanix is growing its market in private cloud and its revenues are growing.

For VMware, after the acquisition of Broadcom, Broadcom has increased the products prices and only focussing on few enterprise customers to generate the revenue. Because of this most of the customers are trying to look for alternatives.

This presents a good opportunity in Hypervisors in private cloud space including E2E and Netweb.

5 Likes

While that will lead to a revenue pickup, i feel they underpriced it significantly. And this is supposed to be the H200 that they just purchased. Well it is the India AI mission and returns are supposed to be lower, the MRR of 32-38 cr does not look feasible when you are giving 1/4th of company capacity at such heavily discounted rates. More like 27-30 cr. I am aware normal orders will have better margins though

5 Likes

While it is underpriced, margin should be better as no spending on sales!!

2 Likes

Yeah thats true but the predicted run rate does not make sense anymore. Queston that comes up is are they struggling to get customers? The AI story means it should be a no brainer for conversions which isnt the case? Salea should not be an issue

3 Likes

E2E Acquired a Coimbatore based company involved in providing in GPU infrastructure and AI Deep learning workloads

5 Likes

The company is not acquiring the entire entity; rather, it intends to acquire the specific assets of the company. The extent of assets that will be acquired from Jarvis is currently unknown. However, a preliminary search indicates that Jarvis possesses 100 GPUs. Further research is necessary to obtain a comprehensive understanding of the situation.

4 Likes

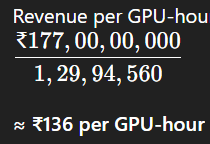

E2E gets 177cr order for total GPU hours allocated: 1,29,94,560 hours.

I have tried to convert it in number of GPUs -

If we assume 1 GPU running 24x7 for 360 days:

- 1 GPU → 360 × 24 = 8,640 hours in a year.

- Total GPUs equivalent:

1,29,94,560/8,640 ≈ 1,503 { GPUs}

So, this order represents ~1,500 GPUs running full-time for 1 year.

1500 GPUs for 177 cr is not bad deal.

8 Likes

How do we estimate whether it’s a good or okay deal? Want to understand

Yup this is much better than the previous deal assuming the calcularions hold.

As highlighted above, 1503 GPUs needed for this deal.

Cost per GPU-hour:

This is very competitive, since cloud providers (AWS, Azure, GCP) price H100 SXM at 250-350 rupees per hour.

Rough cost structure for E2E:

For profit analysis, we need to estimate costs:

(a) GPU hardware cost:

- H100 SXM (80GB) cost: ~$25,000–35,000 per unit

- H200 SXM will be $40,000+ per unit

- Let’s assume an average: $30,000 (₹25 lakh) per GPU

For 1,500 GPUs:

≈ ₹375 crores capex (if all were newly purchased).

But they may already own a fleet, or lease, or get volume/NVIDIA partner pricing.

(b) Electricity & datacenter:

- Power consumption: ~700W per GPU + overhead (cooling, networking, host) → ~1.2kW effective per GPU.

- 1,500 GPUs → ~1.8 MW sustained.

- Annual power cost (₹7/unit) = ~₹11 crores.

(c) Infra + Opex (network, staff, racks, depreciation):

Could be another 10–15% of capex annually, say ₹35–50 crores.

. Profitability Outlook

- Revenue: ₹177 crores (for 1 year).

- Direct Opex: ~₹50–60 crores (power + ops).

- Capex Depreciation: If new purchase, ₹375 crores amortized over 3 years ≈ ₹125 crores/year.

- Total yearly cost (depreciation + opex): ~₹175–185 crores.

This means profitability is thin or even breakeven if they bought GPUs fresh.

But E2E already owns the GPUs (700 H100 existing and 2048 H200 recently aquired), which means incremental cost is mainly power + ops (~₹50–60 crores), and this deal would yield ₹100+ crores gross profit.

. Strategic Angle

- The per-hour pricing is ~50% cheaper than AWS/GCP → very competitive for India-based or cost-conscious AI customers.

- This deal also signals capacity utilization: This contract ensures strong utilization & cashflow.

Summary:

- ~1,500 H100/H200 GPUs are needed.

- Deal value = ₹136/hour (~$1.6/hr) → half the cost of hyperscalers.

- If GPUs were a new purchase → breakeven at best.

- But GPUs already owned → ₹100+ crore profit after power & opex.

- Strategically, it looks like a utilization + market positioning play rather than a one-off profit-maximizing contract.

23 Likes

There’s news that OpenAI is in talks with a few companies, including E2E Networks. I’m curious about what kind of services E2E Networks could potentially offer to OpenAI. Can anyone shed some light on this?

1 Like

There may be a possibility of Sovereign Cloud offerings as solutions like ChatGPT and Perplexity are keen to work in Indian market and as per Govt guidelines the Cloud has to be in India. This is just my assumption.

1 Like

3 Likes

That;s good news. Its reassuring that E2E has the backing of LnT, so they will leave their mark. I want to know how differentiating their Software solutions is

2 Likes