Tarun at CFA society.

Tarun at CFA society.

AWS/Azure and E2E are different businesses. AWS/Azure focus is not on renting GPUs - they are mainly a infrastructure as a service for tech companies to have their entire stack on it. E2E is now primarily a “hyperscaler” and comparable is Coreweave.

Coreweave’s H200 pricing is $50/hr[1]. On a monthly basis, thats $36,000. With an annual commitment, you would get 50% discount or more. So approx $18,000 or Rs 15.3L at exchange rate of Rs 85/$.

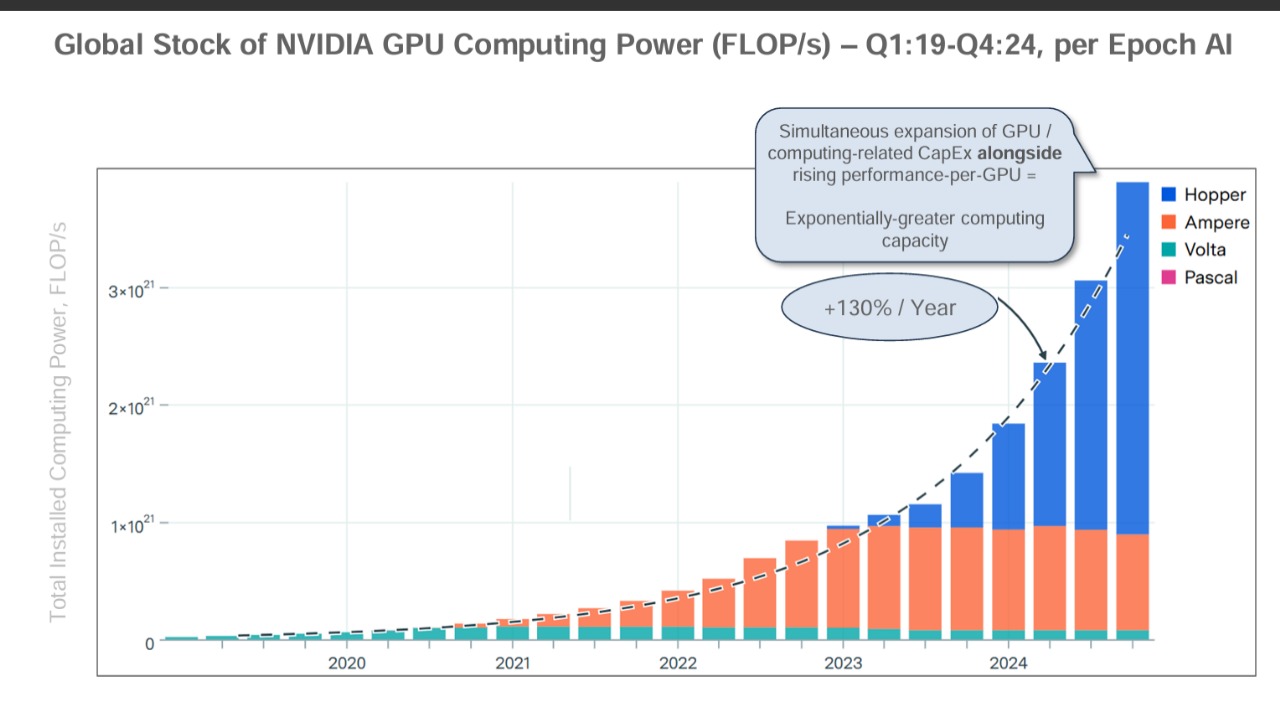

If anyone is looking for a indepth study of what is going on in the space of AI from a global perspective. Be it Chip design companies, chip manufacturing companies, companies who are making models, companies who are providing infrastructure, companies who are using these infrastructure to provide cloud services and companies who are using these cloud services to cater to end consumers.

This research report is recently published by bond capital in May’2025 and is a very interesting read.

This is a publicly available document. Here is the link-

FY26-Q1 results and concall scheduled on 22Jul.

https://nsearchives.nseindia.com/corporate/E2E_16072025125233_EarningcallIntimation22072025.pdf

I won’t expect anything bottom line wise. With the massive capex they are doing, PAT should be very low (even negative) … but I want topline to pick up with decent EBITDA margins

The business seems to be a heavy asset business. I think the EV/EBITDA multiple will be a suitable valuation parameter for this kind of business. Based on the revenue and EBITDA projection for the next 2 financial years. It is trading at around 10 EV/EBITDA multiple.

However, as per the books for FY25, the company has around 1350 cr. of cash which will be invested and EV value will increase.

As expected, negative results. While topline growth and EBITDA have also not performed well atlast their monthly run rate is up. I see 14 crores which would indicate a topline of 14*3 but since it is 36 crores, it means MRR as of now is trending upwards as they said woukd happen.

Waiting for management clarification but seems like their testing for big enterprises is still ongoing.

E2E is in an exciting space and when compared to CoreWeavs and the likes, its not that expensive. Definitely will be buying more if it comes back down to 1800-2000 levels.

How are you analyzing the results? In the call the CEO said that:

they expect ‘some’ business from selling software to L&T. Seems underwhelming

software revenues will be significant from next financial year.

What is your read on the bear thesis that the return on capital employed for GPUs is not attractive due to short life.

Thanks. Asking since you had shared some very helpful datapoints previously

Went through ppt and earnings call

This result was quite bad

Points that were not clear -

Futuristic statements

Everything was Not good as per my humble opinion

With no revenue growth how are they expecting higher utilization rate of GPUs. With Chennai capacity added, I am afraid utilization will further go down unless they really expect to sign deals with several POC clients in Q2.

In Q4FY25, they were doing POCs for large customers, which occupied a large percentage of GPUs. This resulted in lower MRR. From my understanding of yesterday’s concall, they seem to have got good customer traction from these POCs.

The share price after one year will depend a lot not only on the revenue but also on the expansion plans at that time.

My award for the best concall commentary, among those I have listened to in the recent months, goes to Inventurus Knowledge Solutions (no buy/sell recommendation). E2E concall can be much better in comparison. Things can be explained in a structured and concise manner, ensuring continuity from the previous concall.

Disclosure: Invested.

great summary; i’d like to add a few points from the concall: