Though we must note that the infra industry that Sanghvi movers is in is not expected to jump the way AI as a space can deliver in the years to come. If you believe that AI will take over the world, then E2E networks is in an interesting space. The 40 crore numbers also ignores Sovereign AI and the LnT expansion.

5 Likes

I am not sure whether GPU obsolescence is a big deal. At least it isn’t anything particularly new to cloud services - almost all computer hardware has a shelf life of around 3-5 years (if you check the depreciation schedules in the financials for major cloud service providers, average will be be between this range).

Think about your laptops, phones - a 4 year phone or laptop feels antiqued. Most of us churn our personal gadgets within 3-5 years - hardware is no different, GPU or not. In fact, a lot of this stuff happens without the customer even being aware of it in case of IaaS/PaaS.

To me, the major risks are

- Demand is transient, not sticky - Essentially, you have 2-3 years of very intense training demand and then all models kinda reach their max capability and so training demand ramps down significantly. So you’d have E2E’s revenues spike for 2-3 years and then drop back down to baseline.

- Competition - It is, at the end of the day, an extremely competitive space with no moats and everything comes down to who can execute the best. So even if demand is sticky, they need to get sticky customers who continue to use E2E over years rather than switching to another cloud service provider. For example, OpenAI just recently choose Oracle over MSFT data centers for a large part of their upcoming training and inference.

Disc: Not invested

10 Likes

Demand is transient and competition is high, along with that life of GPU is only 3 to 4 yrs.. that makes it even worse since one does not have enough time to recover in case business goes through rough patch for a year or so.. not enough room for safety at such high PE.

3 Likes

Hi Hitesh,

Any insights on why the promoter pledge is so high at almost 55%? Haven’t heard this discussed on any of the recent calls. Since you plan to meet with him on the sidelines of the Sovereign Tech conference, could you please check with him on this point?

Thanks in advance

2 Likes

It’s not a pledge. It’s encumbrance which restricts E2E to further transfer the stake without obtaining permission from LnT.

4 Likes

Aware of a friend who has secured a seat. Will post an update here soon. If anyone has specific questions, feel free to let me know and I will convey them ahead.

1 Like

e2e networks shared their analyst and investor presentation yesterday. it covers ai cloud platform growth, gpu capacity expansion, and updates on their strategic partnership with l&t.

if you enjoy reading in a visual format, this is for you.

e2e.pdf (4.5 MB)

3 Likes

Some questions on cloud platform

- Can we get a difference between E2E SCP vs VMWARE. Because any multi national company would prefer big company because of mission critical Data stored in their cloud.

- Can SAP or any other enterprise software be easily integrated with cloud platform ? Because Migration is still a large market globally

- Any corporation/enterprise/startup using their platform ? And how is the feedback?

4 Likes

L&T must be using AWS or other cloud provider for its IT operations. Is L&T considering switching to E2E in future?

2 Likes

If E2E has to create wealth, the software business has to scale up.

Currently there are hardly any software revenues. But the software creation is being expensed in the employee salaries.

If the software platforms pick up - and there are multiple different such platforms - each with multi Million Dollar runways - this can be a winner.

There can be a tailwind from Aatmanirbharta also - one never knows when the cloud sector may start increasing indigenous content like the defence sector.

Plus government contracts can be pretty sticky if E2E plays it’s cards well.

This being the longer term vision - in the shorter term we can see the strong guide by a pretty conservative management as tilting the scales in an investors favour.

Dis - Have a small position.

6 Likes

5 Likes

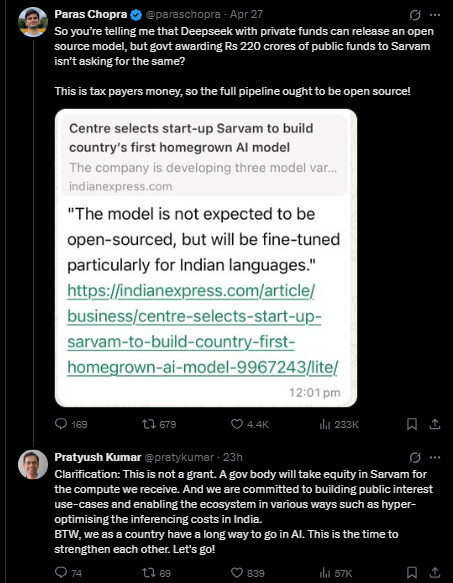

Sarvam AI is first company’ to get Government fund 230 CR to develop India’s first AI LLM, few more to be selected soon. Also govt is planning to double it’s gpu offering under india AI mission. Total would be around 29000 GPUs..

5 Likes

I read somewhere that the Sarvam AI code will not be open-source. If that is the case, does it not mean using public funds to build private intellectual property? It will be interesting to see how it develops because people will likely raise objections to using public money to build private IP.

2 Likes

I checked api.sarvam.ai to see what they are using for inference right now and it looks like they are using Azure (request ends up at a data center server registered to Microsoft). The location of these servers appear to be in the US.

I checked their website and they already appear to have a suite of existing LLMs for Speech to Text, Text to Speech and Translation for Indian languages. It is unclear what this new “sovereign LLM” will be. (The quote from Pratyush hints that it will be used for adding voice mode)

Some numbers - Provisioning of 4096 H100 GPUs over 6 months (source - ISN article linked above) works out to be 313cr at E2E’s H100 pricing of 1400 Rs/hr (which can assume other providers would have similar rates). I am guessing it will be discounted to 230cr for a 6 months contract.

The ET articles linked above mentions that Yotta will provide 9216 GPUs, E2E 1,353 GPUs and NxtGen, 1,088 GPUs. So only Yotta has the capacity to completely fulfil Sarvam’s training workload (though Sarvam could choose to split it but that seems unlikely to me).

Disc: Not invested, tracking

3 Likes

L&T has its own Data Center business called Cloudfiniti. They probably use that and will stick to that. They see E2E as a specialised player in the AI cloud space (where Cloudfiniti is not present right now). For AI-related use cases, they could switch to E2E.

3 Likes

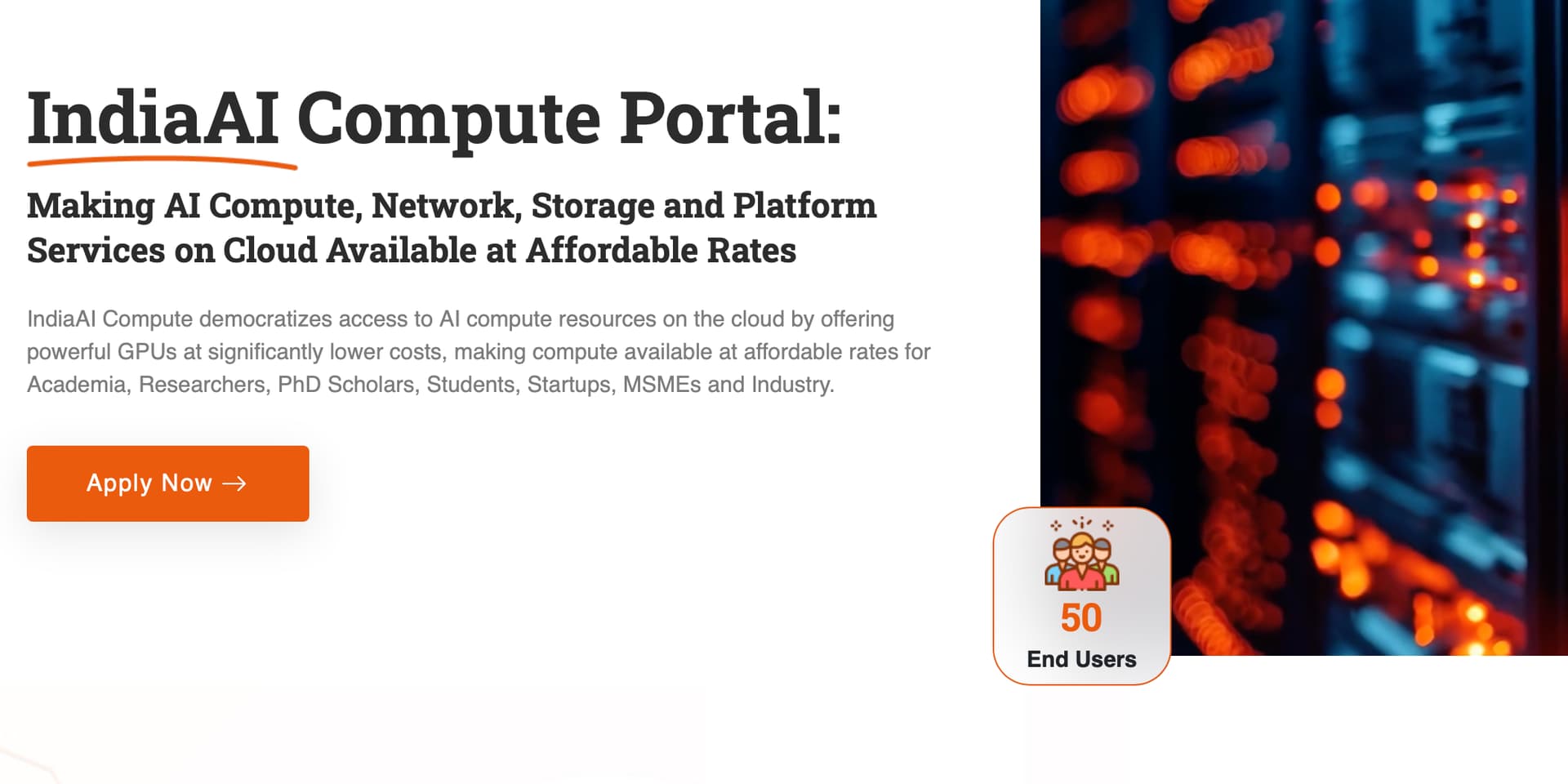

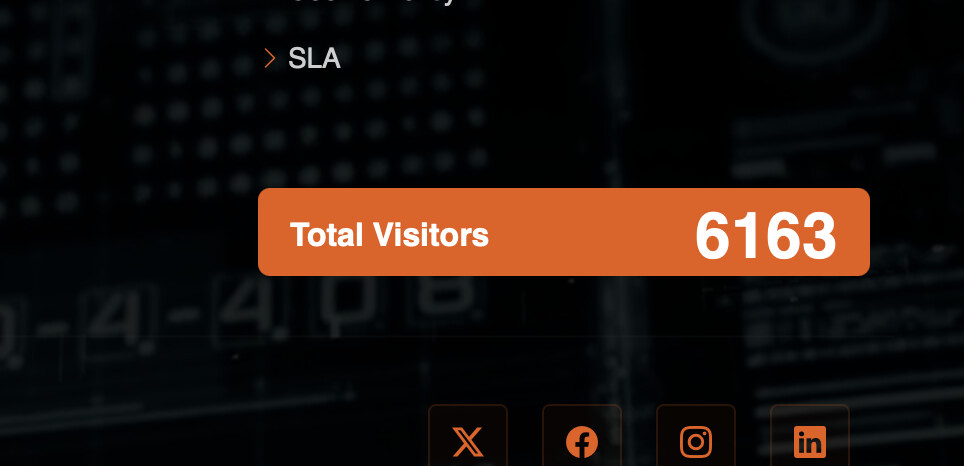

In the recent concall, promoter said that IndiaAI portal has already started and workloads should start coming in a couple weeks.

But on the IndiaAI Compute portal (https://compute.indiaai.gov.in/login), it says only 50 end-users right now. Website visitor count is 6,163. The portal launched on 12th March, 1.5 mos ago. Possible that the number hasn’t been updated yet. Being a government mission, I am sure monthly/quarterly usage numbers will be posted somewhere, either IndiaAI website or MEITY.

2 Likes

E2E Concall takeaways

- Last time I think we spoke we were practically at 700 or so 700 or 1,000 hopper series GPUs. Today including all our GPUs we almost have a GPU capacity of almost nearly 3,700 GPUs. This makes us practically the very largest of GPU cloud GPU installations in India amongst the Indian players.

- We have nearly 100 plus engineers working on our AIML and cloud infrastructure platforms.

- From a data center standpoint we have access to 10 megawatts of data center IT power capacity spread across majorly Delhi NCR and Chennai region.

- All of the software that we built is our practically own proprietary software which wraps around a lot of curated open source software to deliver a platform experience.

- MRR has stayed, monthly recurring revenue has stayed constant from December to the March period. Major reason for that has been that we have been running a lot of trials with larger customers, larger startups both directly as well through our strategic partnership and these are long cycle sales and we felt the need that there is a lot more waiting for us.

- We are working in a market which where it is dominated by two players – so one of them does about $10 billion of revenue and the license cost is almost 4x to 5x higher than what we are charging for our platform. And the other player does nearly $2 billion of revenue.

- FY26E revenue guidance: 50-70% revenue growth

- FY27E revenue guidance: We have built a capacity where the capacity is enough to take us from monthly current revenue of INR11 crores to maybe around INR35 crores to INR40 crores where we are targeting this number to be by end of say March '26 or maybe a quarter here or there. Implies Rs420-480crs annual revenues in FY27E. Can be achieved with existing capacity.

- Capacity growth guidance: So, if we look at like, say next 2-3 years, we would be targeting anywhere close to 10,000 GPUs plus overall on our platform. Today we are at 3,700. So, anywhere next 2 years we should be to add anywhere between 6,000 or so GPUs maybe even more.

- Margin guidance: So, actually our EBITDA this quarter came down to 40% from 60%. Steady state is of course we intend to get back to 60%.

Conclusion

- Revenues: Rs164crs in FY25 => Rs246-Rs280crs in FY26E => Rs420-480crs in FY27E

- EBITDA margin: FY25 59% =>60% in FY26E => 60% in FY27E

- 2.5x-3x growth in 2 years. If PAT goes 3x in 2 years FY27E PAT at Rs141crs and stock is trading at 36.3x FY27E P/E.

- Also over next 2-3 years company plans to increase capacity by another 2.5x-3x for the next leg of growth

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://nsearchives.nseindia.com/corporate/E2E_06052025134229_Updated_Transcript_17042025.pdf

9 Likes

I recently came across an article in The Economic Times that highlights a concerning trend in the AI infrastructure market – the rapid and significant fall in the rental cost of high-end GPUs. A key excerpt:

“The rental prices and margins at which you can rent has significantly gone down. For example, on-demand H100 (an Nvidia GPU) used to cost $11–12 an hour back. Now you can get them for less than $3 from a decent cloud service provider.”

For E2E Cloud, which has positioned itself as a GPU rental and AI cloud service provider, this development could present serious headwinds.

Why This Could Be a Challenge for E2E Cloud:

![]() Margin Compression: With the drastic reduction in GPU rental prices, E2E Cloud might face significant pressure on its margins, especially if customers demand similar price cuts.

Margin Compression: With the drastic reduction in GPU rental prices, E2E Cloud might face significant pressure on its margins, especially if customers demand similar price cuts.

![]() Intensifying Competition: The entry of larger players with deeper pockets into the Indian market could erode E2E Cloud’s early-mover advantage.

Intensifying Competition: The entry of larger players with deeper pockets into the Indian market could erode E2E Cloud’s early-mover advantage.

![]() Capital-Intensive Growth: Despite falling rental prices, expanding GPU infrastructure and maintaining high-quality orchestration layers still require heavy investment, which could strain E2E Cloud’s balance sheet.

Capital-Intensive Growth: Despite falling rental prices, expanding GPU infrastructure and maintaining high-quality orchestration layers still require heavy investment, which could strain E2E Cloud’s balance sheet.

![]() Reduced Pricing Power: If customers can access cutting-edge GPUs from global providers at highly competitive rates, E2E Cloud may struggle to differentiate on pricing alone.

Reduced Pricing Power: If customers can access cutting-edge GPUs from global providers at highly competitive rates, E2E Cloud may struggle to differentiate on pricing alone.

9 Likes

This is in line with the view i had shared earlier - as AI and its usage matures, AI related compute would tend to be a utility, and the profit pools that are now centered around the compute aspect of AI currently (NVIDIA included) should tend to move towards products and services that would be built to harness the power of AI in a succeedingly better manner. The layers above the compute, if you will.

4 Likes