At the end of the day it’s all about earnings. If in coming years company can show strong bottomline then the market cap can show significantly. Investing is all about probability. I had identified it when the market cap was around 170 crores. No one was optimistic about the company and the future prospects. No one knows anything beyond a point and we can only focus on the cash flows and the earnings. Most of the people ignore the cash flows and invest in a borrower conviction. Hope the company does well and reward the shareholders.

4 Likes

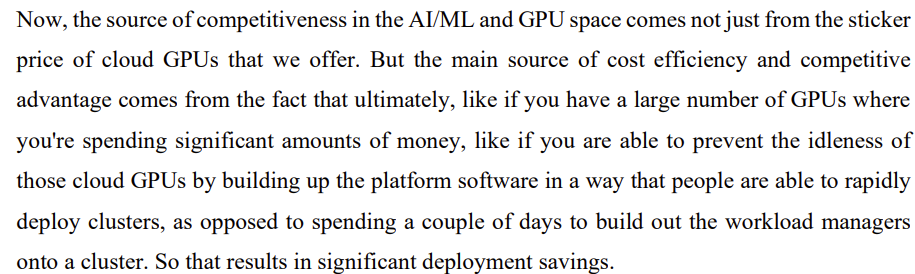

The key value addition happens at the software level. E2E mgmt has mentioned this multiple times-

Software is probably one of the factors which allows hyperscalers to price their GPU instances & cloud services higher than smaller players.

E2E has had its platform operational longer than any other Indian player which gives it first mover advantage. It remains to be seen how it translates in to actual competitive advantage vs new players like Tata communication.

L&T licensing their platform for their own use indicates there is a some entry barrier in creating one from scratch. After all, they have an army of developers in their IT subsidiaries and they could have created the platform themselves if it was easy.

3 Likes

Going to respectfully disagree with the promoters here based on my experience. There are lots of off the shelf open source free workload managers - nVidia itself has built one. All major cloud providers such as AWS, Azure, GC have their own workload manager. I don’t think its going to be too tough for Tata, Jio etc to build something comparable.

There is some scope for reducing costs at firmware level by optimizing the hardware’s firmware to be very specific to the model you are training (thats partially how High Flyer managed to get Deepseek’s training costs down so much) but thats unlikely to be provided as a service as you need something generic so that any model can be trained or inferred on their GPUs.

Ultimately, there are not many software moats out there - even something as cutting edge as frontier models are constantly being disrupted. OpenAI was the leader but now it has several competitors with comparable or even higher quality. It will ultimately come down to execution and the management’s ability to outcompete others in a very tough industry.

6 Likes

Interesting perspective from Aravind Srinivas (Perplexity) on Data Center business https://youtu.be/y5Ewu8wYgqM?feature=shared&t=5970

2 Likes

Interesting

https://x.com/balajis/status/1903700743242326284?s=08

I firmly believe that as AI as a phenomenon grows and matures, AI infrastructure in whatever shape and form would be a commodity and the providers would be utility providers like electricity companies. DeepSeek is the first step towards that direction. The value add would be by smart players leveraging AI the most, for their business. Not just startups creating AI first apps and services, but also ‘traditional’ businesses making the best use of AI, like, how Bajaj Finance is doing.

1 Like

The company is planning to buy blackwell GPUs means there is some immediate capex planned in next quarter..they usually buy in multiple of 128 GPUs

https://x.com/e2enetworks/status/1903326947532226879?t=yVPfvCT33P2nHHsSUtku4w&s=19

5 Likes

E2E Networks boosts its leadership to drive growth & innovation in cloud & AI. With new experts on board, the company is set to scale its presence in India’s digital infrastructure space

6 Likes

4 Likes

This is huge..2000 plus H200 GPUs procured in such a short time… Looks L&T partnership playing out big..I guess it should be minimum 500 cr capex. Anyone, pls correct me if I am wrong here.. privious H200 procurement was around 256.. so around 1700 GPUs would be additional capex…

https://nsearchives.nseindia.com/corporate/E2E_03042025124325_Press_Release_H200.pdf

12 Likes

13 Likes

Executive Summary: E2E Networks Limited Q4 FY25 Earnings Call

Company Overview

- E2E Networks is a leading Indian cloud infrastructure provider focused on AI/ML workloads and cloud GPU services.

- Founded in 2009; public since 2018.

- They have access to 10 MW of IT data center capacity primarily in Delhi NCR and Chennai.

- Currently hosts one of the largest GPU cloud infrastructures among Indian providers, with ~3,700 GPUs deployed.

- They’ve built a proprietary sovereign cloud platform tailored for single-tenant AI workloads, ensuring data security and independence.

- 100 engineers working on AI, ML, and cloud infrastructure.

Q4 FY25 performance

- Revenue from Operations: ₹33.5 crore vs ₹29.4 crore (up 14% yoy)

- EBITDA Margin: 40% (vs. 60% in prev quarter due to higher trials and POCs)

- Net Profit Margin: 41% vs. 12% in Q4 FY24

- Diluted EPS: ₹8 vs. ₹2.4 in Q4 FY24

FY25 performance

- Total Revenue: ₹106.4 crore (up 102% YoY)

- EBITDA: ₹47.5 crore (up 117% YoY)

- EBITDA Margin: 59% (+820 bps YoY)

- PAT Margin: 29%

- Diluted EPS: ₹27.2 (up 85% YoY)

Strategic Highlights

- GPU Capacity Expansion:

- Added 2,048 H200 GPUs recently; these are undergoing testing and will go live shortly.

- Total installed GPU base is now ~3,700; plans to scale to 10,000+ GPUs in next 2–3 years.

- Capital Raise:

- The company raised a total of ₹1,500 crore through two fundraises

- This capital was primarily used to:

▸ Expand GPU capacity (from ~700 to 3,700 GPUs)

▸ Build out infrastructure for Sovereign Cloud and India AI Mission opportunities

- Sovereign Cloud Platform:

- Competing with global players who charge 4–5x more for similar infrastructure.

▸ Large addressable market (global peers generate ~$12B revenue)

▸ No revenue guidance yet due to long sales cycles - Offers a cheaper, India-based alternative with strict data compliance and air-gapped options.

- Positioned for private, public, hybrid, and on-prem deployments

- Strong gross margin potential (~75–80%), with plans to sell globally through L&T partnership.

- Competing with global players who charge 4–5x more for similar infrastructure.

- India AI Mission:

- Selected as a major panel provider under the Government’s India AI Mission.

- The Indian government has allocated ₹4,500 Cr as a 40% subsidy, expected to drive ₹10,500 crore in AI infra demand over 3 years. (i.e., ₹3,500 Cr per year in AI infra demand)

- E2E is targeting 10–20% market share in this initiative. This could translate to ₹900 Cr to ₹2,100 Cr in revenue just from India AI Mission-related work.

- Strategic Partnerships:

- Deep collaborations with L&T, NVIDIA, Intel, and AMD.

- Joint GTM with startups and OEMs to build end-to-end AI solutions.

- Product Initiatives:

- Launching AI learning products for students; aiming to capture 10% of India’s 24 lakh engineering student base. (this is good imo. they’ll hire/ attract good engineers from this pool)

- Marketing & Sales Investment: Increased spending in Q4 to build brand visibility and scale enterprise outreach.

Challenges & Outlook

- Short-term MRR stagnation:

- Revenue plateaued in Q4 due to GPU resources being allocated to non-revenue trials and POCs for large enterprise clients and increased marketing costs

- Sales Cycle:

- Long and variable sales cycles (6–12 months) for enterprise and institutional clients make short-term forecasting difficult.

- Focus remains on long-term, high-value clients rather than short-term revenue.

- CapEx and Funding Plans:

- Future expansions will depend on demand for newer generations like Blackwell GPUs.

- Plans to add 6,000+ GPUs. Estimated cost per GPU at ₹45 lakh implies ₹2,500–3,000 crore of CapEx.

- This may be funded via internal accruals and debt.

- Outlook:

- Targeting MRR of ₹35–₹40 crore by March 2026.

- Expected FY26 revenue to be 1.5x to 1.7x than FY25.

- Sovereign Cloud and India AI Mission initiatives expected to materially contribute from the second half of FY26.

D: Invested

17 Likes

Current Capacity:

GPU capacity 3700 gps, largest in India as of now. 2300 are h200

100 + Engineers on AI ml, cloud infra.

10 Mw data center capacity.

Guidance:

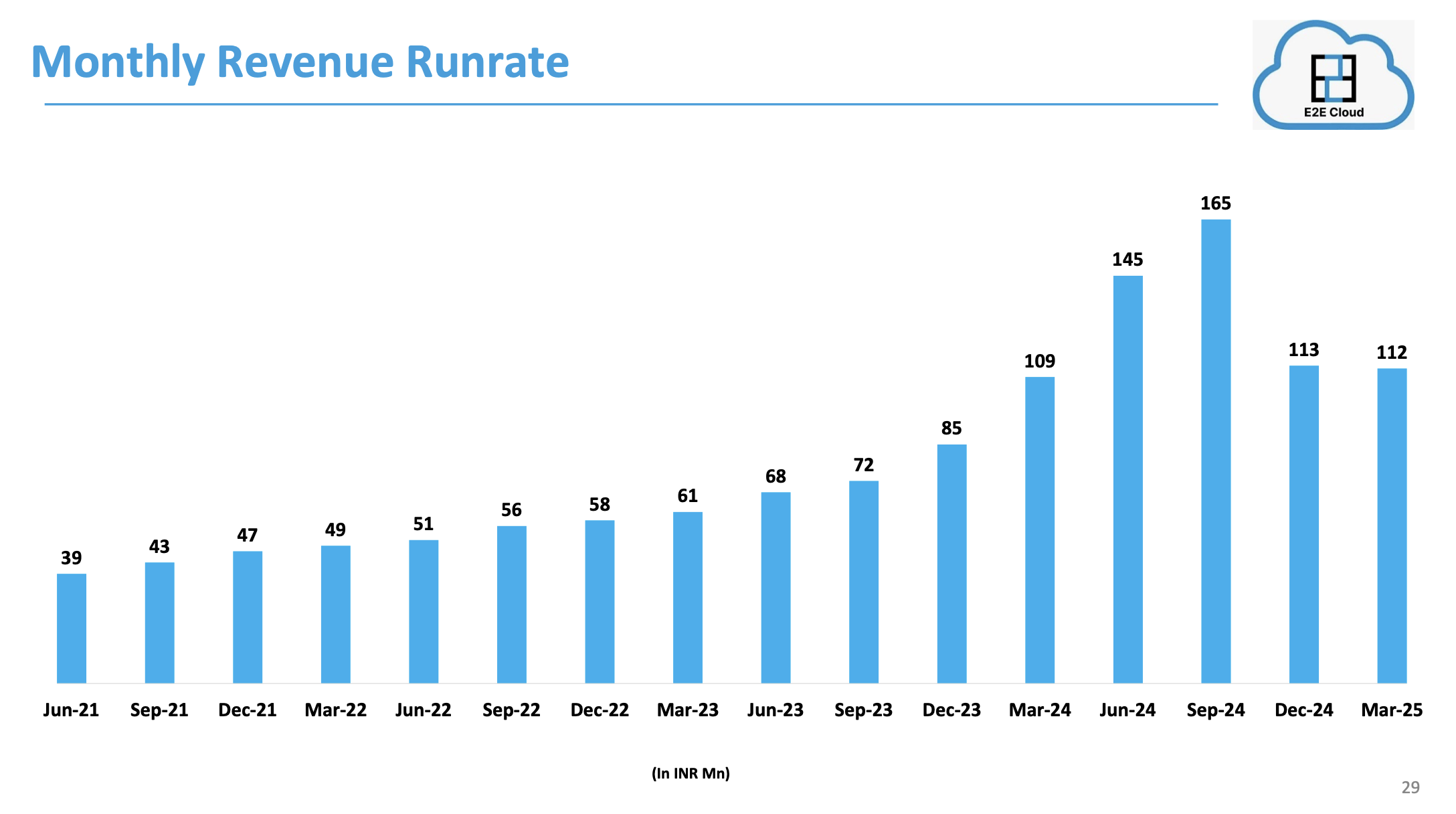

Slow MRR growth in Q4 was a result of a deliberate strategy to invest in acquiring larger, long-term customers by running trials. Due to limited capacity available in q4 there was a loss of immediate revenue growth.

MRR: 40 cr by March 2026 inclusive of India AI mission but Sovereign cloud not included.

Fy 26 and fy 27 capex: May add 6000 GPUs to reach 10,000 GPUS in total, possible capex of 3000 cr using future cash flows + debt route and/or equity dilution.

Intent to get back to 60% EBDITA margins.

Sovereign cloud and AI: Opportunity size is significant but currently not part of guidance. 75% gross margins expected.

Operations Update:

Chennai Data Centre will be live in 2 weeks.

Capital work in progress is for 2000 GPUS, which are being tested in the cluster and not yet given for production.

By Q1 all GPUs acquired so far to go live.

18 cr MRR Capacity utilization as of now at peak will be 40 cr MRR by March 2026.

India AI mission:

Empaneled t as a Major Cloud GPU Provider. Already started work on this, target to get 10% -20 % revenue of 4500 cr outlay in next 3 years. Around 20% discounted compared to street price as lower costs incur in this due to low sales and marketing costs and no Customer Acquisition Costs.

At the peak 900 cr revenue possible by 3 years from now. Margins could be around 60%

LnT partnership:

Will enable e2e for international business for the sovereign cloud platform, will be pursuing bigger deals and bigger customers with a robust sales team due to LnT coming in.

Read below to understand about sovereign cloud

https://www.business-standard.com/markets/capital-market-news/e2e-networks-launches-sovereign-cloud-platform-for-secure-scalable-cloud-solutions-125031100469_1.html

Dscl: Invested no transactions in last 30 days.

24 Likes

Company has officially said this what i have written about the software part. Now it’s just a matter of time. Software revenue Start following in Topline.

4 Likes

Some notes on my latest look at E2E after their results

Concerning decrease in MRR

MRR has fallen from 16.5 cr to 11.2 cr. There are also some global indications regarding a trend shift towards slowing training demand with Microsoft apparently canceling some of its buildouts (though they maintain these are “strategic reallocations” and “remain committed to a $80B buildout”).

Capacity additions

3700 GPUs have a total billing capacity of 335.38 cr. At 40Cr MRR guidance, it looks they are targeting full utilization of their GPU buildout + server infrastructure by end of FY26.

India AI mission

551.75 cr allocated for FY25 but only 173 cr used so far. Not sure if this is due to bottlenecks due to red tape or lack of demand.

2,000 cr allocated for FY26. Unclear how much will be used.

Can’t find any source tracking the expenditure of India AI mission. I guess we’ll only know from the budget docs next year. However, if we use FY25 as a benchmark, we can expect only 30% i.e. 600Cr of spending.

Stiff competition for this spending with lots of other heavyweights also approved - 13 in total including heavyweights such as Tata, Jio, CtrlS etc

Research Reports

JM Financial has an excellent report on the data center industry where all the players are currently private - https://jmflresearch.com/JMnew/JMCRM/analystreports/pdf/Data%20Centers_Entering%20a%20hyper%20growth%20phase.pdf

(Note - This only deals with colocation services which are pure hardware provisioning. Not IaaS which is more the domain of AWS/GCP/Azure/E2E etc. Still an interesting report to go through)

Valuations

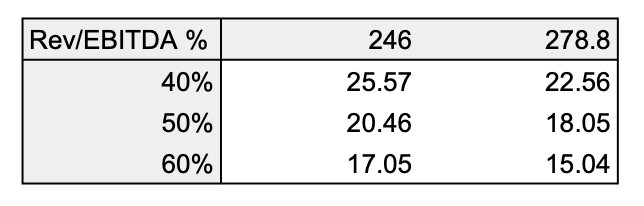

It has been tricky trying to think of how to value E2E. With a large depreciation component due capex attributed to buildout to 10,000 GPUs, EV/EBITDA should be the metric which is around 18 if we include the Other Income line item of 39.43cr and around 26 if we exclude it.

No idea what the Other Income of 39.43 is but I’m assuming it’s interest from the funds collected during their fund raises so EV/EBITDA would be 26 as we should reasonably exclude this Other Income line item.

At 1.5-1.7x FY25 revenue guidance and looking at EBITDA margins for 40-60%, we get a range of 1 year forward EV/EBITDA

Only at 1.7x revenue growth at 50% EBITDA margin does E2E start looking fairly valued on EV/EBITDA multiple. There is some slight upside if you think they do 1.7x revenue at 60% EBITDA margin in FY26.

Disc: Not invested, tracking

15 Likes

@HiteshTinna, You earlier indicated they no longer want to grow asset heavy GPU business. Why are they targeting to have 10,000+ GPUs now?

If you get chance to meet them again, do check what IRR and payback period they expect from GPU investments.

1 Like

That was not what they meant. Basically they wanted to rollout slowly as compared to others as they wanted to keep money to buy and play out various new chip developments that would come out from NVIDIA and the likes while also managing unnecessary depreciation and low starting utilization. But they realised that to incorporate bigger clients, their existing capacity was just too small which is why they decided to do this massive CAPEX. They still have money left to deploy for other chips and they said they could use debt given the good cash flows from such businesses. Based on their concall they utilised the capacity for demos with large clients but was this a strategic initiative or their inbound was not happening as expected?

Invested

3 Likes

Anyone from Mumbai. Here is a chance to meet Tarun Sir one on one. We will get a better clarity of future business and sovereign cloud platform.

If anyone is coming do DM or reply

Thanks

3 Likes

interesting analysis

4 Likes

GPU life is 3-4 years only for the most cutting edge workloads. And I doubt too many enterprises in India will do any cutting edge work?

Am I understanding it right or theres some gap?

1 Like