Below is a tabular comparison of E2E Networks Limited’s financial performance, highlighting key expenses and metrics on a quarter-over-quarter (QoQ) and year-over-year (YoY) basis for the 2nd quarter Financial Year 2024-25 results:

While the results are impressive across various financial metrics, I was hoping to see stronger topline growth. The generative AI industry in India still has a long way to mature, but as this transformational technology is adopted across industries globally, it opens up opportunities for new players—especially those focused on GPU-intensive rather than CPU-centric hyperscalers. This shift is not limited to India but is a worldwide trend. Incumbents like AWS and Azure are also making strides in the GPU space with some exciting innovations. The key reason I believe new entrants can capitalize on this is the evolving usage of technology by emerging companies. Unlike the pre-generative AI era, when cloud computing was a smaller part of total expenditures, cloud GPU costs are now becoming a major factor in business models of tech companies and that might be one of the reason why these companies are becoming more conscious of choosing the gpu cloud provider which gives them more value for money.

As investors, I believe we need to stay vigilant regarding the rapidly shifting landscape of this industry. This could be one of the fastest technological shifts the world has seen. The drivers of this change include rapid advancements in GPU chip technology, improvements in large language models (LLMs), AI Agents and quicker adoption of AI across industries. Over time, the cost of these components will decrease, further driving demand, innovation and adoption.

… bottom line of 19.79% is growing faster than top line growth of 15.03% might suggest e2e is beginning to see scale-advantages work in their favour. (in my prior experience in this business … ) This often appears in items like per-rack-datacenter-leasing-cost, deployment costs and other operating costs increasing linearly even if there is an exponential increase in number of racks deployed. Given the stack is fully built and model perfected, I fully expect this gap to increase in the future as they get more and more of this.

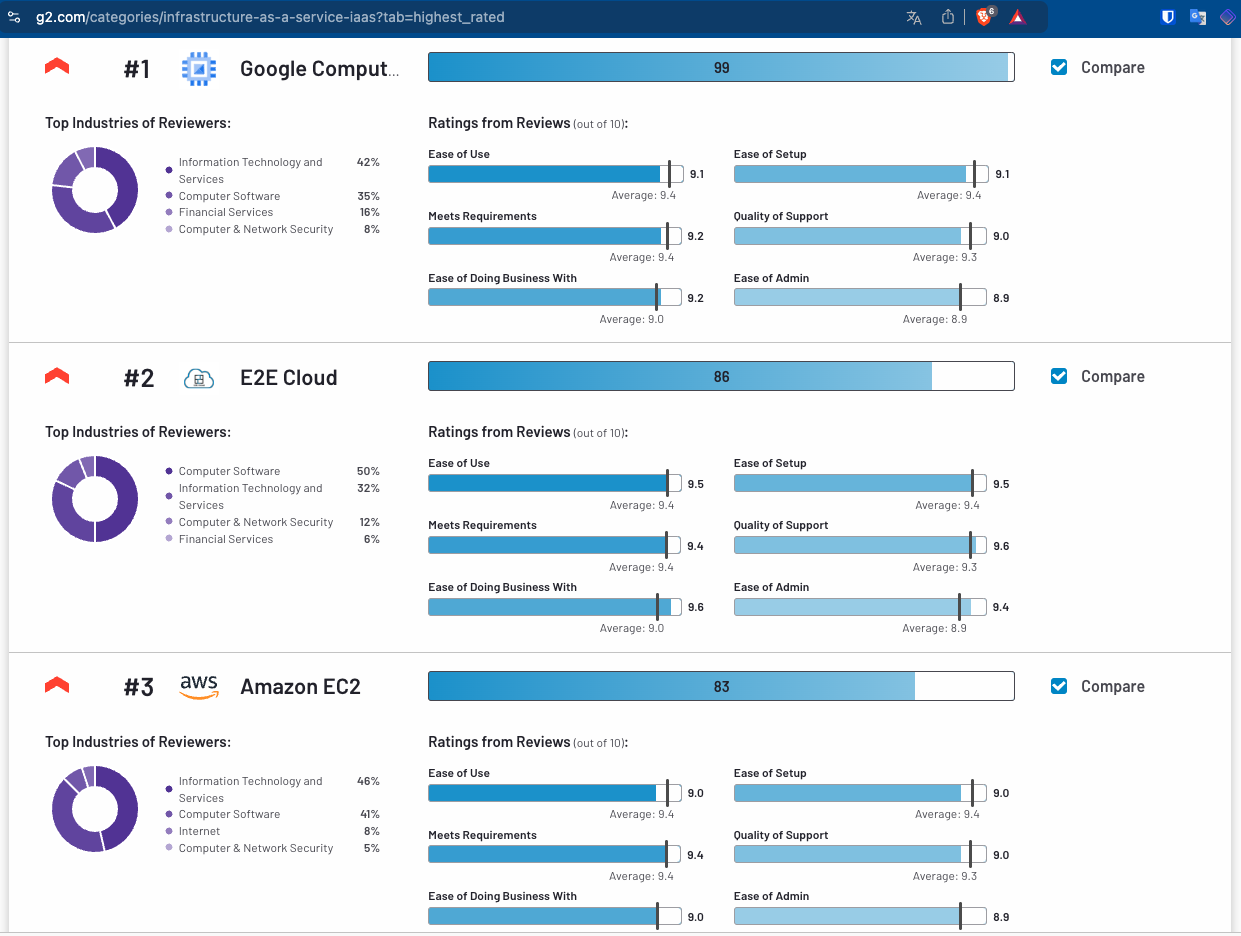

this gives some comfort… but i didnt understand one thing - e2e has better numbers on all 6 metrics than google, yet google overall rating is higher. why?

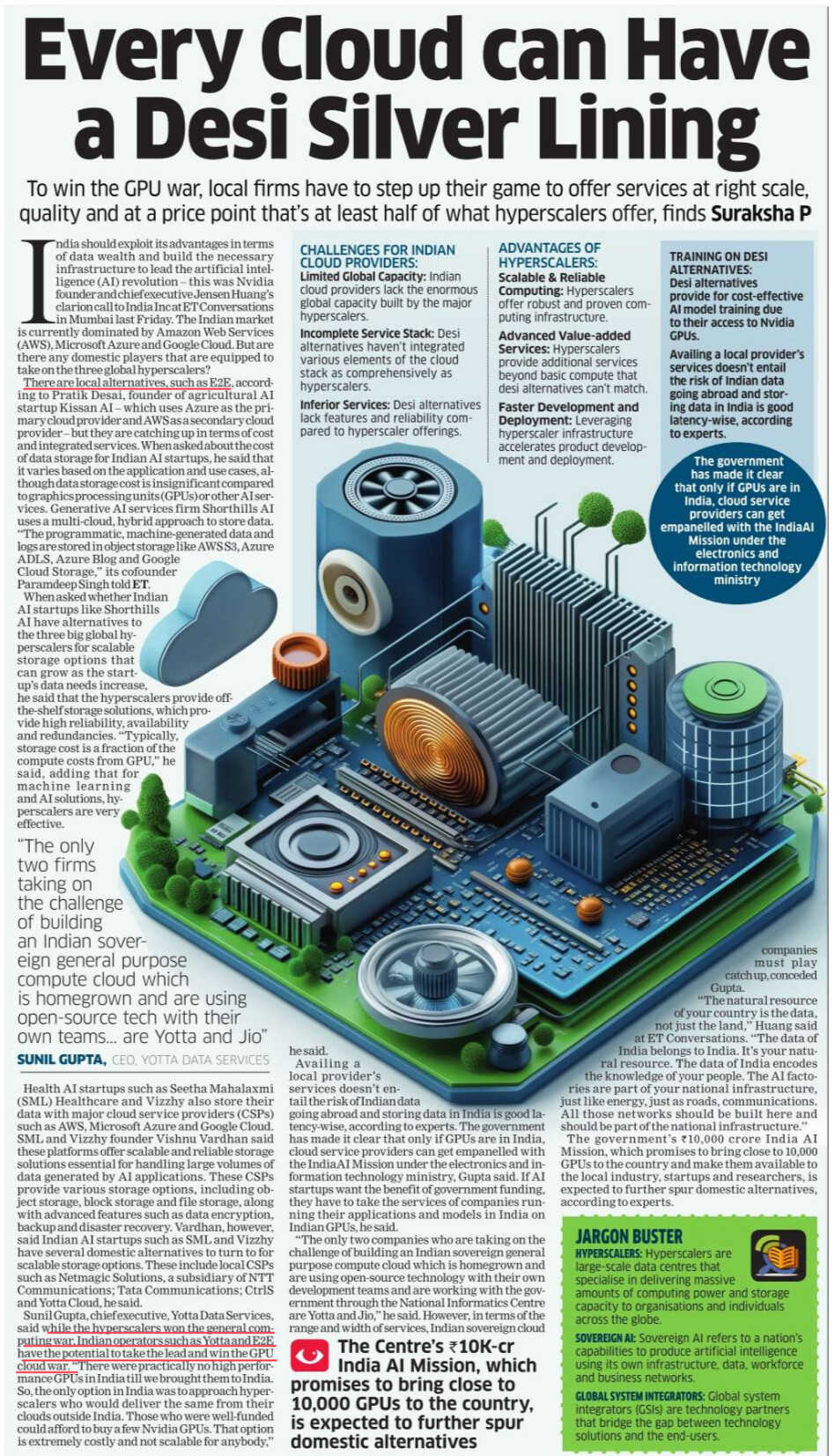

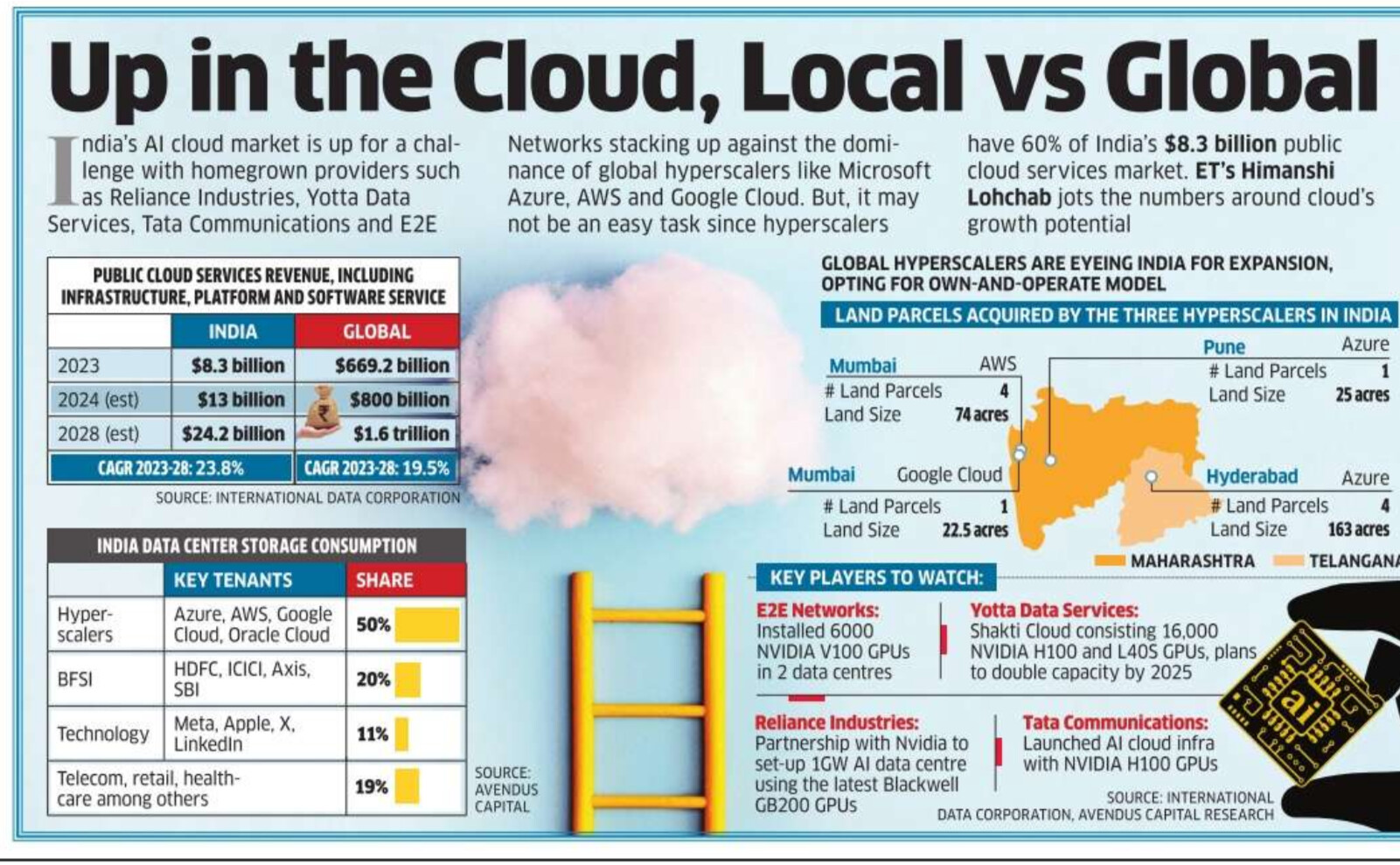

An article in today’s ET. Good round up on AI start up ecosystem , hyperscalers, local cloud GPU providers like E2E and their opportunities & weaknesses in competing with the big 3 hyperscalers.

E2E networks just announced Another fund raise today. I think this time qip will be around ~ 500 cr , price could be 3500 ? double of the last QIP price . Lets wait for the Company to finalize the QIP details.

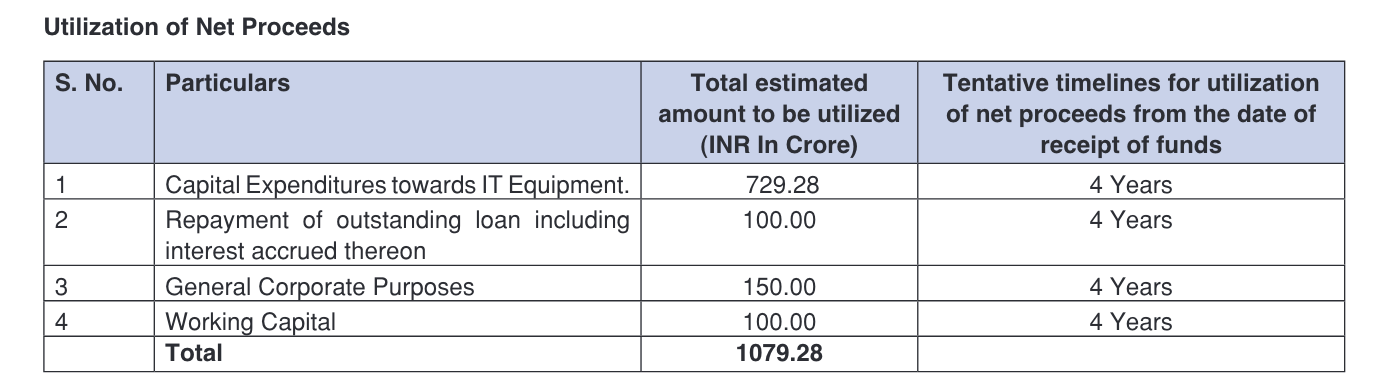

"Preferential issue and allotment of 29,79,579 equity shares having a face value of Rs. 10/- each for an aggregate amount of Rs. 10,79,27,80,032.75 (Rupees One Thousand Seventy-Nine Crore Twenty-Seven Lakh, Eighty Thousand Thirty Two and Seventy Five Paise Only)."

Am I missing something or are the valuations absurd? Aren’t they a infrastructure business that requires capex to grow? The market seems to be factoring in a lot of growth, and definitely the opportunity is huge but can they scale up that quickly without equity dilution or significant debt?

Disclosure: Exited recently due to valuation concerns

My view is that …As long as demand tail wind exists , even basic infrastructure provider will grow at rapid pace and returns will justify capex as margin profile is way way superior to cost of capex . As of now looks like demand shall stay for long in India considering data generation and on the go analytics trends

Interestingly enough, in the latest concall, management was not ready to give any indication about their capex plans for the next couple of years, in spite of persistent questioning by the analyst from Lucky Investments. I quote:

“So we have no upper limits in our mind with regard to how the growth block should grow. It

completely is driven by the demand. So we are able to like set up our deployment in a way that

like we are prepared for large capacity expansion.

But obviously, we keep building the capacity as the demand keeps coming in and as the

customers keep getting signed up onto our platform. So based on that velocity, we keep on

building the infrastructure. Now, obviously, there is some sense to this fundraise.”

I understand being ambitious in wanting to capture as much of the demand you can, but in business you do plan your capex, fund raising, etc couple of years in advance right? Can’t be open ended! I found this part of the call interesting and perhaps a bit strange.

@BuyRightSitTight I also found the management’s responses during the conference call very evasive - be it on capex plans or growth. It seemed as if they were trying to hide something.

They are not a pure infrastructure play. This is evident from their margin profile which is quite contrasting with Netweb. They are compute provider. Their value addition happens one layer above infrastructure. They have productized all this infra to sell. For example, instead of just giving you server where you install your database, E2E will give you easy DB setup without having to think about the hardware level stuff. This is why they can dictate the margin they do.

The reason for the extreme valuation is the cash infusion they are doing to get more fixed assets(computer hardware), and they being focused on high density compute allows them to pack more compute in the same racks. Last concalls Dua said, the Data Center costs them approx 10% of the revenue which is quite low if you think about it.

They had 200cr fixed assets in March 2024. Then additional 400 cr. which is now operational (announced on Twitter). Finally the new 1400 cr. coming in bringing the total assets to 2000cr. (200 + 400 + 1400). They may not invest all the cash on computer hardware, so this 2000 cr is the upper limit. They will realize the money from L&T deal by 31st Dec, 2024 and take a quarter to acquire and install everything. If we take it to be true, that means from Q1 FY26, they can have up to 2000 cr assets vs 200cr in March 24. 10X assets → 10X sales → 10X profits. (assuming they can sell all of it.)

With the current PE of 300, if we assume correction to 150 PE for the next year, the 10/2 = 5X movement on the stock is possible. Of course, this assumes the stock will command 150 PE. If it commands 75, that gives 2.5X for FY 26.

I am concerned what the L&T partnership will entail and definitely need more info on it, but I think overall E2E has shifted gears and it’s still going to grow aggressively.

but utlising 729 of the 1079 for fixed assets. Further the 327 from the secondary transaction will go to Tarun Dua personally and not to the company, so the return will be more tepid. But a 1300 cr fixed asset is still 6.5 times of the fixed asset end of FY24.

From your buying price it’s already 90x or so for you . so great to see such conviction and pretty detailed work with the understanding of the business.

Does it matter to you sir, even if it does not realize all the potential upside after this deal?