Please read the post above by “salonihemnani011” in Sep 2020 - The foreign currency loan at sub 5% interest and thus interest cost will not be significant after the plant commission as well.

2 Likes

https://drive.google.com/file/d/1zXeOtYx4hH6mi2E0TlVqYcRQb2txE8kT/view?usp=sharing

Sharing audio recordings from the AGM, some of answers regarding business and competition in there.

From volumes one can guess some part of ex-promoter selling(Dashratbhai) is coming at higher levels, need to see how much he is left with at the end of the qtr.

10 Likes

@Donald

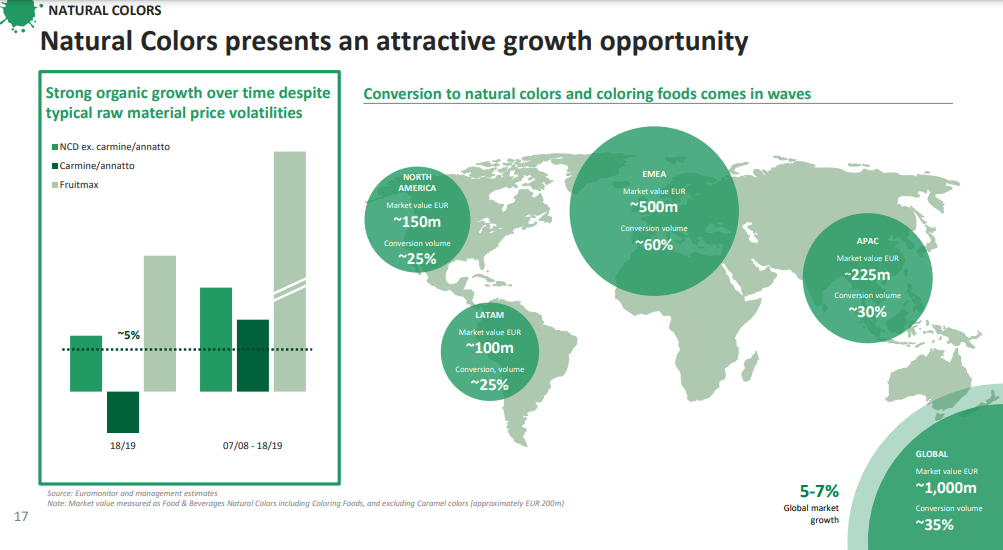

On the Addressable Market size of Food Colors market (natural + synthetic), the best source of the overall market size comes from CHR Hansen’s FY19 roadshow presentation (Fruitmax brand - Natural Colors Division)

Based on above slide:

- Total Market size is EUR 1 Billion and growing at 5-7% CAGR.

- More interestingly is the conversion volume from synthetic to natural of 35%.

With respect to conversion volume found the below slide from Frutarom - Jan 2018 ppt (before it got acquired by IFF)

Source: https://mayafiles.tase.co.il/rpdf/1144001-1145000/P1144574-00.pdf

Does it warrant some concern?

Googling various market research reports give inconsistent figures for the current market size.

The global food colors market is estimated at USD 3.88 billion in 2018

The food colors market size was valued at $2.1 billion in 2019

The global food colors market size was estimated at about USD 3.9 billion in 2020

Roha Dyechem has done 300 cr capex due to be completed by March 2021 and commercial production to begin in FY22.

Source: Rating Rationale

7 Likes

Shareholding pattern came out and it shows no change in promoter shareholding, so entire price volume action post results happened with 2 large individual investors acquiring stake from retail & clearing members.

I checked with the management on the Dahej Plant and the update is that it has not been commissioned. Company is expecting to start by April end subject to Covid.

5 Likes

Mona Laroi - looks like connection with Oldpine Advisors

Retail have reduced ~2.5%, clearing members ~1.9%

2 Likes

Anyone who met management or from nearby destinations who might have any update on the Capex commissioning?

Meanwhile I reached out to a food colours dealer and per him demand seems strong, he reached out to the company to place a big order and was told that they are fully booked till June end.

12 Likes

Subdued results. Seems RM escalation has hit them hard.

Regards,

Raj

Disc: Invested

1 Like

Why interest cost is higher on qoq.as new plant not started yet , so interest cost sould have been capitalised rather than expensed . Anything am I missing?

Yes, it’s puzzling as to why the interest cost has tripled QoQ even though the plant was not commissioned till the end of the quarter.

Also looks like they had 5crs of inventory gain owing to raw materials price increases. Without this, their margins would have been even lower. Whether they are able to pass the higher raw material costs is a significant concern. Though according to me they should be able to pass them as food colours comprise a very low proportion of the costs of the end product of their customers.

3 Likes

As per last year AR the Citibank term loan mortarium was ended march 2021,so from q1 onwards they have to start pay interest , thats why q1 interest cost higher

4 Likes

Was the entire capex funded from citi I.e. loan of around 120 cr for new plant (As per management commentary) and going forward can we expect more interest expenses as more money should have been borrowed in last one year ? Also wasn’t the management funding capex from overseas loans?

As per 2020 AR 40cr term loan is taken from citi bank at 3m USD+2.2% interest which work out to be around 2.5%. and another 40cr from hdfc bank which is at interest of MCLR+0.95% which is around 9% . Waiting for 2021AR to check from where the other borrowing coming into.

4 Likes

Commercial production started in dynemic products , company disclosed in exchange notes

1 Like

Hi all

As per the company’s announcement (https://www.bseindia.com/xml-data/corpfiling/AttachLive/ed04672e-28f7-4228-82c1-97fb1478cd98.pdf), capex of INR 150 Cr is expended towards a capacity of 2760 MT.

Couple of questions:

- CWIP as per Q4FY21 results is INR 194 Cr - so what is the status of the remaining INR 44 Cr?

- Is this 2760 MT capacity for food colours only (i.e. no intermediates).

- As per Sahil’s post above (post 113), Dynemic’s current food color capacity is 2950 MT - so effectively, the company is doubling its food colour capacity by investing 150 Cr? Current Gross Block is 34 Cr - so is the company investing 4-5x current Gross Block just to double its capacity? I presume not, suggesting a good chunk of INR 150 Cr is going into intermediates which is not reflected in the 2760 MT capacity increase.

Would really appreciate if you can help reconcile the current capacity + realisation numbers to the capex and upcoming capacity + realisations.

Edit - found a few answers based on the other thread which has a lot of info.

So total Capex is being used to double the food color capacity plus manufacture intermediates. Based on the company announcement, only the FDC manufacturing has gone live. Within the capacity for intermediates, 60 pct would be sold out to external third parties while balance would be for captive use. Appears quite a few of these intermediates are not commodity in nature, but it remains to be seen if the company can actually sell these products.

Disc - invested.

6 Likes

one more question on this capex is company’s peer Vidhi has planned capax of 60 Cr for capacity expansion of 3X from current capacity of around 3500 MT then why dynemic has incurred 150 Cr for just capacity of 2760 MT ?

3 Likes

Q1 results look good on first sight. Revenue up 2% sequentially, EBITDA margin at 22%.

3d53c823-db0b-4b5d-ac95-01b5cea93d88.pdf (bseindia.com)

Need to understand why interest cost and employee expenses reduced from Q4FY21 to Q1FY22. Also, need to see if the recently live facilities will start contributing to revenue from next quarter.

2 Likes

Can someone help me understand the Share holding pattern?

At first glance it seems that the promoter holding has reduced significantly by 6%

Dashrathbhai Patel has gotten rid of his entire stake in the company it seems.

Is this a cause of concern?

(Disc: Not invested, on my watchlist, trying to learn more about the company)

1 Like

Please share the AGM notes if anyone attended. I heard that it was quite informative.

2 Likes

Great results from Dynemic Products with topline growth of 44%(finally!) and company moved from loss to profit, bottom line should further improve with capacity ramp up.

Management indicated in AGM that every qtr from now on would be better than the previous one with 70%utilisation of Dahej by financial year end.

(Disc: invested)

10 Likes

I had a brief chat with management in the company, the key message I got is this:

- we have resolved all production issues and the focus now is on increasing sales

- we have grown every year since start of the company in 1990s, only exception is current time as COVID led to cost escalation and some very low demand last qtr

- demand situation has turned positive and we only see growth from here on

- personal message to me was don’t mistake selling stock, wait for 2 years

11 Likes