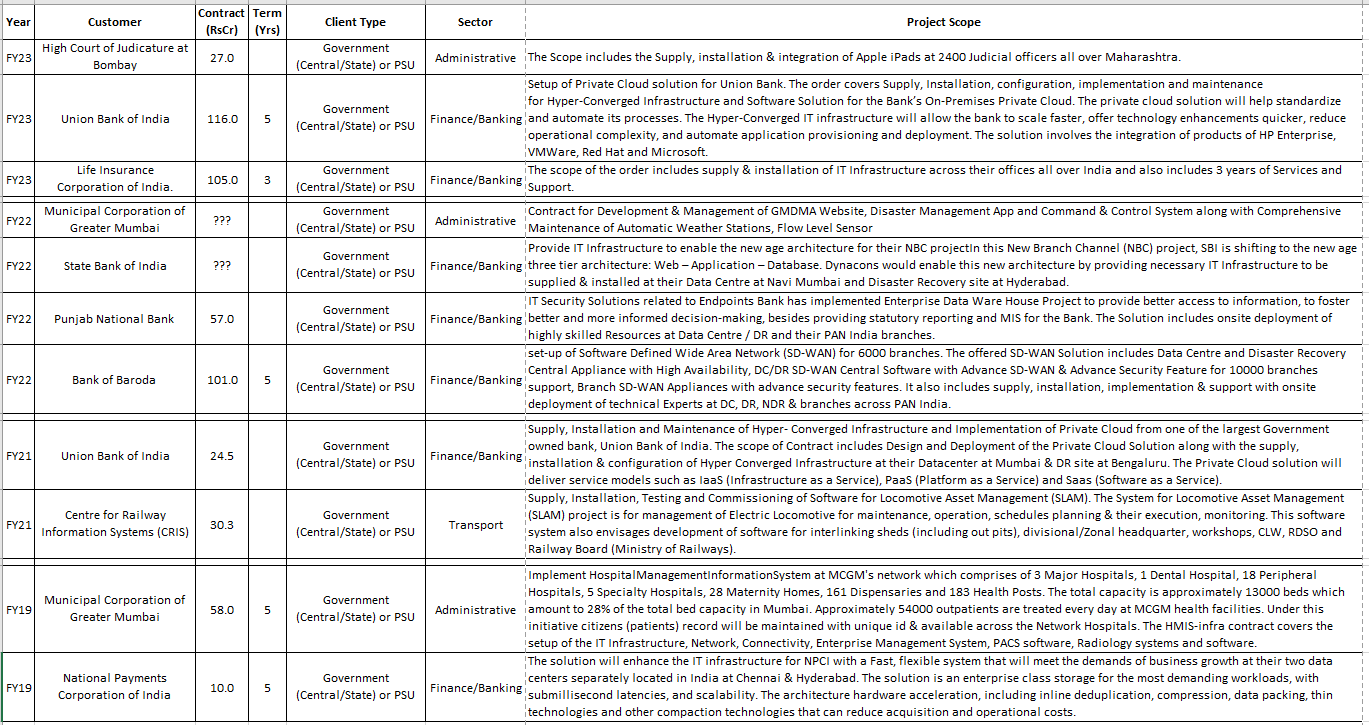

I went through the past few years of AR to understand the deals undertaken by Dynacons. Since FY19, almost all contracts which found mention in AR are for Government (Central/State) or PSU type entities (primarily B2G). Also ~ 60%-70% of these customers fall under Finance/PSU Banks category.

Most deals are for setting up/improving IT infrastructure as regards to Data Centers, Private Clouds, Data Warehouse/Storage etc. Details below;

There is probably a bidding process to win these contracts and the qualified bidder with lowest price likely wins which is reflected in OPM of 4%-6%- range. From a competitive dynamics standpoint, both the Customers (Government entities) and Suppliers (MNC like Dell, HPE, Cisco, IBM etc) have strong bargaining power.

Does anyone knows if Dynacons also provides services to private firms looking to setup Data Centers/Cloud/Data Warehouses etc? Any clue on what % of revenue is recurring owing to ‘service and maintenance’ contracts once the infrastructure is setup?

While reviewing this company, I felt this is like one of the company I worked for in the past and ceased to exist due to merger.

Until early to mid 2000, we had old CMC Ltd in government sector catering to many organisations in Govt and private . This was disinvestment Candidate under Vajpayee Govt and Tata Sons acquired a majority stake, later handed over to TCS and over the years merged with TCS, delisted and ceased to exist.

I think after CMC exited the low OPM Equipment supply, hardware/network customer service and in teens OPM System Integration, no big player went in to this space. (I may be wrong and like to hear views opposing this). Even when cloud infrastructure came In to being, OEM agnostic big players were not there in market due to low OPM business. I feel, DSSL is agressively growing in this space bagging both Govt and private orders . TCS was not keen on these kind of business from the time Mr. Ramanan came as CEO and later merged it to TCS, delisted the company. Most of the order list you posted and what I see in disclosures looks like what I see in late 90’s for CMC Ltd.

Edit response to below question.

Equipment supply and domestic IT infrastructure management will be low OPM business due to completion from small local.players who will have some knowhow and willing to sell 2 to 3% margin. So companies like DSSL will flaunt their ability to manage large orders, but still will lack commanding very high OPM as many will try to do this business at 5-7 or in some cases even lower percentage of OPM. So I think they command only 5-10% OPM in the business they are in, so should not be a concern. There’s much space is there to grow in that range as big organisations need end to end ownership by their IT partner.

Until they target export business or expand to another domain low OPM will continue. But as of now, they seem to have an edge in what they do and there is scope to grow. So trying other overcrowded IT options may be Diworsification .

Let us wait and watch

Disc: Invested 2% at higher levels than current while learning about this and tracking as the organisation is growing fast.

And this is why experience matters. Appreciate you sharing it James.

One more thing it does is to open up a possibility or DSSL to be involved in a merger of some kind. Correct me if I am wrong.

The composition is surely leaning more towards the Govt projects. And bagging govt projects is well, a Skill in itself, speaking from personal experience.

If a company is capable of bagging govt projects ?

It surely knows something or does something right - personal opinion.

Adding to above, and keeping the above information in mind, how would a name like DSSL go about increasing its Margins ?

EDITED : Got the answer to my question in the above reply from James.

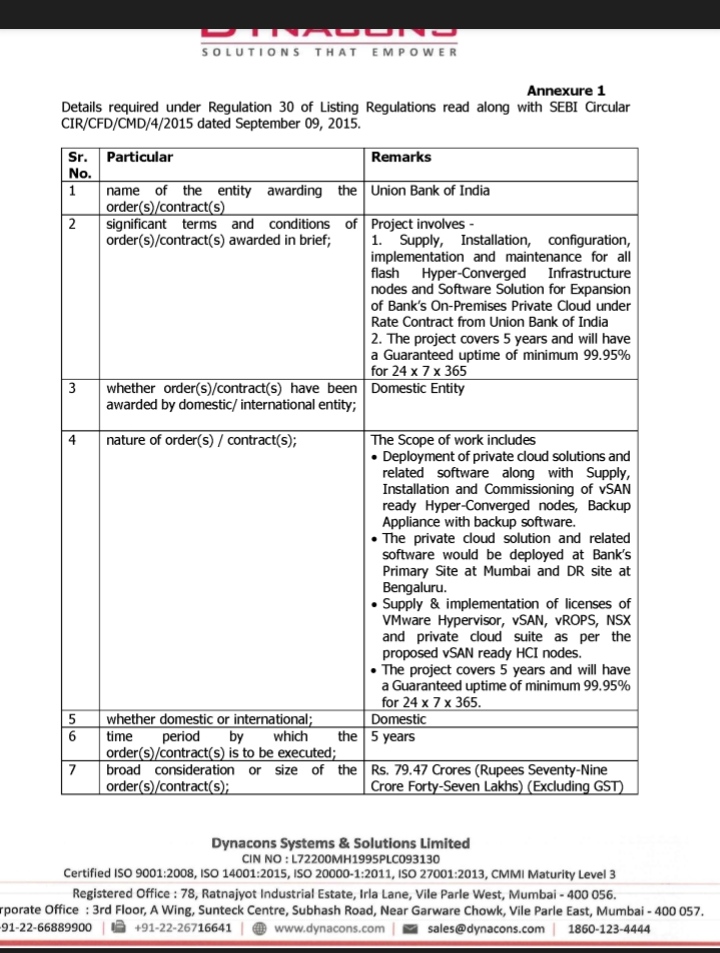

Dynacons Systems & Solutions Ltd has won one of the

prestigious contracts worth Rs. 106 Crores for Supply, Installation, commissioning and O&M of PKI

Solutions, IT Infrastructure Components and Connectivity Services for e-PASSPORT PROJECT. 6c69e26c-cc46-4c82-9c3b-2a1c276b253f.pdf (2.0 MB)

Another Contract Win, and from an entity promoter by govt of Gujrat.

No reason to beat around the bush and try to understand “why and how DSSL wins such projects, & can it do it again?”.

For your product to be sticky in the realest sense ? it has to be low or lowest in price.

Within that price it has offer what others are offering.

But you also have to be known - that you are the one offering it at a lowest price, so that is where marketing and other such promotional activities come in, but for our company that it, probably, its connections.

This ends up creating a cycle, where the more projects you win (because you have the lowest cost), the more you are known, and the more you can sell.

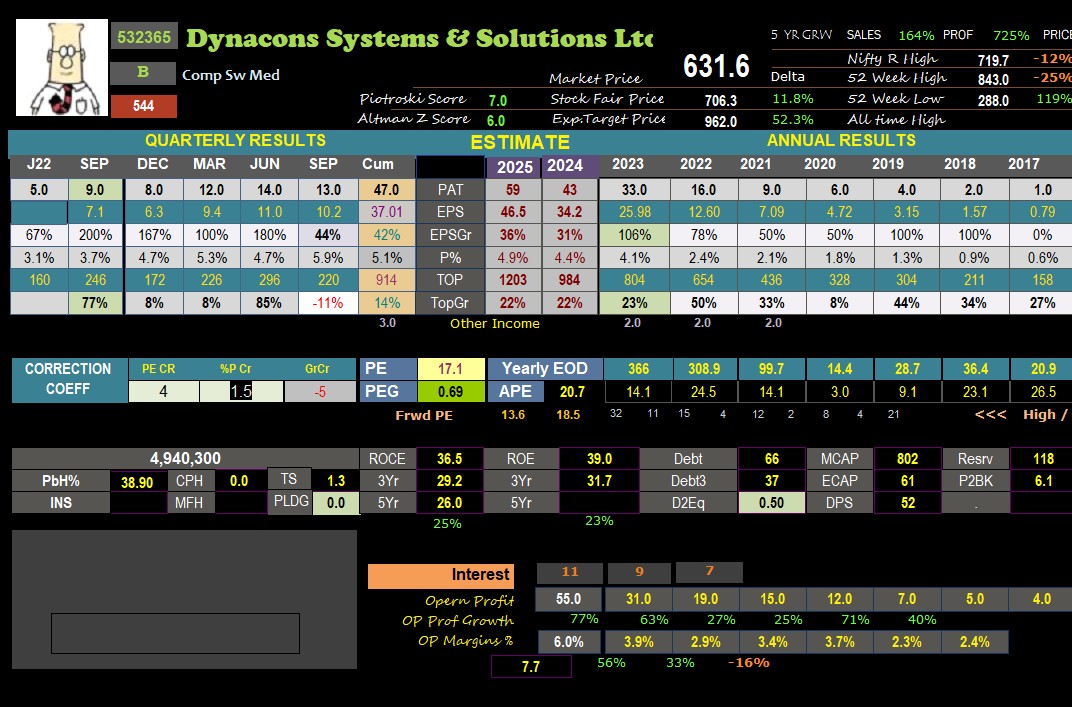

By today I booked profit and exited, to release money for another buy. I may be wrong in quickly exiting…But I usually try to move in and out when I think most of it is priced. I missed the bus also multiple times due to this. But in small caps where we don’t know lot of information, I think that helps me increase my PF size. If this quarter results are very good, I may buy again by looking at PE then.

Nothing wrong I can see with the company. But less tracked company I trade often.

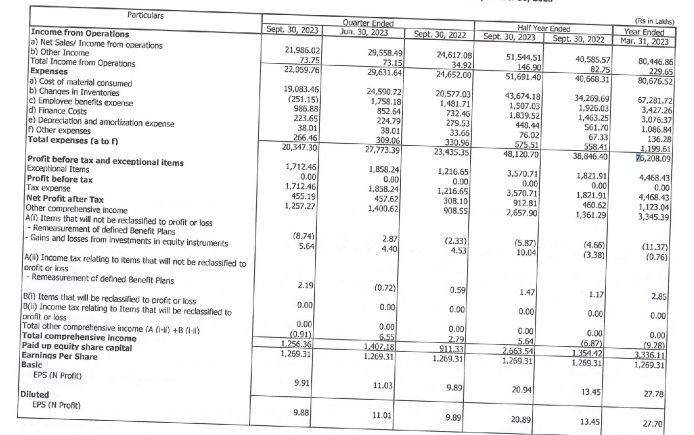

Just before 30 minutes or so, DSSL Q2 result is uploaded on BSE. The YoY result is good if we look at PAT but I didn’t understand why EPS stood the same, there is not split or bonus issues and share capital is same!! If we consider EPS only then the YoY result is flat…

If you look at the half yearly PAT and EPS, and the YoY PAT then the numbers are fantastic, but YoY EPS is baffling me as well. I am relatively new to Fundamental Analysis. I looked and there is no bonus/split given. Can some experienced hand help us understand the EPS part. Per screener there are a total 1.27 Cr shares outstanding which matches the figures at BSE and NSE.

Dynacons has established a subsidiary dedicated to 24/7 information security monitoring. Named "CyberconsInfosec Private Limited”, this company will serve as the security operations center and will serve as the central hub for advanced threat detection, incident response, and 24/7 monitoring services.

This should help them augment their security and surveillance offerings and will further help them establish an annuitized business model.

I think the reasons for low cashflows is because its major customers are PSU so high receivables, I think its receiving high orders because of upcoming election and the government’s push on capex which has led to IT upgradation, looks like a cyclical company with very little MOAT can be a good play for next 1-2 qtrs.