Very apt explanation about Dreamfolks business…Though building platform is not that great moat but as you have explained. bringing consumer, 100% lounges and most of the card issuers of the country onboard is certainly a nice moat…

What I observed during latest concall that Ms Kallat’s very mature answers, no over promising and I think she learned lessons from the last rout on the market…one example is she cautioned about revenue growth as banks started differentiating between low and high spending consumers…and my take is that this is a wise move business wise as they can milk more from limited supply of lounges…

One more growth area they have started this quarter is tying up with nationwide salon chain…as personal grooming is catching up, this business will pick up more than golf is what my guess is…card issuers may have one more choice to offer of salon access instead of lounges…that way dreamfolks can add significant no. of touch points…On cnbc interview, Ms. Kallat also desisted from guidance about national and international revenue mix in the future…

Regarding new competitor entering the market, that most of us worried about, my guess is that as most of the lounges already choke a block , getting incremental business is going to be tough and hence not very mouth watering scenario for new entrant…and also pace of coming up of new airports and lounges is going tobe tardy…though great ROE and ROCE, scaling up will be difficult and it may be a moat in itself…competitor like priority pass is already there…

Though Aditya Birla MF and Small cap fund completely exited during this quarter, Mark Mobius has added this stock…

Uncertainity is the name of business and I’m optimistic about

how Dream’s international business and new age business like golf,salon,visa and other businesses fair in the immediate future…management says all these businesses commands higher margin.

I have a tracking position around 550 and I think its going to be unique and exciting business…

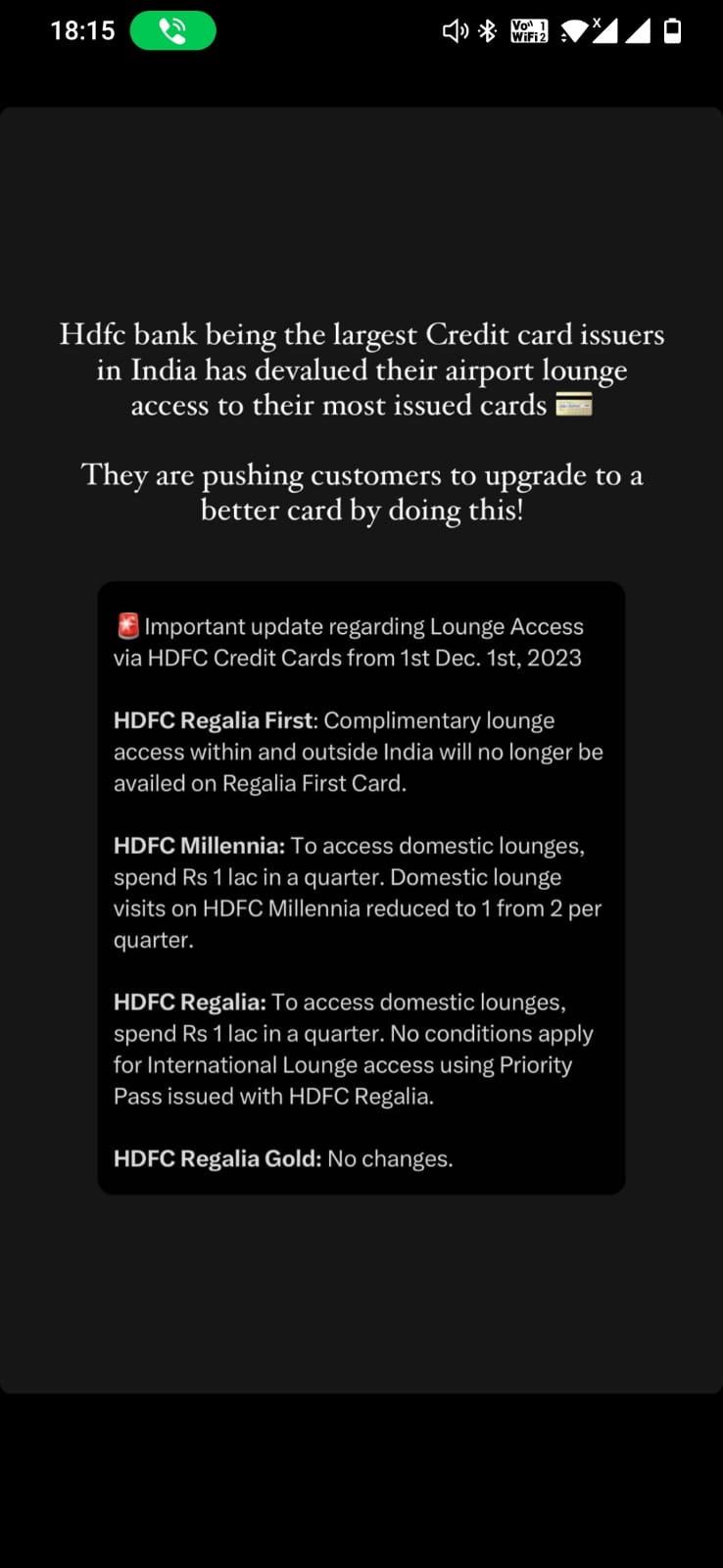

Hdfc putting restriction for lounge access & that 1 lac limit per quarter. I think, HDFC is No. 1 in terms of credit card market share.

I was inclined to buy dreamfolks but such news puts question mark about volume growth (degrowth ?).

Very transparent, clean and to the point - no manipulation or beating around the bush

Excellent Leadership !!!

Few anti-thesis points:

You may have come across in social media platfroms that the Lounges had big queues. I assume that most people were going there just because it’s available for free and I believe not many would go if there’s no free lounge access option.

I don’t think many of them would shift from current cards (500 AMC ) to premium cards (1500-2000 AMC) just to avail the Lounge access benefits.

Let’s ask ourselves the following questions:

- Where do I and my peers (colleagues, neighbours) stand in terms of earning spending ability (top 5% in India, top 20% in India, etc…)

- Am I (and my peers) willing to pay 1500-2000rs AMC for a card just to avail the Lounge access benefit ? ( If I’m in top 20% and not willing to pay then people below 20% are also not willing to pay, and same for top 5% and vice versa)

- Am I going to /willing to spend 1-1.5 lakhs in a Qrtr to avail Lounge access benefit ?

From my limited understanding people are taking different Credit cards to avail shopping benefits (1.5% or 5% reward points) and the lounge access is not a deciding factor. So, I believe people will just let go of lounge benefits

From my above anti-thesis I believe that the revenue will not grow beyond 50% (not CAGR) in next 4 years and stock would not reach it’s ATH of 847 any time in next 3-4 years unless the contribution from their other business vertical (leasing their software to othe cos etc.). and I’ll not be buyer in a business with no growth at 35x P/E

Disc: My views are with limited understanding and no holding in the stock

Reflected on your analysis. Considering that fact that a Plate of Dosa and Coffee can cost Rs 350-400 in a Domestic Airport, an annual fee of Rs 1000-1500 for a premium credit card that offers free Food (in Lounges) may still be a viable proposition. And Indians are very good at doing these calculations.

Have also seen that some Lounges have created an extension to acommodate the surge in demand. Despite this, some people are not able to enter the lounge due to huge rush. In Mumbai one Lounge does not allow people to enter earlier than 4 hour of flight takeoff (should improve footfalls). So even if some banks reduce the eligibility and the numbers don’t drop substantially where Lounge capacity utilisation falls, it should be fine.

The current trend should also lead to creation of Premium Lounges (For Business Class etc), where the freebie seeking crowd is not allowed. That may lead to incremental revenue for DFS.

Disclosure : Invested.

Partially agree with your views, but it all depends on how much and where people want to spend.

The views I’ve shared and other 2000+ stocks in Indian market would allow me to deploy money in other opportunities compared to a Co that’d degrow or slow down in growth (as per me)

Market is dynamic because we have both type of views.

For banks, free lounge access is selling pitch for their card. For consumer, it is also beneficial provided card is LTF. Majority people accumulates as much as new card if it is LTF (Either to use it for bank offer or use for lounge access).

Now think of scenarios:

-

Avg. middle-class family who does once a year trip have multiple CC, will try to explore it lounge access even if they don’t want to eat much. Who doesn’t want freebies?

But now same person, if they need to either pay 500/1000 AMC charges & to meet criteria of spending, they might avoid going in lounge. Also if they are with family, they need 2 separate cc for husband & spouse to enter in lounge. If either of them don’t have access, they might avoid lounge. -

Frequent fliers will definitely apply for more cards in their bucket so they can have access.

-

One positive note in future - Bcoz of reason no. 1, less crowd or waiting in lounge then few other people will join the kitty who have access with card but avoiding due to mad rush.

Also in hdfc mail, they have written after achieving 1 lac spend they need to login to smartbuy portal & then generate voucher code which they can use directly at lounge without swiping card. So does it means, they are bypassing dreamfolks by doing so?

The root cause of why you are seeing an increasing number of Banks cut back on complimentary Lounge Access is the cost that has gone through the roof over the past year and the associated commotion at airports as well.

As per Dreamfolks, about two years ago, on an average they were billing the Banks INR 600 per visit to the lounge this price per trip has shot up to INR 990.

Very interesting interaction from the Concall transcript

Moderator: Thank you. The next question is from the line of Tarbir Shahapuri from Nidara Capital.

Please go ahead.Tarbir Shahapuri: Hi. Thanks a lot for taking the question. You guys have emphasized a lot on the technology that you have developed. I am struggling to kind of understand what exactly is the

technological edge and if you can just help me with how much money you have spent to

develop these? The technology, the platform over time that would be really helpful.Balaji Srinivasan: The way to think about it is that banks basically use this as a way to administer the benefitsthat have been given to the end consumers, and this is the main platform on which all the

usage, the spend, and everything is getting tracked. So, there are two elements to this. One

is the interfacing with the client such as a bank or a network and on the other end is the

access mechanisms that is deployed at let’s say a lounge or a golf course or spa outlet or

any of these locations. So, it is an end-to-end platform that gives the banks the ability to

manage a card program. So that is the layer one of it and as we mentioned in this call as

well earlier, banks are using this technology to also drive a lot of their spend based models

and the usage-based models. So, they are able to carve out or identify segments of users that

are profitable for them or consumers that are not good for them, etc., etc., and do a

differentiated benefit in practical terms. So, the idea is that this becomes a long-term

solution for them where they are able to also launch new products in this tech bit. So that is

our core strength, but from an end consumer point of view also what is interesting is that the

access mechanism such as for example banks are taking our technology integrating this into

the bank apps and that also then has a consumer side to it, but the consumer does not really

realize this is our tech because it is probably branded as somebody else’s tech. To give an

example, if you go to any large metros today there would be some or the other mechanism

to do a kiosk check in for a lounge. It may or may not have a DreamFolks branding on it,

but that tech is actually given by us. So, we do end-to-end tech service for both banks, so

everyone in the ecosystem we are giving them a solution.

Tarbir Shahapuri: And if you can help me with what is the total cost that you have spent to develop this

software or platform you call it.Giya Diwaan: We have actually developed it over a period last four to five years. We started way back in 2017-2018 and slowly and gradually new capabilities/stacks get built in. If I just put a

number to so far what we have invested probably somewhere around Rs. 5.5 Crores is what

we have spent in last five years to develop this.Tarbir Shahapuri: Understood, okay that is really helpful. Great. Thank you so much

I think at the end of the day, we have to think from the perspective of the person who is picking the tab. The card companies. . If their core business is growing at say 25%, there is no way they can support growth of say 65% in the benefits that they give to the card holders. This will eat away from their margins. They might have allotted certain portion of their expenses/revenue for this benefit. There is no doubt on the pull factor of this benefit for customer retention/acquisition. But that doesn’t mean they can keep spending incremental amounts of money every year and let it eat into their margins.

So, i think some sort of equilibrium has to be reached, where the growth rate of spend under lounge access has to come in range of the card companies core business growth. This can come via measures that credit card companies are now taking by way of restricting access to high spend customers etc. This is natural, we should keep hearing about more such measures until that equilibrium is reached. This could keep the stock price under cloud.

This is what i think about the current developments.

Banks have two streams of earning through credit cards.

- Earn the interest on delayed payments (i think this will not be the major stream of income since indian consumers care enough about their credit rating.)

- Earn MDR charges. Around 2% is the MDR charged, out of that even if 0.5% goes to card companies, banks earn around 1.5% (this should be the major income from credit cards for banks).

Now if bank provides a lounge access (paying around ~1k ) to the holder. It only makes sense if the consumer spends at least 1lac (income through MDR 100000*1.5% = 1500), or charge a maintainence.

Cards with AMC will seldom sell in indian market in my opinion if there are lifetime free cards.

Hence lounge access tied to spend based system should be the new norm in my opinion and is not going to go away.

Now considering a middle class family with yearly income of 12-15 lacs. The expenses would be around 5-6 lacs a year. If they try to bring most transactions on cc, then considering transactions worth 4 lac they get around 4 lounge access per year.

Conclusion, not very sure about this part still trying to make up my mind.

4 lounge access is good enough for singles, but not for families. 4 lounge access would not suffice and since the income and expenses is more or less fixed opting for another card for the family member will just divide the expenses/transactions. Hence for this to work out the discretionary spends in the middle class families has to increase.

I don’t see the same growth can continue.

The figures used for income/expenses are to the best of my assumptions

Contrarian views are very much requested.

Disclaimer: Not invested, studying.

Icici sapphiro requires only 5k per quarter spend to get loung access. This is a lifetime free card. I don’t think banks ever broke even or thought in that direction with regards to the expenses towards lounges. And I don’t think they would be applying limits like 1 lakh per lounge access

1 lakh is a very big figure of expenditure to avail lounge services at this point of time where the avg spend numbers on cc (may 2023 data) comes out to be 16-17k.

I beleive that they might be setting up a limit (which is closer to the avg stats) for montly/quarterly spends.

That’s kind of true that the growth ahead will not be the same and looks uncertain

Plus we should remember that most lounge service are available on payment of around 1.5k. So if one is so desirous of the lounge service service he can just pay for it, without needing the services of DFS, why bother keep up with joneses and spend 1L on CC.

People like to get things for free. They will spend their time on Cred for hours to get free points rather than do something productive and buy whatever they need using money.

I believe airport footfall and credit card customers growth are key triggers for DFS stock.

Still it does not have any moat, in the end they are just middleman.

Business model of Card issuers is always offering freebees to acquire new customers…and they must have some budget in mind,How far they can go…only time will tell…if lounges become out of bound,they may ultimately stop

that offering but it may replace with something else…like free coupon for restaurant chain,multiplex, premium salon,spa or diagnostic chain…options are many…main point is how Dream platform will adopt to changing trend…what I feel is card issuers will always focus on core business and Dream will continue their core business of being aggregator…situation is dynamic and I’ll like to pointout that Priority Pass is 30 Yr old now…

Exactly. Icici offers buy get one on bookmyshow. They don’t look for profit, it is a perk. Similar to lounge access. We need to keep that in mind. As well as the other concerns.

Completely agree with @ORION that the card issuers will definetly provide with some free incentives to attract customer to their cards and as we are seeing that the premiumization trend is playing well it all depends upon how dreamfolks is able to cash that and be an aggreagtor for that partcular service (be it salon,golf,spa etc)