9 crore related party transaction for the period from 01/10/2022 to 31/03/2023. And similarly 16480543 cr transaction for the period 01/04/2022 and 30/09/2022.

Highly appreciate experts’ views on this.

Is this normal or consider to be negative aspect?

Air passenger traffic continue to remains strong for Q2. Below is the data taken from Airport authority of India for the 2 months of Q2 which shows more than 20% growth in both domestic and international passengers. ( I have not taken September month data as they seem to have have uploaded the same July month data for September as well. Some reports do indicate that September domestic air passengers no grew by 19% yoy.)

Passenegers (in millions)

2 MONTHS OF Q2FY24

2 MONTHS OF Q2FY23

Growth%

International

11.36

9.27

22.5

Domestic

49.17

39.35

25.0

Total

60.53

48.62

24.5

Q2 results scheduled on 25th. Key thing to watch will be op margin trend which was down in Q1 and likely to remain under pressure.

Discl: currently holding tracking quantity.

I too invested some amount considering this data and the indication by management that OPM was down in Q1 due to “one time costs”

If this proves to be a better quarter and management shows strong guidance, I will double the amount.

Key points:-

Revenue mix = 76:24 (domestic vs international)

Likely moderation in revenue in the short term as card industry aligns to spend based program structure; however this should bode well in the long term since it enables the higher spend based travellers to avail lounge services

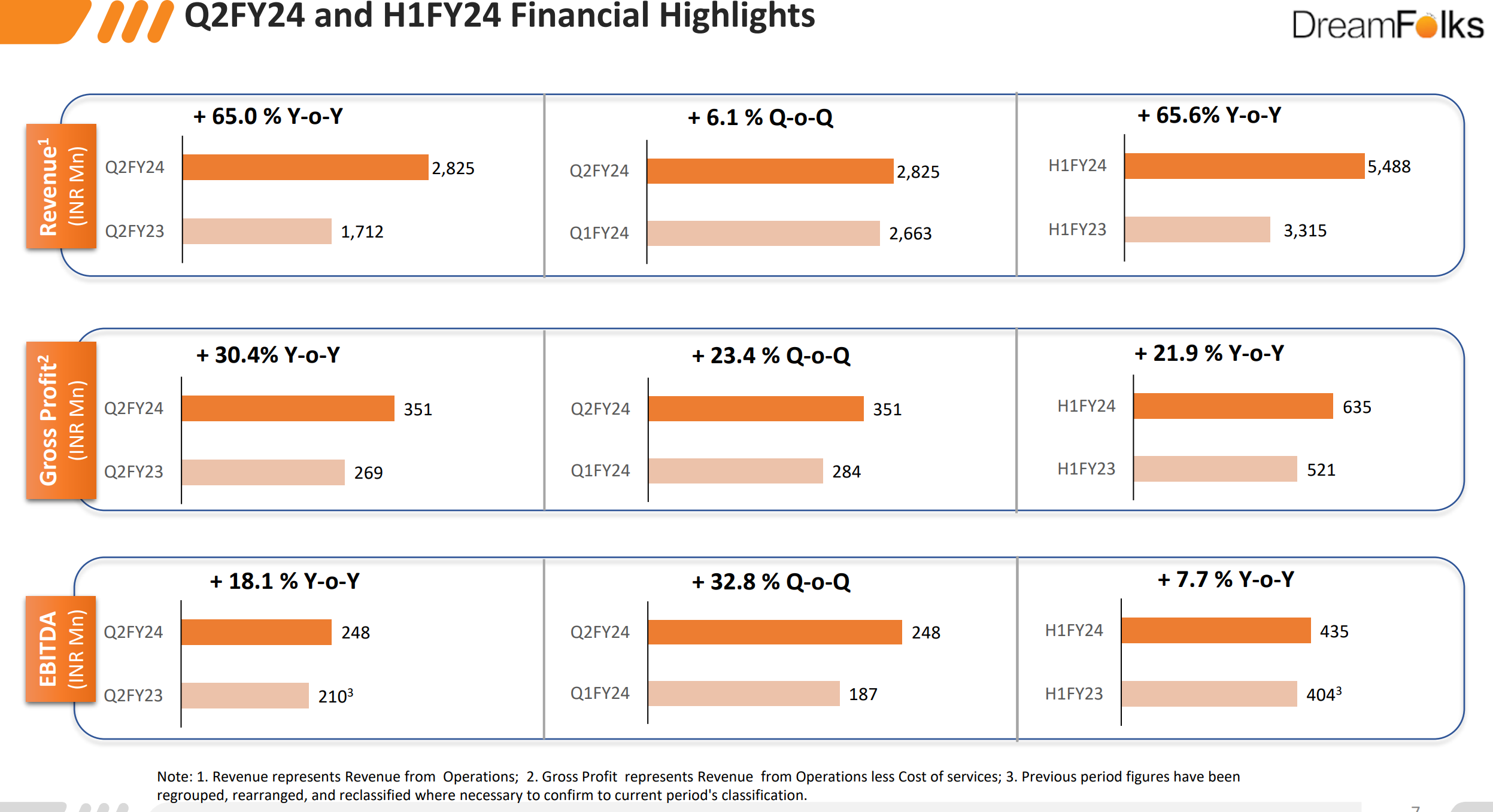

Sales growth = 65% y o y & 6.1% q o q

Gross profit growth = 30.4% y o y & 23.4% q o q

PAT growth = 19.2% y o y & 38.25% q o q

OPM at 9% vs 7% last qtr

New services:-

Tie up for pan-India Salon services and

Offering technology solution in Malaysia for SEA clients - details around the business model to be seen

When a cardholder uses their card to access a lounge, Dreamfolks Services receives a fee from the bank or credit card company.

In addition to credit card partnerships, Dreamfolks Services also offers paid lounge access to individual travelers. However, this is a relatively small part of their business. The vast majority of their revenue comes from credit card partnerships.

As on today, dreamfolks gets a cut (larger share of revenue) from the banks for every cardholder availing the service. More the number of cardholders visiting the lounge better is the revenue for dreamfolks - a volume game.

However, from a business standpoint, it makes sense to ensure that the lounge service is availed by travellers with higher spending capacity rather than what it is today - lounge is overcrowded with majority being low spend travellers (predominantly low spend card holders). It’s more of an occupancy rationalisation measure that augurs well for lounge operators.

At the end of the day, lounge operators need to make money in this ecosystem for them to expand their area and offerings (scale up) else dreamfolks gets impacted too.

In the previous quarter, as per management, “one-off” expense charged by lounge operators, acquisition of a business and wage hikes caused EBITDA margins to fall from 12% to 7%. This quarter the EBITDA margins have improved to 8.7%. Although a positive sign, it is not a complete recovery most likely because wage hikes are irreversible.

Gross margin guidance for the year is between 11% to 13%. In H1, they’ve done 11.5%

Due to increased Accounts receivable, CFO is negative for H1 FY24.

Existing business updates:

Management comments about what exactly is the proprietary technology:

DFS’s platform gives the card providers (banks) the ability to manage card programs. Card providers also drive consumer analytics using this platform. DFS has invested around 5.5 crores over last 4 to 5 years to develop the technology. I still find it hard to comprehend.

New lounges or larger existing lounges (after transformation) are coming up at Hyderabad, Delhi

Railway business has been growing fast but the base is quite low to be called out separately

When asked if card providers can decide to reduce DFS’s margin, the management said they do not think card providers can/will do that. Won’t share details about card providers’ budget to offer lounge services to its customers.

Non-lounge services like “meet and greet” have higher gross margins. Management noted that the segment is small. Once it grows to provide a 20% contribution to revenue, overall gross margins will improve. It will take another 3 to 4 years.

Newer business updates:

Lent their technology of card-based lounge management as a service to a Malaysian lounge operator. Currently, its revenue is too small to be material as it just began per management. However, if it grows, it will prove that their technology has got some teeth after all.

Onboarded a network provider to offer E-sim service to its consumers using DFS’s e-SIM service. I don’t know further details about the profitability, scale, etc. of this initiative.

Onboarded a card provider for providing on-demand golf services to its consumers.

New service: Partnered with salon chain brand. DFS plans to offer salon services to its customers. No further details were provided.

Risks:

Management provided a heads-up about a potential risk due to a change in the way card providers offer services to consumers who avail lounge service. Card providers look to prioritise customers who have higher spends or usage of credit cards. This means fewer customers will get fewer free lounge access than in the current situation. It may directly impact DFS’s revenue in the short term. They didn’t quantify the impact as the situation is still unfolding.

Just listened to the concall - pretty much aligns with my perspective.

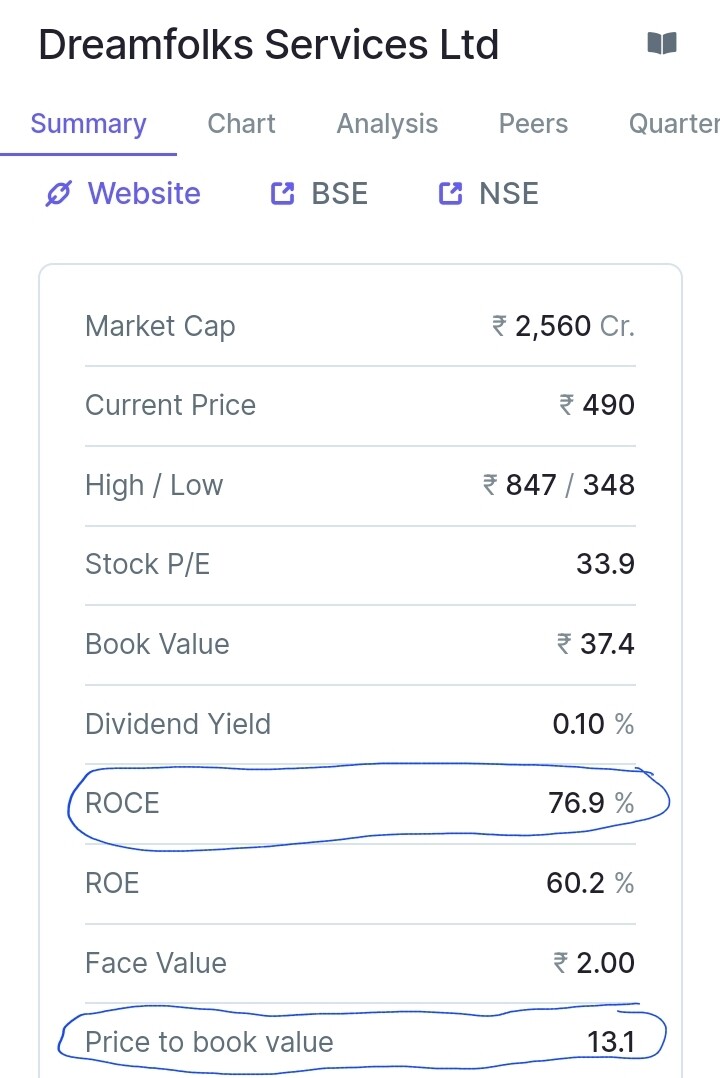

A back of the hand calculation for an investment horizon of 3 years is as under.

Figures as per screener:-

Sales growth h1 fy24 = 65.56% (much less than the previous years)

PAT margin for this qtr = 6.38% (don’t think margin can go below this)

Estimated sales for fy26 = 3507.82

Estimated PAT for fy26 = 223.8

Estimated PAT CAGR = 44.73%

No major equity dilution expected.

Ttm PE at CMP = 34.64 => PEG of less than 1 which shows it is undervalued.

P.S. This is not to be construed as a buy/sell recommendation but a perspective on the valuation.

What I have understood after reading the annual report, is that they are counting growth mostly from a couple of areas

→ Increasing number of airports, more airports are being built or going to be operational in next 5-10 years, more airports more lounges. https://timesproperty.com/news/post/upcoming-airport-projects-in-india-blid4421

→ The other growth area will be the pick up of debit-credit cards in the growing middle class in the country. In India, there are around a 86million credit cards and around 945 million Debit cards, In comparison China has 10 times these numbers, The Company expects that more people using debit/credit cards can/will have a trickle-down impact on the usage of lounges in airports as well.

→ They are also looking to expand in the international lounge market but not sure how big this opportunity could be for the company.

I couldnt attend the call, but from the Q2 numbers it seems that the gross margin is back near to 15% (13.7% to be exact), does it mean that the mgmt has renegotiated the contracts with the banks? Did the management mention any thing on this?

I think it has already been posted in 92 posts which are already there in the thread. Hard for someone to present answers in capsule form for such questions. Kindly be considerate to others and put the effort to go through the thread. Hope you take in the right spirit.

Let me begin with the stakeholders involved and then the business model.

Consumer: People who avail of lounge services by paying through a credit card (or sometimes debit cards).

Lounge operator: Simply put, the company that owns/runs lounges at the airport. They provide services including food and beverage, place to rest and entertainment to customers. The cost is ~Rs 700 for using a domestic lounge.

Card providers: Usually the banks (HDFC, SBI, etc.) offer credit card services to consumers. Few credit cards have perks which include a certain number of free access to the lounge, access to the golf course, etc.

Dreamfolks Services (DFS): In my opinion, this is a software company that claims to have a proprietary platform of lounge access management.

DFS’s Business model:

The consumer wants to enter the lounge. She swipes her credit card.

DFS platforms check eligibility to enter. The eligibility check is based on multiple criteria including:

a. If the card falls under the free lounge access program

b. If the consumer has any remaining lounge visits from the quota

DFS pays the lounge operator Rs 700 and allows the consumer to avail its service

DFS adds a markup of about 12.4% (which was ~15% earlier) and charges the bank ~Rs 786

Bank pays DFS in around 100 days (which explains high receivable days)

Key considerations

Is there “moat”?:

I am inclined to say no.

Is it possible for banks to cut DFS out of the chain and build their own platform? I think certainly possible, but it may not be economical for the banks. If HDFC builds the lounge access platform, it will save 12% on Rs 700, which is Rs 84 per consumer per lounge access. It will not be material for HDFC given its huge size. The same is true for ICICI, SBI, Axis, etc.

Can a smaller bank or a technology player come in to disrupt?

I think certainly possible, we will have to wait and watch.

Can banks and lounge operators squeeze the margins?

Yes, they can and the lounge operators did it last quarter.

Revenue growth:

Banks want more number of users to use credit cards. Hence to entice customers, they offered free lounge access by bearing the cost. Hence, revenue growth is a function of the number of people with eligible credit cards AND the frequency of air travel. Also increasing the number of airports and increasing the size of existing lounges will help. If revenue growth slows or stops due to any reason, valuation may get rerated.

Summary

I think the business is the result of a very smart founder who has extensive experience working at lounge management firms. The founder saw a gap where the banks were not interested in dealing with multiple lounge operators and their technology interface. Banks simply wanted to focus on, well, banking. The lounge operators wanted to focus on F&B, and hospitality rather than creating a technology platform that will interact with multiple banks’ APIs.

We must celebrate that the founder is a lady who made it big in the world of business. Kudos to Ms. Kallat. But I am currently not sure if this can be a long-term bet. I am watching the margins carefully.

I could be completely wrong, please do your own diligence.

Thank you so much Mahesh. Really appreciate. Wonderfully explained. Thats the beauty of this forum.

So i understand fortune of DFS is dependent on lounge traffic which is increasing rapidly and the traffic mainly comprises of credit card holders that get free access. I dont know about current credit card growth, but with several digital wallets / fintech apps (with post paid features) coming in a big way, credit card future looks gloomy - hence banks offering more such priveleges to lure customers (its their customer acquistion / retention cost)

Perhaps these fintech apps may also start giving lounge access to attract customer or make them spend higher (like banks giving for credit cards). I guess DFS should be getting some license fee / SAAS revenue from lounge operators as well

Hypothetically, if banks / apps stop giving such access, lounge traffic may dry down. I believe and trust DFS is trying to de-risk the business model and building other revenue alternatives within airport solutions.

This is good for dreamfolks. People will have more choices to avail lounge services and dreamfolks need not be dependent on credit card holders/banks alone.

As far as SAAS revenue goes, they have struck such a deal in Malaysia.

It’s correct that dreamfolks is trying to diversify its revenue streams.

How much increase in sales is due to A) uptick in passenger throughput in airports, B) how much due to aquisition/entry into new airports, C) equally contributed by a & b.

Ideal scenario is scenario C.

If only A, then the risk is them losing to competition at the time of renewing/re-bidding with existing airports

I’ve heard, small players winning on re-bidding vs large players.