Appended below is summary of conversation with an industry expert on various pharma divisions.

US Generics market

- There aren’t too many patents coming for expiry before 2022/23. And therefore, the key to success would be how the generic companies manage within the existing molecules. (Probe further: need to find which are these molecules)

- In general, generic companies are focusing on smaller size (instead of larger size which have high competition) and lesser number of molecules (than earlier) to retain focus – so that they can garner higher market share in the selected molecules. This focus is helping in lower costs and higher margins. Many companies (especially big pharma) are also moving out of low margin products which is helping in overall pricing and has resulted in lower pricing erosion lately.

- Key factors which help a company excel in this space are:

a. Selection of molecule

b. Marketing knowledge and infrastructure in US

c. Nimble supply chain

d. Regulatory compliance - Companies doing well in this space are

a. Alembic: They have the right talent in US & Europe which gives them the right marketing knowledge – which molecule to launch and when? Abilify, Sartans etc.

b. Dr Reddy’s: New CEO has extensive product knowledge from his Teva experience which is helping them push the right product at the right time. Also, hired external talent in US. They are selling both directly and through partner.

ARVs

- There was some news that the Global funds supported programs like malaria, TB and AIDS are getting effected due to diversion of funds toward Covid, and thus could hurt Indian ARV players like Laurus, Cipla, Ajanta, Aurobindo etc. He clarified this isn’t true and they haven’t seen thus far any of this playing out. Laurus will do well in this space as they have already won a lot of tenders. They can potentially double their formulations turnover in the next 2 years – From c. Rs 100 crs in FY 19 to c. Rs 800 crs in FY 20 to c. Rs 1,600 crs in next 2-3.0 years (once capacity comes in). In addition, new ANDAs and contract manufacturing business also expected to do well for them.

(Probe further: Why Laurus in particular is doing well in this space?)

API space

- China factor has been playing out for last 2 years – due to irregularity in supply due to environment shutdowns and product quality issues like sartans.

- MNCs are (a) getting out of API space and are (b) Nervous about dealing with Chinese cos and - this can be a good space for Indian companies.

- Larger Indian companies are using the API capacity where available, or outsourcing the same to smaller API cos by providing the necessary raw materials, technology etc - thereby ensuring regular supply.

- There is also a trend of Chinese cos putting equity into smaller Indian API companies wherein they supply the intermediaries and source back the APIs back to China. (Probe: which ones?)

- Dependence upon China for KSMs can reduce slightly but overall will continue.

- Similarly, US dependence upon China and India will continue. It is not feasible to shift to manufacturing to US at a large scale. Significant additional costs are involved.

Contract Manufacturing

- This is a very big space for India where Indian companies are increasingly taking market share away from their global counterparts.

- Key differentiating factor here is cost, execution and customer network.

- Syngene, Sai Life (private Hyd based co.), Divis and Laurus seem to be well placed in this space.

All in all, pharma expected to do very well over next 2-3 years with all spaces expected to grow – API, US generics, Contract mfg.

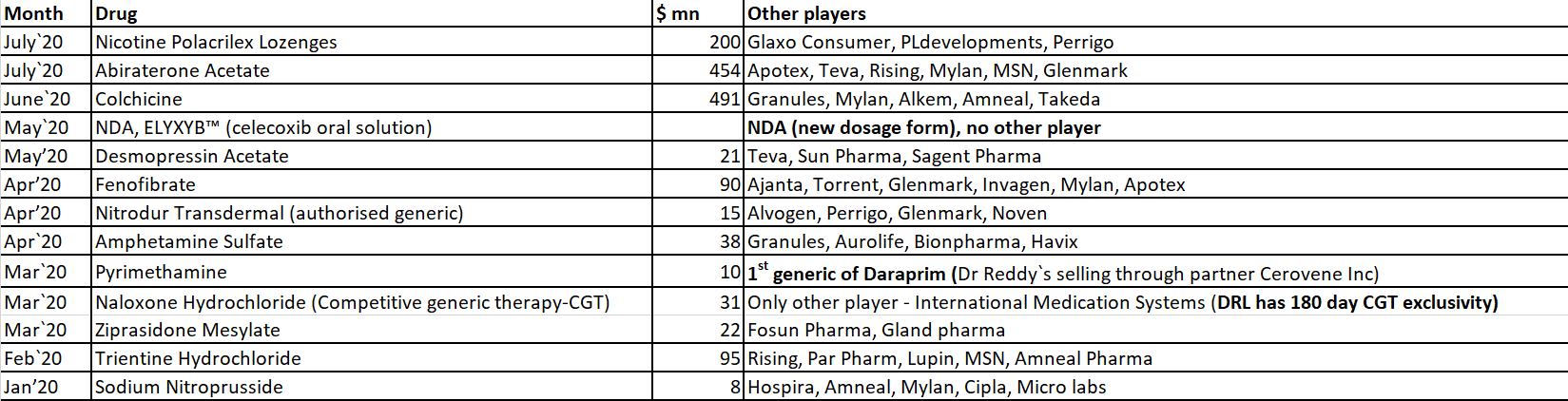

Separately, summary of Dr. Reddy’s launches YTD CY 20. It seems to give a sense of few differentiated launches with limited no. of players: