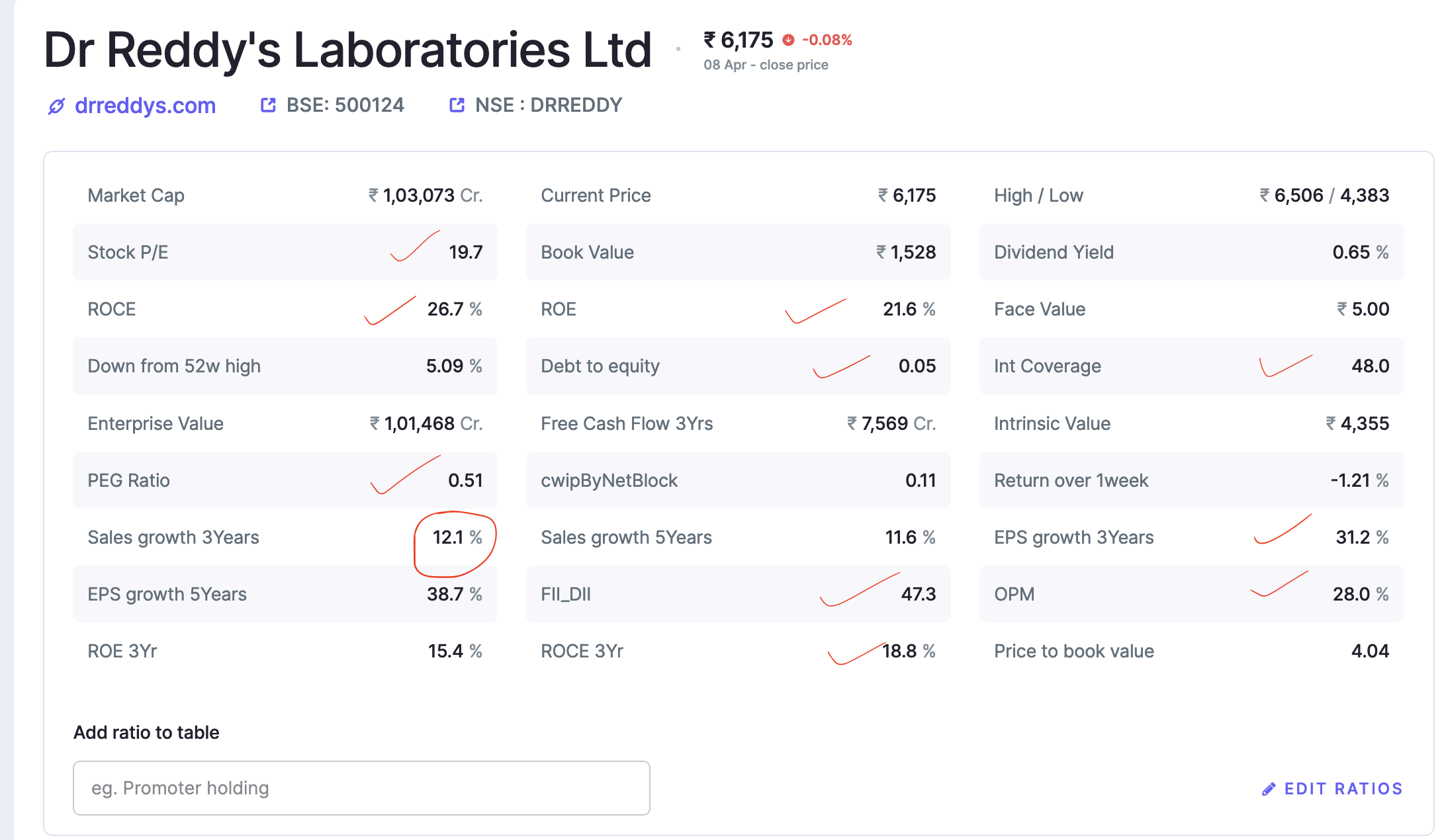

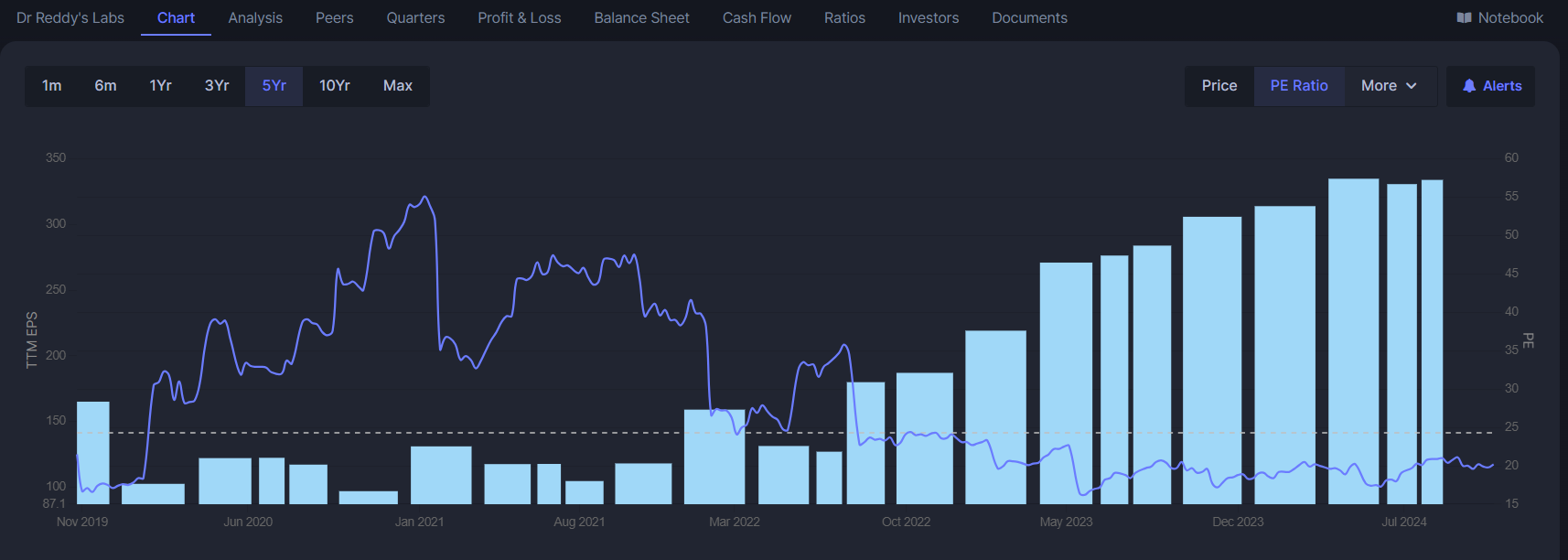

Dr Reddy looks like “Double Engine” stock with above average EPS growth without P/E growth

Fundamentally looks undervalued. Only problem is large Market Cap.

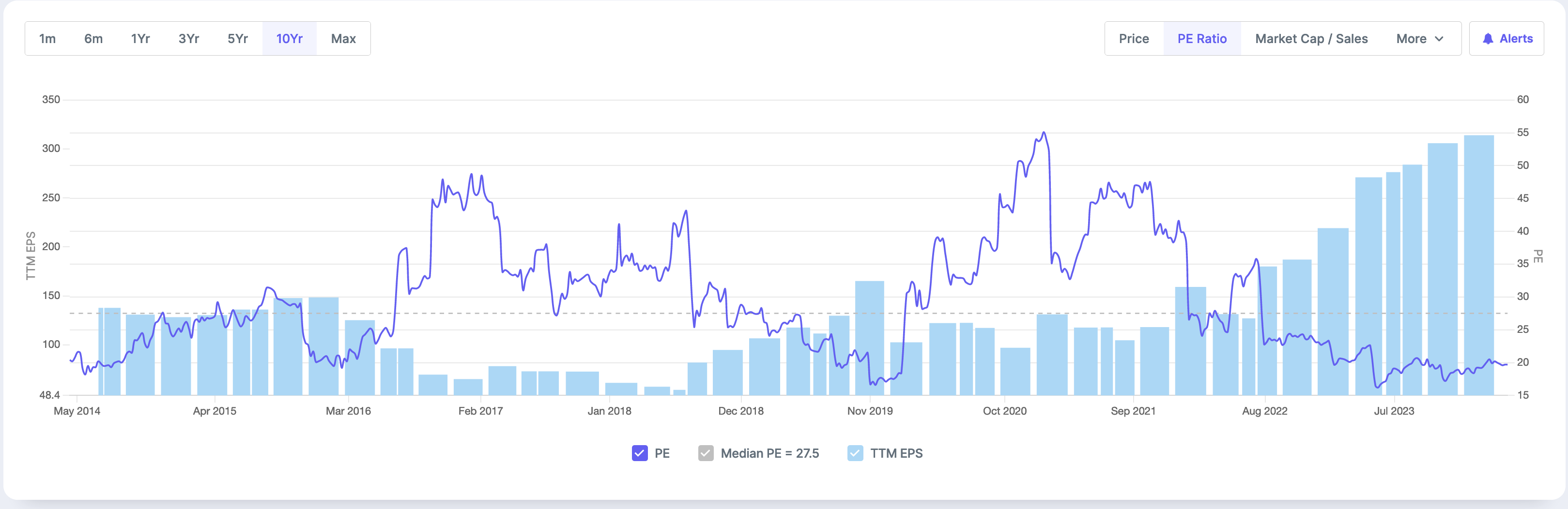

Dr Reddy looks like “Double Engine” stock with above average EPS growth without P/E growth

Fundamentally looks undervalued. Only problem is large Market Cap.

Board of Directors at its meeting scheduled to be held on July 27, 2024, will also consider the proposal

of alteration in share capital of the Company by sub-division/ split of existing equity shares

having face value of Rs. 5/- each, fully paid up, including the American Depository Shares, as

may be determined by the Board, subject to approval of the shareholders of the Company.

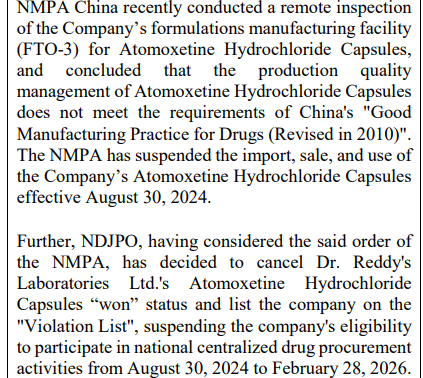

Any idea what impact would this event have on revenue?

Hello Community,

I would like to share some key insights from recent developments at Dr. Reddy’s Laboratories Limited, as it’s been a while since we had a detailed update. Below are highlights from the AR 2024, AGM, Q1 FY25 Results, and the latest credit rating report.

Business Divisions and Products:

DRL provides a wide range of pharmaceutical products and services, including:

The company is organized into three divisions:

Key therapeutic areas include treatments for the central nervous system, gastrointestinal issues, oncology, cardiovascular diseases, and pain management. DRL’s primary markets are the U.S., India, Western Europe, Russia, and CIS5 nations.

Manufacturing and R&D:

API Manufacturing Facilities: DRL operates nine facilities, including six in India, one in Mexico, one in the U.S., and one in the U.K.

Formulation Manufacturing Facilities: The company has 13 plants in India, and one each in the U.S. and China.

Biologics Facility: DRL operates with one biological facility in India.

R&D Centers: It has eight technology development and research centers worldwide, supported by a team of 3,335 R&D scientists.

Product and Regulatory Achievements:

New Product Launches: DRL has launched 181 new products globally, with 20 in North America, 42 in Europe, 106 in emerging markets, and 13 in India.

Drug Master Files (DMFs): It has filed 133 new DMFs globally, including 11 in the U.S. The cumulative global DMFs stand at 1,537, with 251 in the U.S.

Regulatory Filings: DRL has filed 241 dossiers, including Abbreviated New Drug Applications (ANDAs) and New Drug Applications (NDAs). Out of these, 86 filings are pending approval, comprising 81 ANDAs and 5 NDAs. Of these, 50 are Para IV filings, and the company believes 24 hold “First-to-File” status.

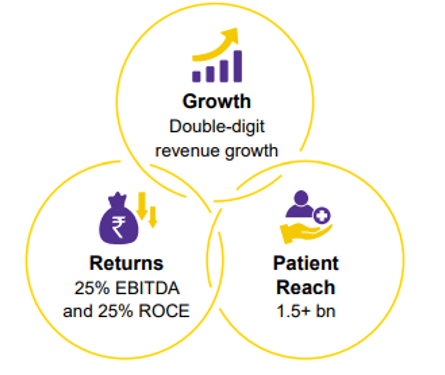

Company Value creations and focus

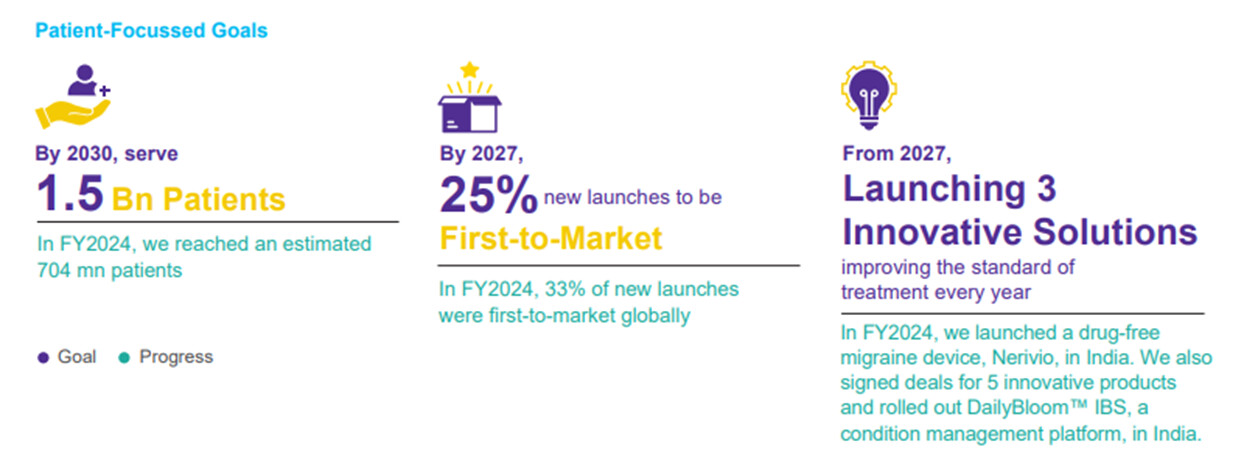

DRL aspires to generate double-digit revenue growth, 25% of EBITDA & ROCE, and to serve 1.5Bn patients in the next 5-6 years.

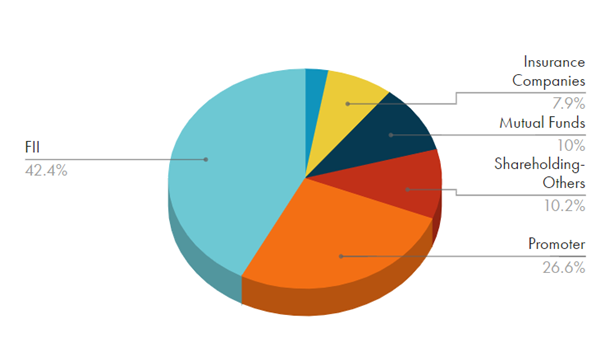

Share Holding Pattern: Public Holding is 10%.

In FY2024, DRL was ranked as the 8th largest generic pharmaceutical company in the U.S. by sales. Globally, it was ranked 11th in India and 15th in Russia as per IQVIA data. The company has grown its market share in several products and improved its ranking in key therapeutic areas across markets.

Aurigene Oncology Limited (AOL)

DRL’s wholly-owned subsidiary, Aurigene Oncology Limited (AOL), is focused on discovering and developing novel, best-in-class therapies for cancer and inflammatory diseases, further expanding DRL’s reach in cutting-edge medical research and innovation.

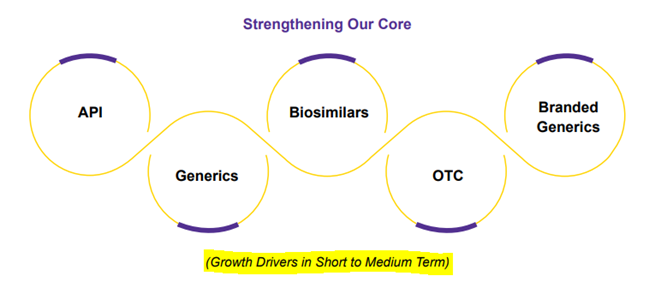

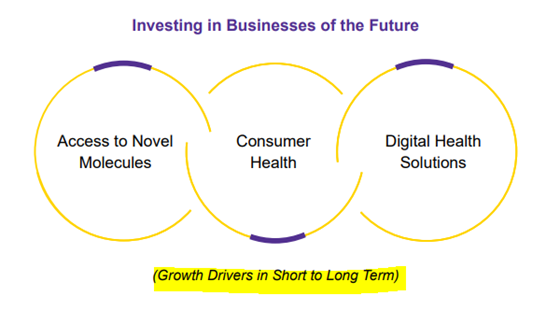

Over the last four decades, DRL has transformed from a company focused on APIs to one that is a leader in formulations, biosimilars, consumer healthcare, and digital therapeutics, positioning itself for continued success in the evolving global pharmaceutical landscape.

I will be sharing additional key highlights in future posts, focusing on the factors driving growth, the identified risks, and the quantitative aspects of the company.

Key Highlights on Growth drivers:

Strategic Collaborations, Partnerships and Joint Ventures

Nestlé JV: Dr. Reddy’s and Nestlé formed a joint venture (JV) to bring nutraceutical products to the Indian market, leveraging Nestlé’s trusted brands and Dr. Reddy’s well-established commercial capabilities. DRL holds 51% of the JV’s share capital, with Nestlé holding the remaining 49%. The company expects to receive royalty payments from the JV as part of its consumer healthcare strategy.

Agreement with Junshi Biosciences: The company signed an agreement with Junshi Biosciences to introduce their novel oncology molecule, Toripalimab, in India and select emerging markets. Recently, the Subject Expert Committee recommended the approval to import and market Toripalimab in India, with a waiver for Phase III clinical trials. The final approvals are expected in the coming months.

Collaboration with the Bill and Melinda Gates Foundation: Dr. Reddy’s has partnered with the Bill and Melinda Gates Foundation (BMGF) to manufacture and supply DMPA-SC, a long-acting, self-administered contraceptive injection. This product will empower women by providing more control over their reproductive health, aligning with the company’s goal to make healthcare more accessible and affordable for vulnerable populations. This initiative also supports the UN Sustainable Development Goals (SDGs) for 2030.

Sanofi Partnership: An exclusive partnership with Sanofi to market and distribute their vaccine brands in India has elevated DRL to the second-largest player in the vaccine segment.

Bayer Collaboration: Dr. Reddy’s partnered with Bayer to distribute Vericiguat, a heart failure management drug, in India. This partnership helps the company expand into Tier-I and Tier-II cities, strengthening its presence in the chronic segment.

Pharmazz Collaboration: Dr. Reddy’s signed an agreement with Pharmazz to market Centhaquine (Lyfaquin®) in India, a promising treatment for hypovolemic shock.

Amgen Partnership: Strengthening its collaboration with Amgen, Dr. Reddy’s will bring romosozumab (Evenity®), an osteoporosis treatment, to India.

MenoLabs Acquisition: Dr. Reddy’s acquired MenoLabs, a women’s dietary supplement brand in the U.S., enhancing its self-care and wellness business.

Nerivio Expansion: Following the successful launch of Nerivio®, a drug-free migraine management device, in India, Dr. Reddy’s extended the product to Europe (Germany) and South Africa and is now available in five countries: India, Germany, Spain, the UK, and South Africa.

China Market Growth: The company is actively expanding its presence in China, consistently submitting 14-15 products annually, with several interesting approvals.

Takeda Partnership: Licensed Takeda’s novel gastrointestinal drug, Vonoprazan, for commercialization in India.

Novartis Pharma: Partnered with Novartis to distribute two of their leading anti-diabetes brands, Galvus® and Galvus Met®, in the Russian retail market.

Ingenus Pharmaceuticals: Obtained exclusive rights to commercialize Cyclophosphamide Injection in the US.

Alvotech Collaboration: DRL is collaborating with Alvotech for the commercialization of their denosumab biosimilar in the US, as well as in Europe and the UK.

Driving Growth Through Innovation and Partnerships

U.S. Product Portfolio Integration:

The U.S. generic prescription product portfolio acquired from Mayne Pharma was successfully integrated into Dr. Reddy’s operations this year.

COYA 302 Partnership:

Dr. Reddy’s entered an exclusive agreement with Coya Therapeutics, a U.S.-based biotech company, for the development and commercialization of COYA 302, an investigational combination biologic for the treatment of Amyotrophic Lateral Sclerosis (ALS).

Biosimilars and Biologics Pipeline:

Dr. Reddy’s is working on a robust pipeline of biosimilar products, including Abatacept and Rituximab. Although their Rituximab biosimilar candidate received a Complete Response Letter (CRL) from the USFDA due to outstanding issues, the company is actively addressing these and expects approval in the next fiscal year.

Innovative Treatments in Development:

Dr. Reddy’s has launched new products in the U.S., including Treprostinil and Regadenoson Injections, as well as multiple other drugs acquired from Mayne Pharma. Additionally, the company is advancing oncology and autoimmune disease treatments.

Expanding Consumer Health and OTC Businesses

Global OTC Expansion:

Dr. Reddy’s is expanding its presence in the OTC wellness space with the relaunch of Premama® in the U.S. and the acquisition of MenoLabs®. Additionally, they entered the UK consumer health market with Histallay®, an anti-hay fever medicine.

Nicotine Replacement and Pain Relief:

Dr. Reddy’s continues to build on its global consumer healthcare portfolio, with a focus on nicotine replacement therapy, pain relief, and women’s health products. Dr. Reddy’s is acquiring a leading brand in Nicotine Replacement Therapy (NRT), Nicotinell®, along with three other brands: Nicabate®, Habitrol®, and Thrive®, covering multiple global markets. These acquisitions provide a strong presence in Europe, Canada, Australia, and Japan, while also offering expansion opportunities in emerging markets. Dr. Reddy’s NRT business won a major tender from Brazilian health authorities, marking significant growth in the region. which has a strong presence in over 30 countries.

Strategic Licensing Agreements:

The company entered into various strategic agreements, including a deal with Tenshi Kaizen to launch Loratadine for the private label OTC business and a collaboration with Mark Cuban Cost Plus Drug Company to provide access to essential medications for Wilson disease patients.

Dr. Reddy’s remains focused on limited competition drugs, with a particular emphasis on injectables and biosimilars, which are expected to drive performance in key markets. The company’s Active Pharmaceutical Ingredients (API) business continues to play a vital role, not only supplying external partners but also supporting its own generic business. This backward integration presents a cost advantage, helping DRL maintain a strong margin profile. The company is further enhancing its backward integration efforts to continue supporting margins.

Dr. Reddy’s is yet to resolve the anti-trust division investigation by the US DoJ concerning price-fixing allegations. Additionally, the company is involved in antitrust lawsuits related to the settlement of patent litigations for Revlimid, which are still being monitored, and the outcomes remain uncertain.

Dr. Reddy’s growth in the US market will continue to be driven by its ability to launch new products and expand its specialty and complex generics portfolio. R&D spending has increased, with 8.2% of sales allocated to research and development in FY24, up from 7.9% the previous year. The increase is primarily due to a higher number of filings and ongoing development efforts in complex products, biosimilars, and small molecules across various markets.

R&D Spending: Approximately 60% of R&D expenditure is allocated to small molecules, with 20% directed to biosimilars and the remaining 20% supporting APIs and other strategic initiatives like in-licensing.

Capex: DRL’s Capex spending focuses 75% on expansion, while the remainder supports maintenance and digital investments.

Dr. Reddy’s remains focused on limited competition drugs, with a particular emphasis on injectables and biosimilars, which are expected to drive performance in key markets. The company’s Active Pharmaceutical Ingredients (API) business continues to play a vital role, not only supplying external partners but also supporting its own generic business. This backward integration presents a cost advantage, helping DRL maintain a strong margin profile. The company is further enhancing its backward integration efforts to continue supporting margins.

DRL’s Aurigene Pharmaceutical Services has inaugurated a state-of-the-art biologics facility in Genome Valley, Hyderabad, dedicated to Contract Development and Manufacturing Organization (CDMO) services. This facility will primarily focus on R&D activities, which aligns with the company’s broader strategy of developing biologics and specialty drugs. Aurigene Oncology Limited achieved promising results in its Phase 1 study for India’s first novel autologous CAR-T cell therapy for multiple myeloma. The Drugs Controller General of India (DCGI) has approved moving to Phase 2 of the trial.

Chirotech Technology Limited, UK: The company dissolved its step-down wholly-owned subsidiary, Chirotech, which had no material impact on the business or financials.

Licensing Agreement with Gilead: DRL signed a voluntary licensing agreement with Gilead Sciences to manufacture and commercialize Lenacapavir in India and other countries.

New Subsidiary in Denmark: Dr. Reddy’s Denmark ApS was incorporated as a wholly-owned subsidiary, marking further international expansion.

Aurigene Oncology Limited (AOL): The company invested ₹2,08,62,912 in Clean Renewable Energy KK 2A Private Limited (CREL), acquiring 26.99% equity in the company.

Rituximab Biosimilar: DRL received a positive opinion from the European Medicines Agency (EMA) for its proposed Rituximab biosimilar. Applications for the biosimilar are also under review by the USFDA, EMA, and MHRA

Bevacizumab (Versavo®): Earlier this year, DRL launched Versavo®, its first biosimilar product in the UK, marking a milestone for the company’s presence in biosimilars.

Product Launches and Pipeline Expansion

In Q1 FY25, DRL made significant progress in expanding its product portfolio:

While the company will rely less on mergers and acquisitions, it will focus more on collaborations, licensing, and acquiring assets or rights to specific assets when needed. DRL is actively building its growth strategy for the years 2026 and beyond, leveraging its strong financial position to make long-term investments in innovation and growth.

This holistic approach is expected to provide DRL with the diversification needed to offset the eventual decline in Revlimid revenues and support the company’s continued growth across geographies and product lines.

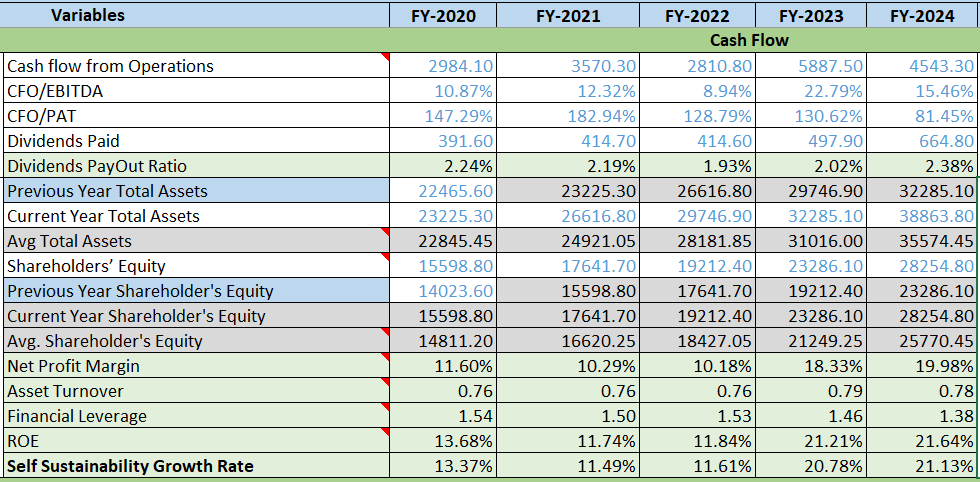

Quantitative analysis of the company:

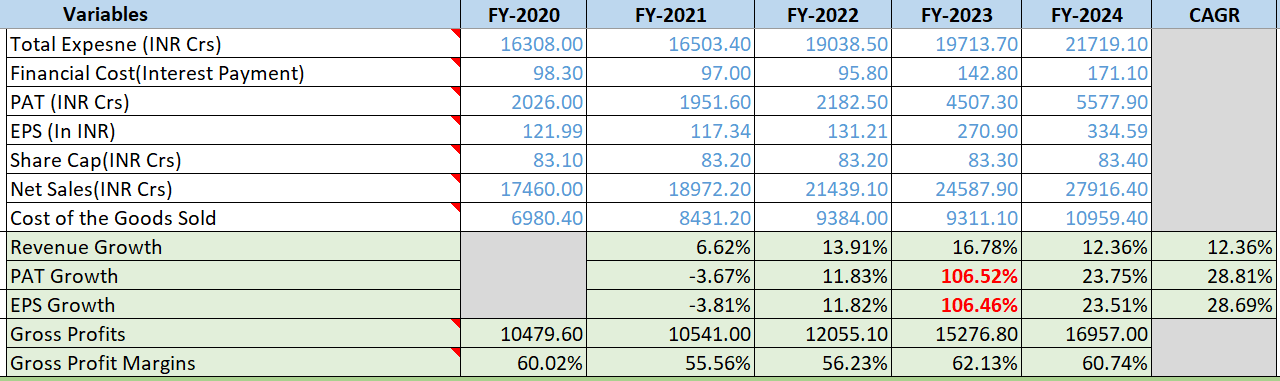

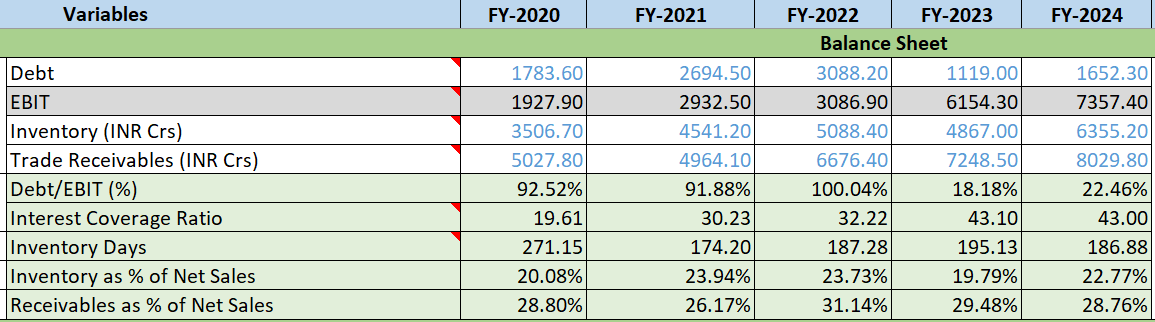

Profit & Loss Statement:

There is a spike in PAT & Earning growth in 2023 due to a combination of an increase in Other income, Foreign exchange gain and a reduction in tax

Other Income contributions were Rs.1055.5cr in 2023 vs Rs.484.4cr in 2022.

Details: During the year ended 31 March 2023, the Company entered into a Settlement Agreement with Indivior Inc., Indivior UK Limited and Aquestive Therapeutics, Inc Pursuant to the agreement, the Company will receive payments totaling U.S.$ 72 by 31 March 2024. The said agreement resolves all claims between the parties relating to the Company’s generic buprenorphine and naloxone sublingual film including Indivior’s and Aquestive’s patent infringement allegations and the Company’s antitrust counterclaims.The Company recognised the present value of the amount receivable at `5,638 (U.S.$ 71.39 discounted to present value) on the date of the settlement as other income.The aforesaid transaction pertain to Company’s Global Generics segment.

Positive and increasing FCF and FCF as % of Sales is greater than 5% makes the business attractive.

DCF Method considering avg 10% growth for 10 years, 3.5% Terminal Growth Rate, and 8% discount rate.

Overall, while Dr. Reddy’s Laboratories faces some regulatory challenges, the company remains proactive in expanding its global presence, especially in consumer healthcare and biosimilars. Its diversified portfolio and strategic collaborations indicate a long-term vision for sustained growth. Currently, the stock appears to be fairly valued, if not slightly undervalued. If management delivers on their plans, the revenue from these collaborations, joint ventures, and partnerships is expected to materialize from 2027 onward. In my opinion, DRL represents a solid mid-to-long-term investment strategy with relatively low downside risk, barring any major regulatory issues.

Disclaimer : I am invested, so I may be biased.

Dr Reddy -

Q2 FY 25 results and concall highlights -

Revenues - 8016 vs 6903 cr, up 17 pc

Gross margins @ 59.6 vs 58.7 pc YoY

EBITDA - 2280 vs 2181 cr ( margins @ 28 vs 31 pc ). EBITDA also hit by one time impairment cost of 92 cr

PAT - 1342 vs 1482 cr ( due deferred tax liability )

Cash on books @ 1890 cr

R&D expenses @ 727 cr - 9 pc of sales ( up 33 pc YoY )

Segmental breakdown of revenues -

North America - 3728 cr, up 17 pc. Launched a total of 7 products in US in Q2

Europe - 577 cr, up 9 pc. Launched 8 new products in EU in Q2

India - 1397 cr, up 18 pc. Growth was led by the in-licensed Vaccine portfolio from Sanofi, new product launches and price hikes. Company is now ranked 10th in IPM

EMs - 1455 cr, up 20 pc. Witnessed strong growth in Russia and RoW territories. Launched a total of 22 products in EM geographies in Q2

APIs and Pharma Services - 840 cr, up 20 pc

EU+North America - account for 53 pc of company’s revenues

Company completed the acquisition of Nicotine Replacement Therapy portfolio ( outside US ) and paid a cash consideration of 4850 cr for the same

Operationalised the JV with Nestle for OTC - nutraceutical products in India and Nepal ( in Aug 24 )

Entered into a non-exclusive in-licensing arrangement with Takeda for commercialisation of Vonoprazan ( a novel GI drug ) in India

Selling, General and Admin expenses were up by 28 pc YoY, mainly led by - one time acquisition costs towards newly acquired NRT portfolio, higher investments in sales and marketing towards scale up of OTC and consumer health businesses

Earlier in Q1 and Q4 LY -

Company acquired World’s no 2 Nicotine Replacement therapy brand portfolio of - Nicotinell, Nicabate, Thrive & Habitual from Haleon PLC ( for sales across the world except US ). Dr Reddy expects the brand to clock an EBITDA margin of 25 pc by FY 26. Deal is expected to be completed by Q3 FY 25

Earlier in Jan 24, company had acquired MenoLabs in US which owns a portfolio of 07 brands for treatment / management of menopause and pre-menopause

Company aims to have a worldwide OTC business with sales of $ 1 billion / yr in next 3-4 yrs. For that they intend to keep acquiring more brands

Two of company’s formulations and One API facility successfully completed their USFDA inspections in H1

Excluding the Sanofi Vaccines portfolio, company’s India business has grown by 9.5 pc in Q2

Company is expecting the India business to continue its high growth trajectory because of the strong new product launch momentum

Have received EMA authorisation for Rituximab. Should be launching the same in European mkts by Feb 25. Hopeful of receiving a USFDA approval for Rituximab in H1 next FY

Most of the company’s R&D is focussed on 3 broad areas - Complex Injectables, Peptides ( including GLP-1s ) and Biosimilars. Have a strong launch pipeline of 20 products lined up for next 2 yrs - which are relatively high value products. This should help them offset the loss of Revlimid sales wef FY 27

Company will have the complete capability to make GLP-1 peptide APIs to formulations in house. They ll only need to buy the Injectable device from others

The results of NRT therapy brands acquisition will start reflecting in company’s results wef Q3. Company believes, they can refresh + reformulate the acquired brands to accelerate their growth rates. Plus they can launch them in additional markets

Company is investing aggressively behind their Russia business. Aim to keep growing in Mid Teens in the Russian mkt for foreseeable future ( primarily by gaining mkt share )

Company has incensed Denosumab ( a biosimilar ) from Alvotech Ltd for launch in US and RoW mkts. Company expects to launch it in US by late FY 26. Dr Reddy should be the 4th or the 5th company to launch it in US

Company has in-licensed Abataceft ( a biosimilar ) from Coya Ltd for US, EU, Canada mkts ( for treatment of ALS - a neuro-degenerative disorder ) . Aim to launch it in US mkts by early FY 27

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Alvotech and Dr. Reddy’s Collaboration to Co-Develop Biosimilar Candidate to Keytruda® (pembrolizumab) which has 2024 sales figure of US$29.5 billion