I am looking at investing in GMR Infra (CMP Rs 14.90). I am looking at a 2 to 3 year investment horizon. Looking at their numbers for FY ending March 2016 and the investor updates, I have done an analysis of positives and negatives as I see it for GMR Infra.

Positives

Capex phase completed and most projects have started generating revenues

Airports business have turned profitable in FY 2015-2016 with PAT at Rs 277 Cr in FY 2015-2016 as against losses of Rs 146 Cr in FY 2014-2015

Airports business have a very high EBITDA margin

GMR Infra’s revenues and EBITDA up in FY 2015-2016 over FY 2014-2015

Income and EBITDA from Highway projects up in FY 2016-2017

Potential for hiving off Airports, Power and Roads business of GMR into separate entities for decluttering the balance sheet and unlocking value

Revenues expected from the monetisation of the DIAL and HIAL real estate projects

GMR cutting down on debt and trying to clean up balance sheet

Receivables from Government agencies and regulatory authorities will add to the revenues

Negatives

Very debt heavy group especially on the projects side with power sector very debt heavy

Interest costs have gone up in FY 2015-2016 over FY 2014-2015

GMR has many issues with regulatory and nodal agencies especially in roads and power projects.

2 out of 3 Gas based power projects stalled on account of non-availability of fuel to generate power and all power projects are operating at very poor PLF’sFinancial Presentation Q4FY16.pdf (1015.6 KB)

I am attaching the consolidated financials for GMR for 2015-2016 alongwith the investor update presentations where GMR has provided an overview of their businesses. I am writing to check views from ValuePickr’s on GMR Infra’s prospects, and the potential for GMR to become a 3 to 5 bagger from the current price over the next 3+ years

Disclosure: I own 100 shares in GMR Infra just for tracking purposes

Points to ponder.

Significant reduction in debt – The Company’s net debt has been reduced from 37000 odd Cr in FY16 to21000 Cr in FY17. Debt reduction via stake sale, disinvestment & debt restructuring agreement through SDR schemes which help bring down leverage further. Net Debt to EBIDTA improved to 4.3 in FY17 from 10.2 in FY16.

Airport business profit has grown substantially during FY 17 – currently the company operates 2 airports – Delhi Airport & Hyderabad Airport. This segment has grown substantially over the last one year. During FY 17, PAT stood at `869 Cr (+423% y/y). This growth was mainly due to monetization of Delhi airport real estate assets & income from in favourable arbitration resolution in the Maldives airport case. The refinancing of their old debt helped bring down interest cost.

Robust EPC order book – The EPC segment is engaged in handling of engineering, procurement and construction solution in the infrastructure sector primarily highways & SEZ’s. The company’s current EPC order book stands at ~ 7,100 Crs. Dedicated freight corridor projects constitute majority of the order book (5,000 Crs). The EBITDA margin for this order book will be in the range of 8%-12%.

GMR Infra has seen a steady performance in the airport segment with Ebitda growth of ~20% y/y. In order to expand its aero/non-aero revenue portfolio, the company has lined up further capex- Delhi airport (~5000 Cr); Hyderabad airport (2400 Cr) and Goa (1900 Cr). Also, the company intends to continue sale of non- core assets including coal mines, road projects and land bank in order to reduce their consolidated debt going ahead. At CMP of19.75, the stock is trading at it’s TTM P/BV of 2.0x

Can this be construed as worth investing? Dig ur own hole. No holdings.

I got interested looking at the large decrease in debt, but a lot of the debt reduction has come from accounting changes where debt is not consolidated on their B/S, although a significant proportion is from the above mentioned activities. I’d advise valuepickrs to read the latest transcript to get more color on this

I had huge investment in GMR infra few years back but had to book loss as the the company went on creating assets and piling on huge debts which eventually brought down the stock price to current level. In-fact most of the infra companies in India have gone through the same story and looking at huge debts now. JP Assoc is one more example.

GMR has to sell off their loss making power business and reduce debt significantly to start generating regular profits.

One silver line is recent SC order which has given them much needed boost to monetise land parcels across Delhi and Hyd airports.

Can you please elaborate, sir? Because I have been tracking the company ad it seems the company is genuinely reducing debt and not just an accounting patch-up. Also, IND AS changes will have affected accounting of all MNC’s if you might have been misled!

Disc. Invested at present 4% of my portfolio.

Debt reduction from 42K cr to 19K crores (Info from AR 17 n concall transcripts) shows the intension of management to make the op profitable. They are very bullish on airport operations and recently bid for Goa Airport venture.

Another interesting aspect is recent court ruling on further commercialisation of vast tract of land parcel avlble around Delhi airport, which at the curent ruling mkt price, accretion to their kitty is around 10K cr.

IMHO, all the above developemnt and GOI initiative to build more airports augur well for GMR Infra to hoist into next orbit.

Disclosure: GMR forms 1% of my PF and my views are likely to be biased.

I have bought this share, about quarter of the quantity I planned to buy. Went through the investor presentation on their website, which brought up a tariff order for Delhi airport. Tariffs have been cut by 90 pc in July 2017, and profits from Delhi airport have turned to losses. Things could get worse here on.

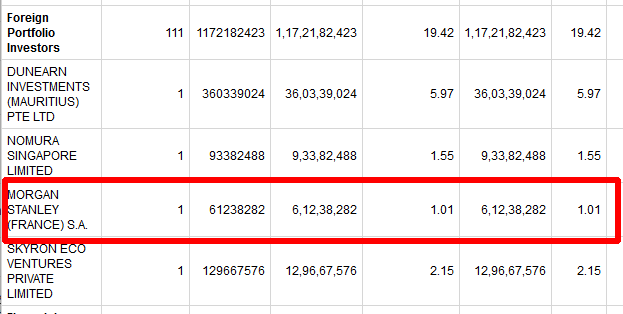

I expected some deeper analysis of this on ValuePickr, but strangely no one has brought it up. Has Morgan Stanley got some knowledge about this issue, that we dont have. Is this likely to repeat in HYD airport? Or Mumbai Airport?

Delhi airport running on losses??? Can you pls share the source… This was one of their very few sources of profits…I was quite bullish on their airport business… Wanted to buy into it…news regarding their intention to list the airport business made me relook my decision, thought of investing in it later…Delhi being one of the busiest airports in the country and needing a lot of expansion in the coming years,if operating on loss will put the whole business in jeopardy

@vaibhav101@pskrishnan

Looks like people have given up on GMR.

2.5 years have passed since this thread started, but stock price is back to 15 rupees.

So trying to get the valued opinions of fellow members on below:

What the current outlook for GMR with all the NCLT cases for power division ? When can one expect the balance sheet cleanup to be complete? Is there any hope in next 1 year or its gone forever?

As per LiveMint article below, GMR Airports is valued at 21,000 crore. GMR Infra total market cap is around 9500 crore as of today. Does this mean other businesses are negatively valued by market or seen as value destructors? Also how will the expected IPO of GMR Airports impact the consolidated debt of GMR Infra which is around 17,000 crore?

@ 3vasup3@vaibhav101 @ ItosLemma I am not tracking GMR Infra now, but in a recent development GMR Airports Limited (GAL) has settled disputes with PE investors in the airports business. GMR Airports is the holding company for GMR’s investments in Delhi, Hyderabad and the new Goa International airports, besides holding a 17% stake in Delhi Duty Free Services. GMR and the PE investors have now reached a settlement. The settlement is Rs 4800 Cr and it values GMR Airports at Rs 21000 Cr. Airports are their most profitable business, and if there is a value unlocking of all subsidaries and the various parts of the Infra business, GMR’s Airports business will fetch a good valuation and premium

A consortium of Tata Group, a unit of Singapore’s sovereign wealth fund GIC and SSG Capital Management will invest ₹8,000 crore ($1.2 billion) to buy a stake in GMR Airports Ltd, which runs India’s biggest airport.

The deal will pump ₹1,000 crore into GMR Airports, a unit of GMR Infrastructure Ltd. and purchase ₹7,000 crore of the airport unit’s equity shares from the parent, according to a statement. GMR operates Delhi International Airport Ltd., Asia’s sixth biggest.

After the purchase, Tata will hold 20% in the airport unit, while GIC will get 15% and SSG will own 10%, the company said in a filing. The deal values GMR Airports at ₹18,000 crore.

GMR Infrastructure, which has net debt of $2.9 billion at the end of December 2018, has been selling assets to pay off liabilities.

French airport operator Groupe ADP would acquire 49% stake in GAL for ₹10,780 crore. Market Capital of GMR as on date is ₹12651. Does it mean that other businesses of GMR such as Roads and Electricity are valued by market as either zero or negative? Electricity business may be a drag but not the road business. Is there some negative only experts can discern in this company?