Negen Capital PMS founder Neil Bahal wrote the following in his newsletters:

Currently, in order to own GMR Airports (which is a lovely business), an investor also has to forcefully own GMR’s Infrastructure business which is honestly, ‘undesirable’ according to me as an investor.

*Think of it like buying a Ferrari which is glued on with a Dump Truck. It does NOT look good when I imagine it in my head.

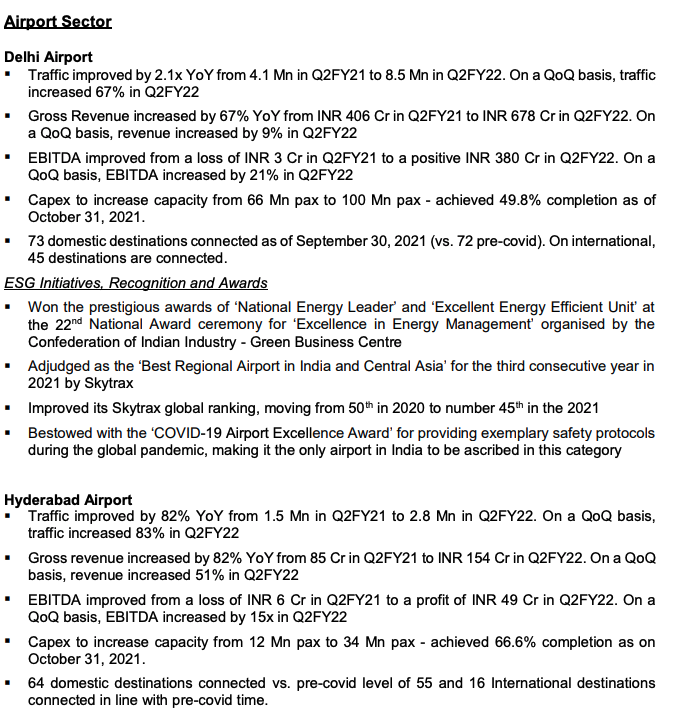

GMR owns 2 marquee Airports in India (Delhi Airport and Hyderabad Airport). It also owns Airports in Goa & Nagpur.

*In total, GMR Airports handle roughly about 25% of all flight traffic out of India. Thats impressive.

The Airport business also has a MNC partner in the form of the French Airport operator called Groupe ADP. They recently acquired 49% stake for big money.

The Airport business has an impressive ROE of 19% which could easily increase with time and a cleaner structure.

They are currently doing ‘significant capex’ all across their airports. They will also get incremental revenue from Nagpur, Goa and Bhogapuram Airports.

Basically, in all likelihood, GMR’s Airport business will grow for many years to come via ‘Structural growth’. It will have nearly no ‘Cyclicality’ to its earnings. Airports just seem to me as a ‘must have’ in any quality long term portfolio.

*This is just my view, and I could be wrong.

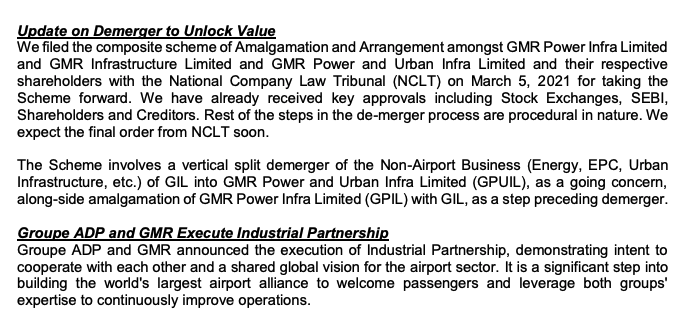

Also, as per me, the Airport business is reasonably valued at the moment and upon a clean demerger, its valuation should just keep rising due to rerating because we all just want the Ferrari without the Truck attached to it, dont we?

*Although, I would love to see lower prices here as its not ‘no brainer’ cheap too.

I cannot imagine any institutional investment committee green lighting the purchase of GMR as a conglomerate today. Ours included.

*But, as a clean demerged, standalone entity, it could probably be a ‘Must Have’.

The update here is that the Sydney Airport in Australia is seeing a fierce takeover battle and you wont believe the ‘price’ which has been agreed to buyout the airport.

50x Ebitda!

*No, I have NOT mixed Rum in my Coffee, I assure you.

*To give context, GMR’s Airport business controls nearly 25% of all passenger traffic in India.

*India being a fast growing economy, will see excellent growth in Airline traffic for decades to come.

*GMR earned 2200cr EBITDA in FY20 (pre covid normal numbers). If we assume, in normal circumstances, the Airport’s consolidated earnings will grow 22% for next 3 years, we should see a 4000cr EBITDA FY24.

*GMR owns 51% of the business and it’s stake will rise to 58% post earnouts soon.

*So, lets say, we give GMR’s fast growing, structural growth Airport business a 25x EBITDA multiple, we get 4000cr * 25 = 100,000 crore. We consider 58% of this and arrive at 58,000 crore valuation (Debt is regulated hence I dont deduct).

Bottom line - Currently, GMR total market cap is 19400 crore. You do the math.

*Also, do not forget, we may/could/maybe get 2-5rs / share for the left over Infra business which I believe could be available free.

The idea as always is to own ‘High Quality compounders but at a good Price’

Risk: I could be wrong, very wrong. This is not buying advice on GMR. This is only educational content. Kindly consult with your financial advisor before acting on this newsletter.

*Negen Capital PMS owns GMR Infra and could have biased views.