1 Like

Dixon Technologies Business Analysis in Inside Out on CNBC TV18

1 Like

Saurabh Gupta, ED/CIO(Dixon Tech) shares future growth potential

1 Like

So management clarifies that this will have no impacts on its payments. However, could this have an impact on Xiaomi’s ability to place large orders in the near future?

2 Likes

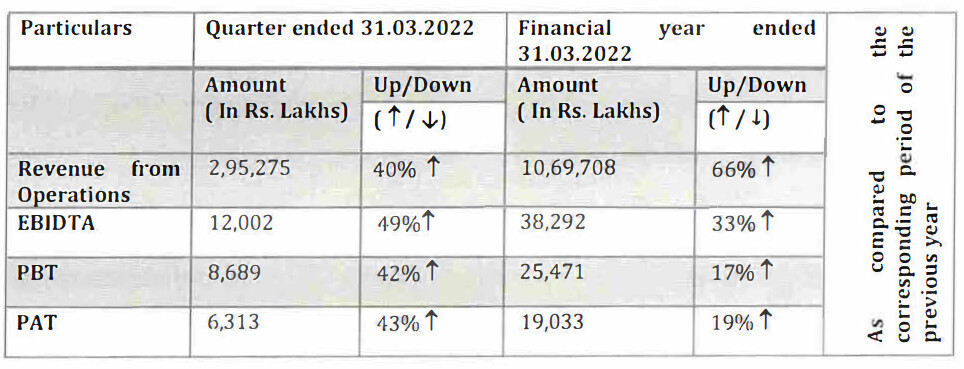

Decent topline growth but concern remains on the PAT margin front which seems to be on a decline the trend, less than 2% for FY 2022, which has dragged the ROCE to 25% from 32% for earlier FY. Because of the impact on margin front profitability is still not justifying the exorbitant valuation.

Unfolding story of Dixon Technologies over the years

Q1FY23 Result- Management Comments

a. Commodity prices softening. This will help in bottom line expansion but revenue will also get softened as they will need to pass the benefits to their customers

b. Management looked cautious on guiding the growth and 17000Cr Revenue looks stretchable

c. 6500-700Cr revenue from mobile division in FY23

d. Management guiding 35-40 percent growth

e. Washing machine segment EBIDTA margins can expand to 9% in coming quarters

f. Tieup with Google for android code on TVs will help in ODM segment for TVs

g. Acquisition of a company which has product line of bluetooth and wireless control for LED segment. This functionality can be extended to other segments like fans also

h. 310-320Cr Capex planned for FY23

i. Export of LEDs started to UAE

5 Likes

Results In.

Market has reacted very negatively to december result, wonder why such bad reaction?

I believe it’s because of a couple of reasons. 1. Rev guidance is weak i.e. revised to 12500 Cr from 14000-15000 Cr. 2. Margins don’t seem to be improving and its guidance is also lower yet again. Even in general, I always thought there is this overhang of Xiaomi being the single biggest client for them. I had exited my position 2 quarters ago for the same reasons i.e. measly and non-improving margins and perpetual weak guidance.

5 Likes

My notes from Concall and recent interviews

a. In Q3FY23 Consumer Electronics, Lighting products divisions got impacted. Revenues from mobile segment were subdued

b. For TVs which fall under Consumer Electronics the main point of revenue degrowth was fall in Opencell prices in international market which is main component for TVs. Although volumes have grown on steady state in TV business

c. For Mobile segment there was delay in addition of new clients and existing client(Motorola) has reduced its ordering due to slowdown in US. Management is guiding for around 8000/- Cr revenue from this segment in FY24

d. In mobile segment two customers will be added and the orders will start flowing from Q2 onwards

e. The guidance was revised downwards each quarter in FY23 and management said as they are B2B company they get the projections from their customers and they give these projections to the investors

f. For FY24 they will get projections from their customers by March 2023

g. Orders in IT hardware segment will also start from FY24

h. OPM is steadily improving as raw material price hike is passed on to customers in ODM segment and value engineering steps they have taken at the plants

My views

a. There may be delays in executions or order wins and may impact few quarters but if we see long term then addition of new clients along with new products should drive the growth

b. If the slowdown in US/Europe continues then it may hit export demand for Mobiles/Lighting segment

c. Capacities are getting built with large projections. As and when new customer wins happen they can grow the business rapidly as the infra will already in place

d. Management highlighted debt reduction and future capacity building can be planned with internal accruals

e. Growth in Mobile segment will be crucial factor to be on track to achieve faster growth

Interviews

Q3 ConCall

Disc: Invested

3 Likes

Now Manu Jain has resigned from Xiaomi who took Xiaomi to the market leading position.

2 Likes

A big bet on mobile manufacturing by Dixon. Even it is able to capture 10% of this then it will move Dixon to next league.

1 Like

Hey everyone,

I have been looking at Dixon Technologies for a while now and at the end of FY22 Mr. Sunil Vachani sold more than 7% of his holding. Does anyone know more about this or was this mentioned in any analyst calls? Also, they used to talk about exports from lighting segments? I have not found any update on this in the company’s reports. Is it too small to talk about?

Please chip in if you have any helpful inputs. Thanks in advance!

Will this be a big issue for Dixon?

2 Likes