Few quick notes:

Dixon clients in mobile manufacturing includes Motorola, Nokia, Samsung, Xiaomi and Jio.

New facility of 3,20,000 square feet being set up in Noida.

In the last five years, revenue from the mobile segment grew at 96 per cent per annum.

Risks: Dependent on China for some key raw materials apart from having Xiaomi as client.

Hello everyone, I am new to VP and excited to be here. I am a beginner in company analysis and would be great to learn from everyone.

About Dixon - I have been tracking this stock for about 3 months. Things seem fine and future looks to be bright as there would probably be an increase in electronic manufacturing in India. However, I am concerned about the following and would love some advice on:

Are the P/E levels of Dixon high enough right now that they don’t represent the performance and suggest more monitoring?

Revenues might be controlled on a few large customers. Additionally, the margins in this business tend to be on a lower side. Could this hamper the growth of the firm?

Large players like Tata could eat their lunch if they wanted to. How big a concern is this?

The stock price used to be ATH two years back and is back to the same levels now. Are there any precedents of successful trajectories from other companies who have seen this pattern?

What investors look at are future returns, in Dixon’s case why the prices fell 40-50% from its high was because of the miss in the guidance provided by Dixon management. As there was delays and order deferring from few customers Dixon could not achieve revenue targets of the 18000 Cr which was highlighted by their management.

Now as few more customers which have been added like Xiaomi, Jio, Samsung in mobile segment there is visibility into the near future and the mobile segment may grew at faster pace and that’s why it started reflecting in its price.

Coming to the future projections if Dixon is not able to meet the investors expectations of high revenue growth from Mobile and Laptop segments which are high growth segments then it’s price will be punished again.

Dixon Technologies has started FY25 on a strong note, with 101% YoY revenue growth to INR 6,588 crores in Q1. The company is well-positioned to capitalize on India’s consumption growth and the “Make in India” initiative. Management expects aggressive growth to continue, driven primarily by the mobile and IT hardware segments.

Strategic Initiatives:

Expanding mobile manufacturing capacity to 55-60 million units annually, including the Ismartu acquisition.

Backward integration in components, especially display modules and mechanical parts.

Entering IT hardware manufacturing with plans for a new facility in Chennai.

Expanding into industrial and automotive electronics.

Developing ODM capabilities in smart TVs and refrigerators.

Trends and Themes:

Shift towards local manufacturing of electronics in India.

Growing demand for smartphones and IT hardware.

Increasing focus on exports, especially in the mobile segment.

Development of the component ecosystem in India.

Industry Tailwinds:

Government support through PLI schemes for electronics manufacturing.

Global companies looking to diversify manufacturing beyond China.

Growing domestic demand for electronics products.

Push for exports from India in electronics sector.

Industry Headwinds:

Slow growth in TV and mobile phone volumes in the Indian market.

Pricing pressures in certain segments like lighting.

Global supply chain disruptions (e.g., Red Sea crisis affecting freight costs).

Analyst Concerns and Management Response:

Concern: Sustainability of growth post PLI scheme expiry.

Response: Management expects government to introduce new schemes focusing on value addition and component manufacturing.

Concern: Margin pressure in mobile manufacturing.

Response: Company focusing on backward integration and component manufacturing to improve margins.

Concern: Competition in contract manufacturing space.

Response: Dixon differentiating through scale, customer relationships, and expanding into new product categories.

Competitive Landscape:

Dixon is positioning itself as a leader in electronics manufacturing in India, competing with other EMS players. The company is differentiating through scale, diverse product portfolio, and backward integration initiatives.

Guidance and Outlook:

No specific guidance was provided, but management indicated expectations for “extremely aggressive” growth. The mobile segment is expected to reach 45-50 million units annually in the next couple of years.

Capital Allocation Strategy:

The company plans to invest INR 500-600 crores in capex for FY25, focusing on capacity expansion and backward integration initiatives.

Opportunities & Risks:

Opportunities:

Expansion into IT hardware manufacturing.

Component ecosystem development.

Export opportunities, especially in mobile phones.

Risks:

Dependence on government policies and incentives.

Intense competition in certain segments.

Global economic uncertainties affecting demand.

Regulatory Environment:

The regulatory environment remains supportive with PLI schemes. Management expects new schemes focusing on component manufacturing to be introduced in the next 9-12 months.

Customer Sentiment:

Strong customer demand reported across segments, especially in mobile phones and IT hardware. The company is expanding relationships with global brands like Motorola, Xiaomi, and Lenovo.

Top 3 Takeaways:

Aggressive growth in mobile manufacturing with expansion plans to reach 55-60 million units capacity.

Strategic focus on backward integration and component ecosystem development to improve margins and create competitive moats.

Entry into IT hardware manufacturing with potential to become a significant growth driver in the coming years.

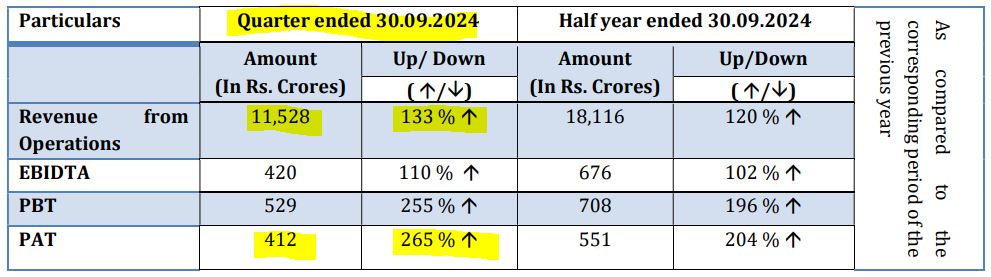

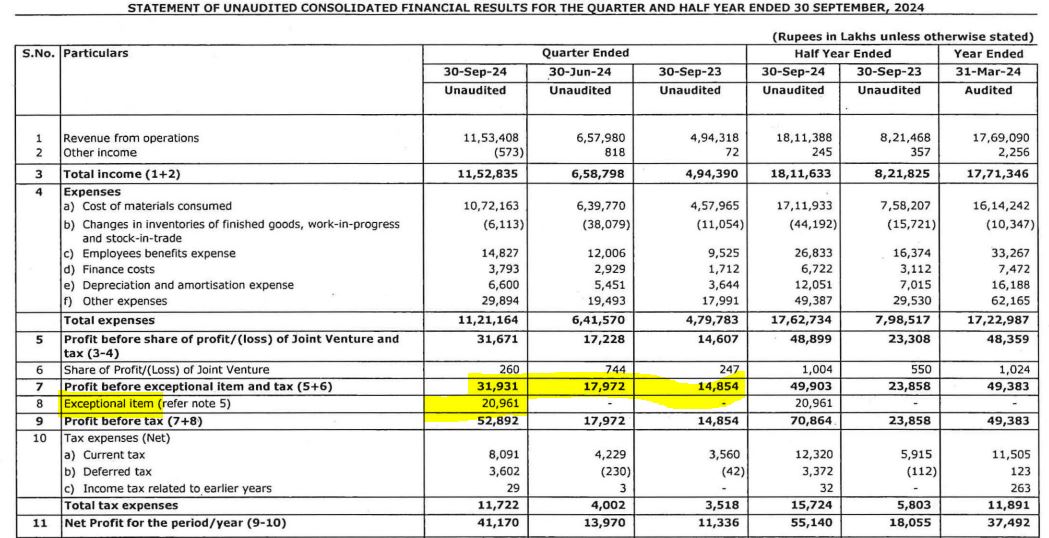

Drilled down little bit into details and realised that there is an exceptional items of 209 Cr. Even after excluding this item, still Profit Before Exceptional items had a healthy jump from 180 Cr. to 319 Cr.

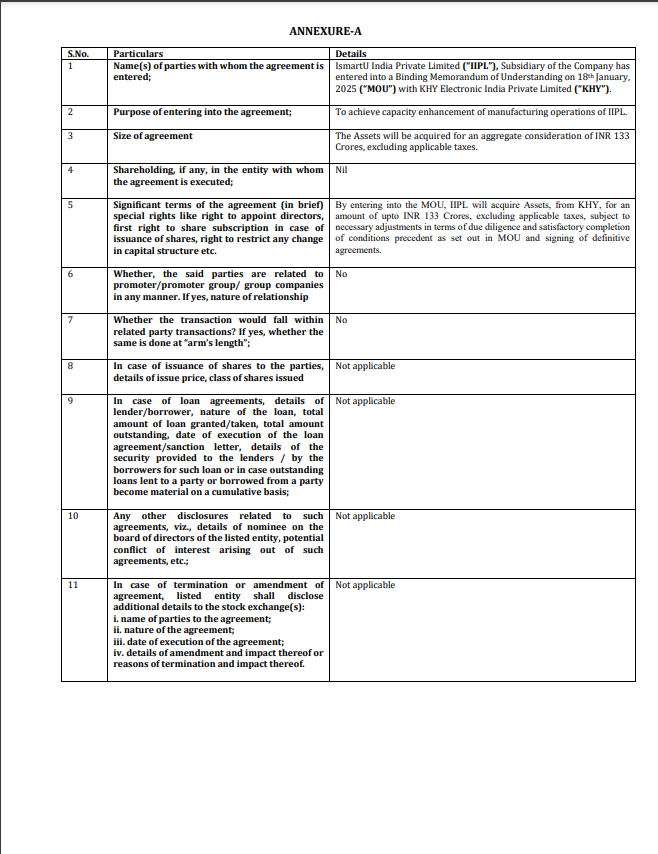

Dixon Technologies’ subsidiary, IsmartU India Private Limited (IIPL), has signed a Binding Memorandum of Understanding (MOU) with KHY Electronic India.

a. Acquisition of land, building, machinery, and other tangible assets to enhance IIPL’s manufacturing capacity.

While they have improved their liquidity and inventory management over 3 years (Current ratio from 1.2 to 1.3 and inventory turnover from 5.5 to 6.4) the quick ratio has been under 1 (0.74). Indicating short term liquidity constraints. There is over dependance on inventory turnover. That means any slowdown in demand resulting in reduced inventory turnover will cause major liquidity problems.

Per recent quarter results, there has been a 32% drop in the consumer electronics business due to subdued consumer demand. I think this is a major risk, including over dependance on global import of components given the current tariff scenario and supply chain disruption risks. Also there is high customer concentration risk. If they lose even a single large customer to competition, they could get into deep liquity crisis.

The company is confident that once it gets into component manufacturing (such as through ECMS), its blended margin should significantly improve.

In relation to mobile phones, backwards integration into components under ECMS is expected to lead to margin expansion and generate a “fairly good blended margin”.

The benefits and gains from initiatives like delving into components under ECMS are expected to be much, much more than the PLI contribution to mobile margins.

They are also exploring opportunities for localising mechanical enclosures for IT hardware under ECMS.

This, driven through a backwards integration strategy like ECMS, should lead to a significant margin expansion at the company level.

Is this report from ICICI generated using some of their tool or some section copied? Well with ICICI direct and the level of firm I am not expecting any error in such reports. However, I have found that their report mentioned Face Value as 10 which is not correct.

Dixon face value is 2 it did go through a stock split