Worth recollecting here Atul Lall’s response to the supply chain issue question in the Q3 call. He made two important points:

On the mobile & TV business, the brands (Nokia, Motorola, Samsung etc) are responsible for managing the supply chain and procurement.

On LED lighting which is mainly ODM business, Dixon proactively built up inventory of chips in Sept/Oct and feels better placed to execute than the competition.

On a more macro level, from what I’ve read the chip issue is real but temporary, and is affecting some industries more than others (e.g. mobiles less than auto as auto are small consumers of chips and do not have the bargaining power of Apple, Samsung etc).

Mutual Funds have reduced their holding by 3.26% (14.18% to 10.92%)

Sundaram Small Cap Fund & SBI Long Term Advantage seems to have moved out

FII/FPIs have consolidated their holding by increasing 0.26% (20.31% to 20.57%)

QIBs have reduced their holding by 0.48% (4.21% to 3.73%)

Small Retailers (share capital<2Lac) : Approx 60K+ new retailers joined the race i.e. jump of 105% in absolute numbers (more than doubled in current quarter)

Above addition resulted in increase of 2.46% in share holding (7.2% to 9.66%)

Big Individuals (share capital>2Lacs) have also strengthened their holding by 0.88% (2.56% to 3.44%)

Overall major shift is retailers have grabbed from Mutual Funds (retail adding 3.34% vs Mutual Funds reducing 3.26%)

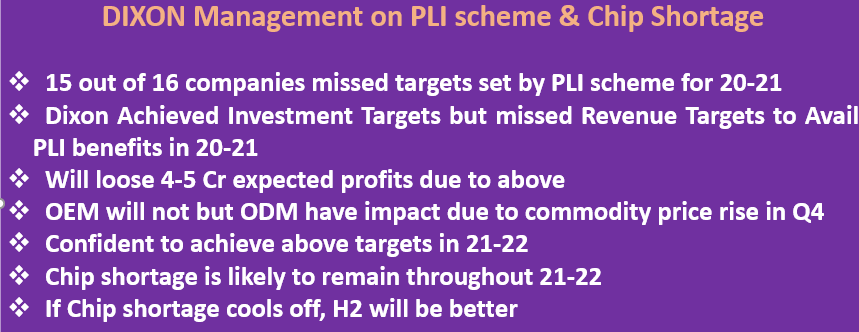

So what would be the impact of this miss on their already razor thin margins + the added complexity of chip shortage which wouldn’t stabilize for another 2 years.

Time 5-630 minute in video mentions - that there shall be loss of 4-5 crs in net profit due to not meeting PLI targets. Industry requested Govt to shift base year of PLI scheme. Dixon Tech is ok with maintaining status quo on scheme.

Good summary of various PLI schemes announced so far. Dixon will participate via 4 of these - Mobiles (approved), IT hardware (in process), Telecom (Bharti JV) and LED Lights (stated previously)

It will be interesting to see how the growth versus valuation story continues to pan out for Dixon.

The results yesterday were good (albeit with compressed margins) and the management has guided for further revenue growth and things look rosy long term.

I though disinvested a long term position basis the following parameters:-

For a 4-5 percent net margin business with high labour costs, every basis point is critical to future growth parameters and PAT calculations. In my understanding, I anticipate future headwinds to the margins aspect of the business - from compressing margins on thier main business (TVs) to high commodity prices impacting raw material cost. Even if this is transferred to the brands partly, would anticipate impact on Dixon.

What price are we prepared to pay for growth - Even if they continue to grow at scorching pace and meet their internal targets of 3x revenue in 3-4 years - the stock would be valued at a PE >40 at the current price after all this growth in 3 years with a significant addressable market tapped.

I anticipate chip shortages to affect their phones business which is amongst the fastest growers

There are other concerns like COVID impact on plants, low net margin, drastically lower PEs of global peers like Foxconn, but those have clear counter points in terms of growth, Short term issues, pent up demand etc.

Finally, it would only be fair to not state possible positives for a business performing very well

A management walking the talk - consistently delivering growth on numbers

Opportunity size still large in domestic markets with electronic manufacturing

Contracts with top new brands being signed regularly

Beneficiary of Make in India and PLI focus

All that said, as an investor, I always don’t question current price, but what is left for me to make in the investment at current price versus what’s my risk if things go wrong?

My analysis here pointed me to a much higher risk than reward, especially with the small cap and midcap index at where it is.

Have taken similar calls on this and a couple of other midcaps I own this week on stocks which worked very well for me over the last few years.

Discl : Was invested, but exited stock this week. This is not a buy/sell recommendation. I have seen several instances in the past where growth stories have continued and confounded all valuation parameters, so this could be the case here too.

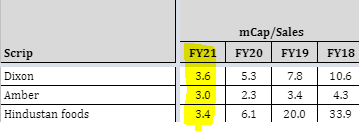

Though valuation is a subjective topic, I think the market values such capital intensive low margins businesses based on their current capacities, WC efficiencies, capex plans & returns(roce) they generate out of these capacities in both present & future. Perhaps p/s would make sense rather than p/e(?), below are the comparisons of 3 key players in similar category:

Personally, I see these high valuations or margins compression(due to lack of chips availability/rise in commodity prices) are short-term issues and don’t see any significant change in the long-term business fundamentals.

Disc.: Biased

@MarketYogi Post selling I do not track the company, but just having an overarching look at the numbers and earnings presentation. I won’t put much emphasis on YOY as that looks rosy but last quarter was a washout. It is even difficult to judge sequentially as the quarter this year also must be impacted.

My primary reasons to exit my investment in the same as I outlined above were 3 fold - margins going down on a very thin base considering cost pressures, can they continue to grow and justify incredible valuations (which have become even higher as happens so often) and the chip shortage issue (more short term but more an issue because of how highly growth is projected).

I think the margins front has come forth in these results - you will see a strong sequential dip in margins and increase in COGs. The cost of materials head in the P&L is now 95 percent this quarter versus 92 percent last quarter. That said - it will have to be evaluated on the earnings call as to what are the reasons for the same - a positive is that Dixon points out in its presentation that this was due to operating leverage issues - so if that gets better post lockdown - it could be a passing concern. Though if it’s coming in terms of RM prices - I would be more worried.

Regarding the valuations and growth expectations, things remain the same so too early to judge, this we will only know in the longer term. One can just put in the best growth expectations and understand if they are willing to pay a forward earnings multiple as per the same.

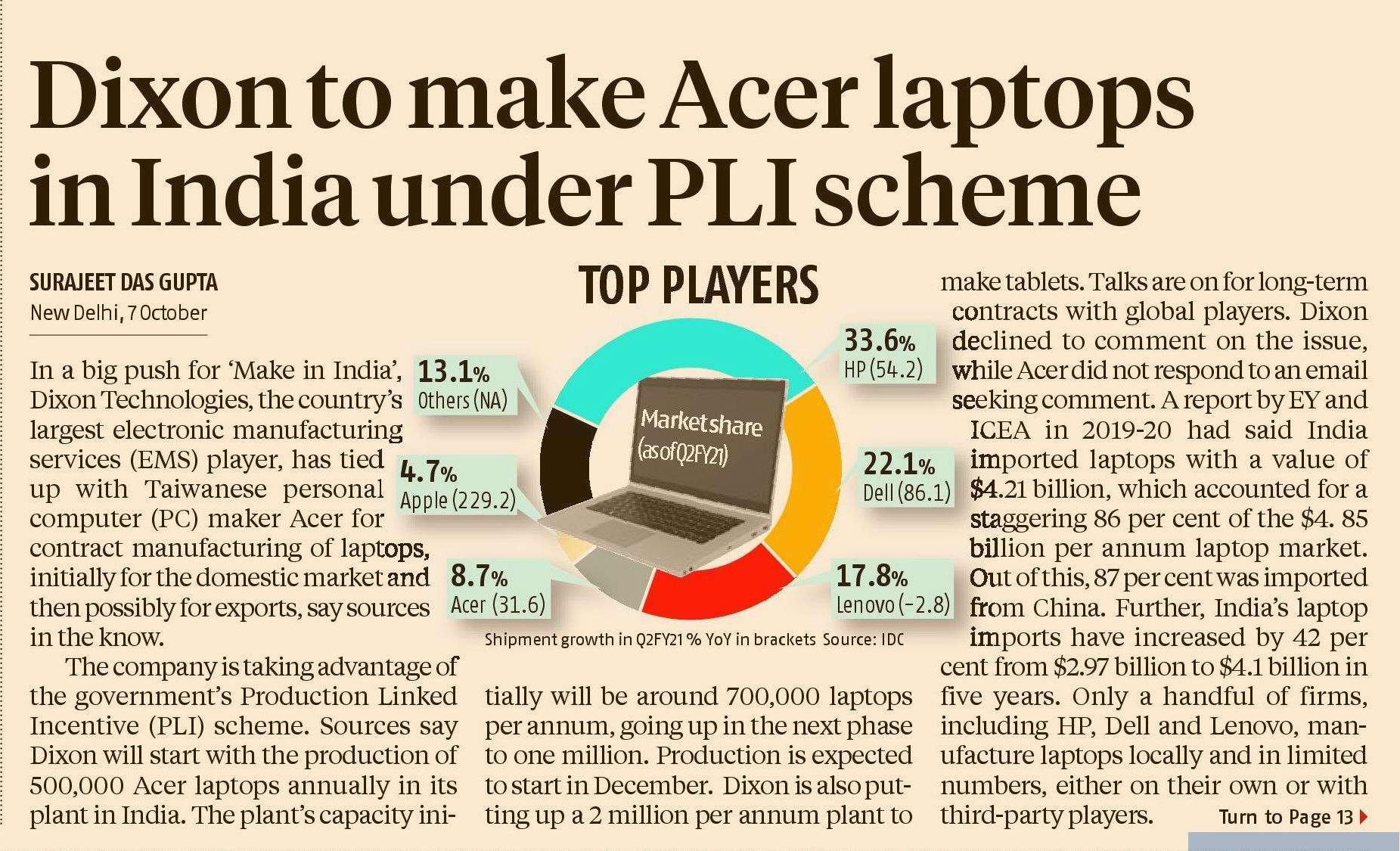

Additionally, thier earnings presentation points out they have semi conductor stock probably, so that maybe partly addresses some concerns on that point, but will again have to be judged on the earnings call.

For me - the decision to exit was taken basis a long term view - it was a 10 bagger so a very hard exit - but made sense in my portfolio strategy as well as my towards my view in moving towards larger companies considering current mid/small cap run ups. Like I mentioned, valuations can continue to confound all of us, and that continues here.

Discl : Not invested, limited tracking information, not buy/sell recommendation or advise

I have couple of questions:

Have been tracking this company for several quarters, am not seeing incremental value add.

In one of the posts above, there was a mention about plastic molding, did not see percentage of value add with this activity

I guess I am missing something in valuing this company, guidance is appreciated

I second your opinion. But at <10% gross margins, it is not possible to add material value from any process innovations. I have made peace with the fact that this is a pure scale play, where they have to bulldoze their way to top. Only ray of hope is if they are able to increase their ODM share. This for me is a key tracker for near to medium term. I hope they increase ODM share in at least their older segments in which they have already established scale.

This is a snippet from Q2FY22 results. The comany auditor has mentioned two subsidiaries which it did not provide the audit for. These two subsidiaries sombined have an asset base of 783 crores (~25% of consol balance sheet size of Dixon). Given the size of the subsidiaries, I wonder why were these two kept out of ambit of the chief auditor (the result being the shareholders have no idea of the workings going inside there)

If one is interested in EMS industry and the upcoming Bharat FIH IPO then the F&S report on EMS industry is a good read. Dixon is at number 3 right now in terms of revenue share.