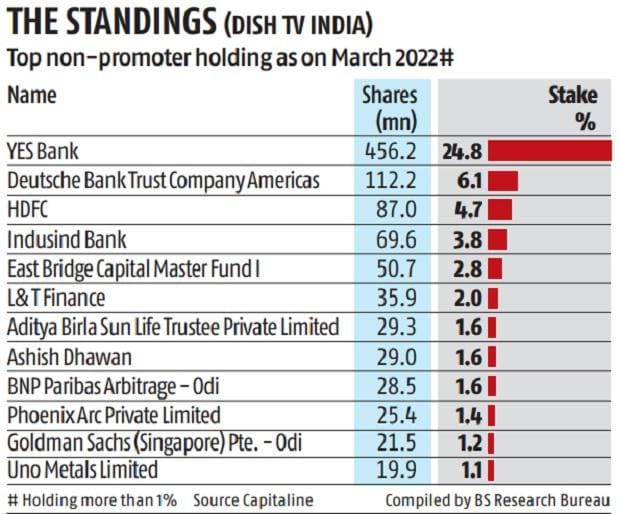

Mr Jawahar goel is not going to be reappointed.Out come of board meeting below.Now this could be the required catalyst to unlock value.

4 Likes

Yes, finally after a year wait. This should be trading at atleast 10x EV/EBITDA within a year or two IMO

2 Likes

Surprisingly the promoters are selling. Idk why they are selling even if they lose the battle they should be getting a better exit than current price.

Annual report released

Financial performance:

"During the fiscal, subscription revenues were lower as compared to the last fiscal primarily due to volatile viewing habits,emergence of the second and third wave of the pandemic in the country, high inflation and conservative spending. Theresultant average revenues per user (ARPU) declined as well. Operating revenues for the year were 28,025 million. EBITDA for the year stood at ₹16,442 million while EBITDA margin was 58.7 per cent. Financial expenses continued todecline due to repayment of borrowings. PBT before exceptional items grew from ₹823 million to ₹2,727 million in FY2021-22. The Company reported exceptional losses of ₹26,539 million leading to a net loss for the full year of ₹18,672 million. The Company stayed focused on deleveraging its balance sheet for the fourth year in a row and paid off ₹4,343 million during the year thus reducing its overall debt to ₹3,756 million at the end of fiscal 2022 as compared to 8,099 million at the close of fiscal 2021. "

EBITDA of 1644 crores.If we take 10x valuation it is 16440 crores.Maybe a 5 bagger.

Disclosure:Invested.

2 Likes

This is a dying industry ,with EBITDA falling every quarter due to subscriber base falling ,If we take last quarter as benchmark with no fall then the EBITDA would be somewhere around 12 to 1300 cr for this year.

1 Like

I dont agree with you on the dying industry part. Post COVID TV has come back big time. People like us watch Netflix and other OTT content but the DTH business is very strong in Rural, Semi Urban part of India. Look at Airtel they are still investing in the DTH business. If the industry was dying they would not look at it.

They charge some 150-200 Rupees per month. DTH is the cheapest source of all plus Hotstar, Netflix and other OTT apps are not making any serious money in India.

I think they should get back to 2000 crores EBITDA in few years plus a 6-8% growth in topline every year.

You will be amazed if you go to the rural part of India and count the number of Dish TV dish on the roof of every building.

2 Likes

1644 crore is a low number. They should get back to 2000 crores easily once the management change happens. The current promoters are not that clean. I don’t think we should take the current EBITDA numbers at face value. The actual number is very high from 1644 crores.

Plus the promoters have sold some stake in Q1FY23. I guess they are need of some money otherwise even they know that even if they lose the battle they should get a better exit.

1 Like

It all depends on the OTT platforms.I think Hotstar will raise subscription charges soon,since it is making 600 crore loss right now as compared to last year loss 361 crore.Also cable operators still constitute a portion of the market.People will move upstream to DTH providers.Also the rural populace may not transition to OTT anytime soon.

Either way Dishtv is undervalued.It has the same market share as Airtel.

1 Like

Where did you get the info that promoters are selling? Any link you can share?

People like us who have switched to Ott platforms ,will most probably never go back to Dth,the people who had low incomes have switched to illegal aternatives (my driver ,maid eyeryone has switched to it and i hardly doubt they will go back either.)

What you have said is true dish tv still being popular in rural areas,Infact on my recent train journey to varanasi i mainly saw disht tv’s but for how long?Airtel and reliance are investing in the business because they sell a bundled package of internet ,dth and landline and same goes for reliance.All these are listed companies aiming for growth when there is no market left in tier 1 cities they will look at tier 2 cities for the growth QoQ that there investors demand .

Your recent post about tata play being listed highlights this ,although tata is a big player but the big investor want the ipo because they want to get out and sell stake.

In any case we cannot predict the futures only thing true even now at 3300 market cap this stock is extremely cheap and whatever could go wrong had gone wrong in the stock and with recent rally market has realized this.

Disc :invested

see the promoter exit is the value unlock here. The company is not properly managed. Even with such poorly managed company you could see soo many Dish DTH on your way to Varanasi.

and privacy was always there in India that did not stop PVR and Inox to grow.

You dont want to change you DTH again and again. You are already getting it at 150-200 rs, which is very cheap. I think a lot of people are worried because of the FY22 number.

I agree with you on the competition part and the competition is there in every sector in India. Look at the home loan segment it is extremely competitive. I think if it was to grow at 8% YoY it will now grow at 4-5%. I do not see a de growth here.

1 Like

Thanks for sharing. I thought you were saying promoters were selling in the last few days/weeks.

Dish TV is good candidate for being acquired. Even goels will want to get best price for dish tv. as they are on path of reconciliation. apart from stepping down as md they have agreed to appoint yes bank nominees on the board. this is heading in right direction for all shareholders… and also employees.

3 Likes

2 Likes

Hi Guys,

I have been tracking YES BANK very closely so how could I miss out here.

My view is this is a sure shot sell candidate. There is no way yes bank is going to run this business. They themself have a lot of problem to cater. I feel they will sell this company after 8 to 12 months from today. What happened with ZEE is going to happen here as well. As of today people are extremely excited and they feel that tomorrow it is going to be bought that is the reason there is jump in share price. It was extremely overvalued at 20 and I offloaded 50% of my position there. Buying it back close to 15 will be a good strategy and there is high chances that you might end up making 2x or 3X kind of return from 15.

Please note that they are loosing market share and not in a good situation. The only reason they are surviving till now is that they are generating positive cash flow. If they are not acquired then there is high chance that you might loose lot of money here. Be cautious and IMO you allocation here should not be more than 5%

at 20 Rs it is extremely overvalued and from 15 Rs it looks like a 3 bagger to you? So, how come it is extremely overvalued at 20 if you have a target price of 45 rs in your mind.

6 Likes

Interesting, no one is talking about this recent news. 3 years Lock-in period is ending by 13th Mar 2023. There will be a huge supply of stocks from that day which can tank the share price.

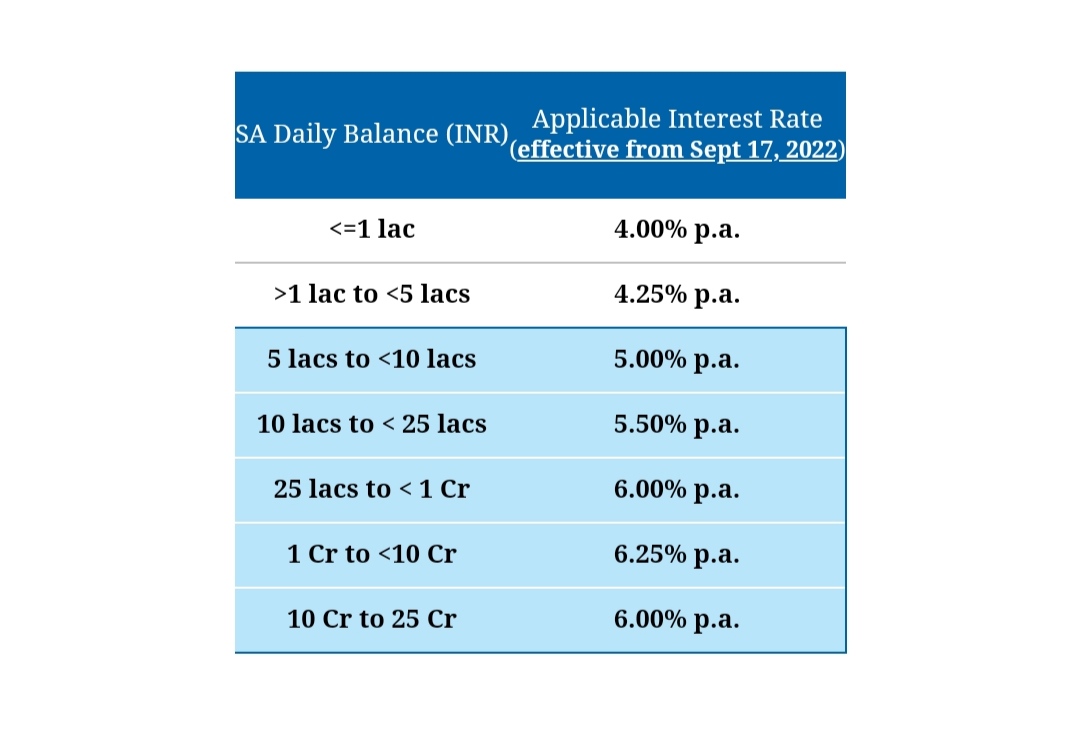

Recently received a mail communication and call from my yesbank manager saying the savings interest rate is getting hiked and the interest is applicable to the entire sum and not on slabs basis. As a savings account holder this is good news but why should the bank give this attractive scheme? Are they in trouble?

Disc:

- Was shareholder and exited at the rock bottom

- Savings account holder, full life savings got held up for more than a month, caused a big distress. Still holding the savings account but reduced the amount considerably.