Long time no update. Did you put more money in DHP?

Thank you for asking, Vishal. No, I didn’t put more money in DHP. Well, actually I tried to - but there’s some compliance rules overhaul going on at my work. So if you want to know whether I am willing invest in DHP India, the answer is yes (Maybe at a ~20% lower price - which when I tried to buy it recently).

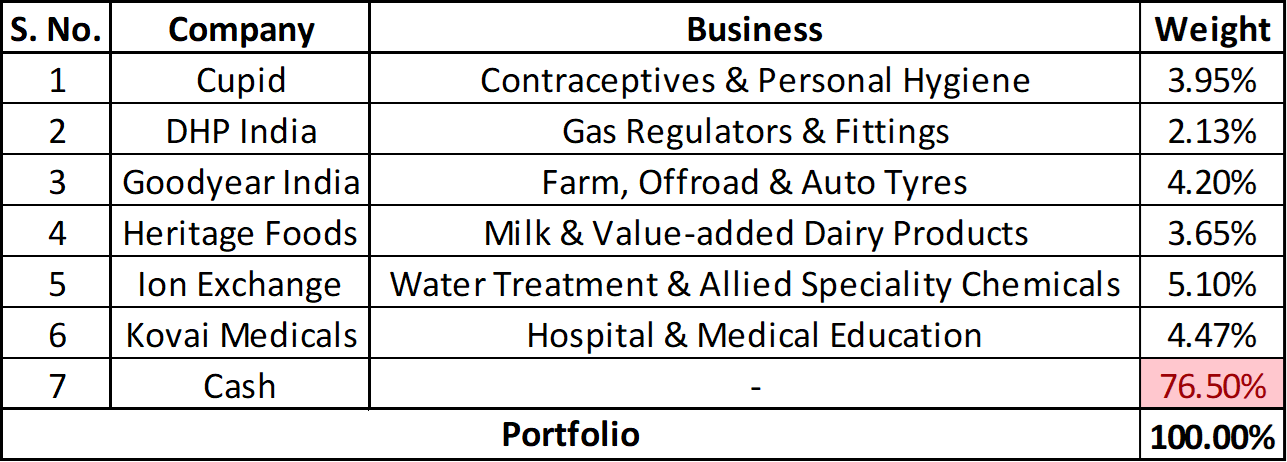

Portfolio Update

The elephant in the room is Cash. Yes, I have not invested anything in the last year. I sold a couple (Cera and IndusInd). Hence, the cash pile up.

Heritage Foods: Due to unexpected weather and production/supply issues, things aren’t going well for the last couple of years. My major tracking point still remains the VADP ramp up and turning it profitable. I’m disappointed at the progress made so far in turning it profitable, but there are new initiatives like the App and online sales that came as a nice surprise. Overall, I would want better visibility in VADP to increase my allocation. Until then though, I am happy to hold it.

Cupid, DHP, Goodyear India: I don’t think there is any visibility issue or such. But Valuations are not favorable in my opinion. I would definitely add at lower levels than these.

Kovai Medicals: I am a little cautious because of COVID related loss of Revenues. Medical Education Revenues also dropped significantly, which I need to explore further. But again, I absolutely trust in the long term story here.

Ion Exchange: Mixed bag of both low visibility and high valuations. I still believe in the long term opportunity in this industry. So, I have no qualms holding it.

Watchlist: Cera Sanitaryware, Huhtamakhi, Inox Leisure, La Opala, NESCO, Navneet Education, Orient Refractories, Precision Wires, Rajratan Global, Swaraj Engines, VIP Industries and VST Industries.

Work is demanding lately, so I have been falling behind on researching my watchlist ideas. I potentially lost a good opportunity to invest in Rajratan Global simply because I was too tied up to do any meaningful research on it.

Precision Wires and Huhthamaki are recent additions to the watchlist (Huhthamaki, I have done some research on a couple of years ago).

Most interested in VIP Industries, just to see how they handle this pandemic and the very likely dull demand even a year or so after the pandemic (Past pandemics are a good reference points). I would love any price below Rs. 280. Rs. 230-250 would be perfect.

12 Likes

76% cash is a lot. And looks like Capex spending is starting along with other sort of consumptions like Auto.

How is the PF performing w.r.t indices currently…I am invested in Ion Exchange…how is the potential of other companies and their returns

I started investing seriously only about a year before starting this thread. So overall, some 3 years and change. I don’t think calculating portfolio returns at this point has any meaning and I haven’t done that.

Regarding returns, my expectations for any Equity investment is at least 15% over the long term, even if something goes wrong with my thesis or the company.

5 Likes

@my 2 cents for kovai medicals recently they collected almost 12 crores(sorry for miscalculating amount) fees in first year MBBS,go on kmch hospital than go for medical college, than go for information under msr clause,there are 150 seat try to giving you some exact amount,

97 seat 385000rs =37345000,

40seats1250000=50000000,

13seats*2350000=30550000,

in the long run there much more growthy opportunities like MD, DNB, hope it plays well,

dislcaimer: invested , not sebi register, no buy and sell recommendation

2 Likes

Can you give source. It might be for 1st year and second year. Last year, it was 17 crores so this year should be 34 crores. It means they have increased fees. There are lot of possibilities in Medical college. Full potential of revenues will take time but it is having certainty. I don’t know exactly but as per some Broker research reports the capex in corporate hospitals is going slow. Capacity is already surplus. So we can expect some improvement in utilization.

Disclosure - Invested with intention to give long rope.

2 Likes

Hi bhai

I Have only one question why there is not a single market leader stock like Asian paints ,HUL etc .

1 Like

What’s the definition of a “Market Leader”?

Cupid is one of the only two companies in the Global B2G Female Condoms industry.

Goodyear India has 30-35% Market Share in Original Farm Tyres in India.

4 Likes

Hey Dinesh,

Can you please tell that 1000 cr revenue projection by KMCH is for incremental capex or in totality. Asking you because you seem to be doing some relevant research on the company.

Thanks!!

It seemed like the Management said that projection is for the Medical College and the 350 additional beds (So, incremental Capex).

But even I wasn’t very clear about it. I wrote a mail to the CS on it and didn’t received a proper response.

1 Like

Ok, even I am under the impression that it is for incremental capex only.

If our understand is clear then this stock can do wonders…

What is ur assessment of mgt on parameters like execution, guidance, capital allocation, investor communication etc…

Thanks!!

In KMCH , one key concern is potential to scale up. Founder promoter is 80 years old now, son is not an intelligent fanatic.

Seems that this would remain one Hospital, one College for a very long time.

Disc. : Invested

@dineshssairam your valuation blog is really helpful. I noticed you do a monte carlo simulation to sample variables. Do you think this is actually useful or overkill ?

For eg monte carlo assumes the underlying distributions to be independent and noise in the system to be gaussian. Are these assumptions justified? Many variables in investing are interdependent and also path dependent as opposed to being a random walk which would breakdown the usefulness of monte carlo.

Additionally even if you sample many trajectories, it would need to be averaged and the distribution of trajectories would anyway end up being a bell curve. So then, do the benefits of monte carlo far outweigh doing a simple scenario based testing ?

6 Likes

You’re right and the simple answer is that it’s too much to Model.

Say, you think some % increase in Margins will lead to some % decrease in Sales. How will you go about Modelling it, really? Even if you could model it for say Sales and Margins, how would you model it for all the 6 components? It’s near impossible.

In my model, there’s a scenario analysis of Growth and Discounting only for the Terminal Period. But generally speaking - yes, doing a simple scenario analysis is also good.

But I don’t think that makes Monte Carlo Simulations complicated. They’re also quite simple. If you have tools like the Crystal Ball for Excel (Prof. Aswath Damodaran uses it), it will make your job even easier.

It’s only a question of the level of analysis you want to do.

I do not have issues with Execution or Capital Allocation. But definitely they can do better on communicating with the Shareholders (Releases, Concalls, responding to Emails and so on).

Right, I dont mean for this to become a monte carlo vs non monte carlo debate. I was wondering if you had some insight on why it would work in valuations. It seems like its being done cause its the norm. Im sure you’ve heard the quote about being approximately right than exactly wrong. Monte carlo would give you a false sense of security. But again this is my opinion, to each his own.

As to modeling interdependent variables there are a host of simpler non-stochastic methods as compared to monte carlo. Anyway thanks for your blogs and keep them coming!

7 Likes

I’m not as smart as you, unfortunately. I’ll stick to what I know for the time being, if that’s all right.

1 Like

Hope you are doing well. No update for long time.

What’s your opinion on current market condition as on mid Aug’21.

In terms of long term perspective, will it be good to accumulate the well performed (in the portfolio) mid cap, small cap stocks?.

Siva

I haven’t updated much because my portfolio position remains more or less the same since the last update, with nearly 80% of it in Cash (Liquid Funds).

Portfolio (Ex-Cash): Cupid, DHP India, Goodyear India, Heritage Foods, Kovai Medicals and Ion Exchange.

Probably note-worthy is the fact that Ion Exchange is ~5.5x for me from Average Cost Price and ~6.2x from the lowest purchase price. KMCH and Cupid have also done considerably well over the years. But I am still relatively young in the markets (Serious investing done for less than 3-4 years) and would like to wait a lot longer to judge my investment performance.

Watchlist: Control Print, DFM Foods, Huhthamaki India, ICICI Lombard, IEX, IRCTC, NESCO, Navneet Education, RHI Magnesita, SIS, Swaraj Engines, UTI AMC, United Breweries, V-Guard Industries, VIP Industries and VST Industries.

I do not look at or care about broad market levels. My investing universe is pretty much the above mentioned companies and maybe 5-7 more firms that are in-and-out of my watchlist.

Within this set, I do not feel comfortable with the valuations of any of them. A couple of them like Cupid, Control Print or VIP Industries come close, but I have to really stretch my assumptions which I do not want to do anyway.

Especially since my investing capital has grown considerably in the recent past, I am more cautious than before. If the competition is between no-bargain valuations and earning low returns in the short term, then the latter wins hands down.

I sometimes wonder if I am trying to ‘time the market’, but I am not looking at market levels at all. I am only looking at the above universe of companies. Now before you quote Peter Lynch at me, please note that this is my money and not Peter Lynch’s money. I am quite comfortable handling it this way and confident that I can earn my target returns of 15-17% over the long term eventually.

21 Likes