Safari has not been able to generate Free Cash Flow since a decade. They’re still playing the catch-up game with VIP Industries. All the Market Share they’ve gained is mostly on the back of higher discounts and more lenient terms to the Supply Chain. So you’ll see that the Operating Margins and Cash Conversion Cycle of Safari is worse than that of VIP Industries, so much so that it’s led to them not generating any FCF for over a decade. Don’t get me wrong. They have a wonderful Management team (Definitely more Shareholder-friendly than VIP) and pretty much the same tailwinds as VIP Industries. But VIP Industries, at least in comparison, focuses on generating Cash. Their recent introduction of Caprese brand is a good example. Safari, even after a decade of competition with VIP, is focusing on capturing the Market Share through aggressive and in my opinion, unsustainable measures like discounts and credit terms. Maybe Safari will overtake VIP Industries, manage to reduce credit terms to channel partners and gradually reduce their discounts while still maintaining Market Share. But in my opinion, the probability of VIP Industries continuing what they do and generating decent amounts of FCF is higher than Safari doing all those things and turning Cashflow positive.

There’s nothing wrong with Relaxo. But Bata is the stronger brand of the two and that’s why I prefer tracking it instead. In any case, both of them seem way overvalued for my taste. I doubt I’ll consider them unless there’s a precipitous fall in their Share Price.

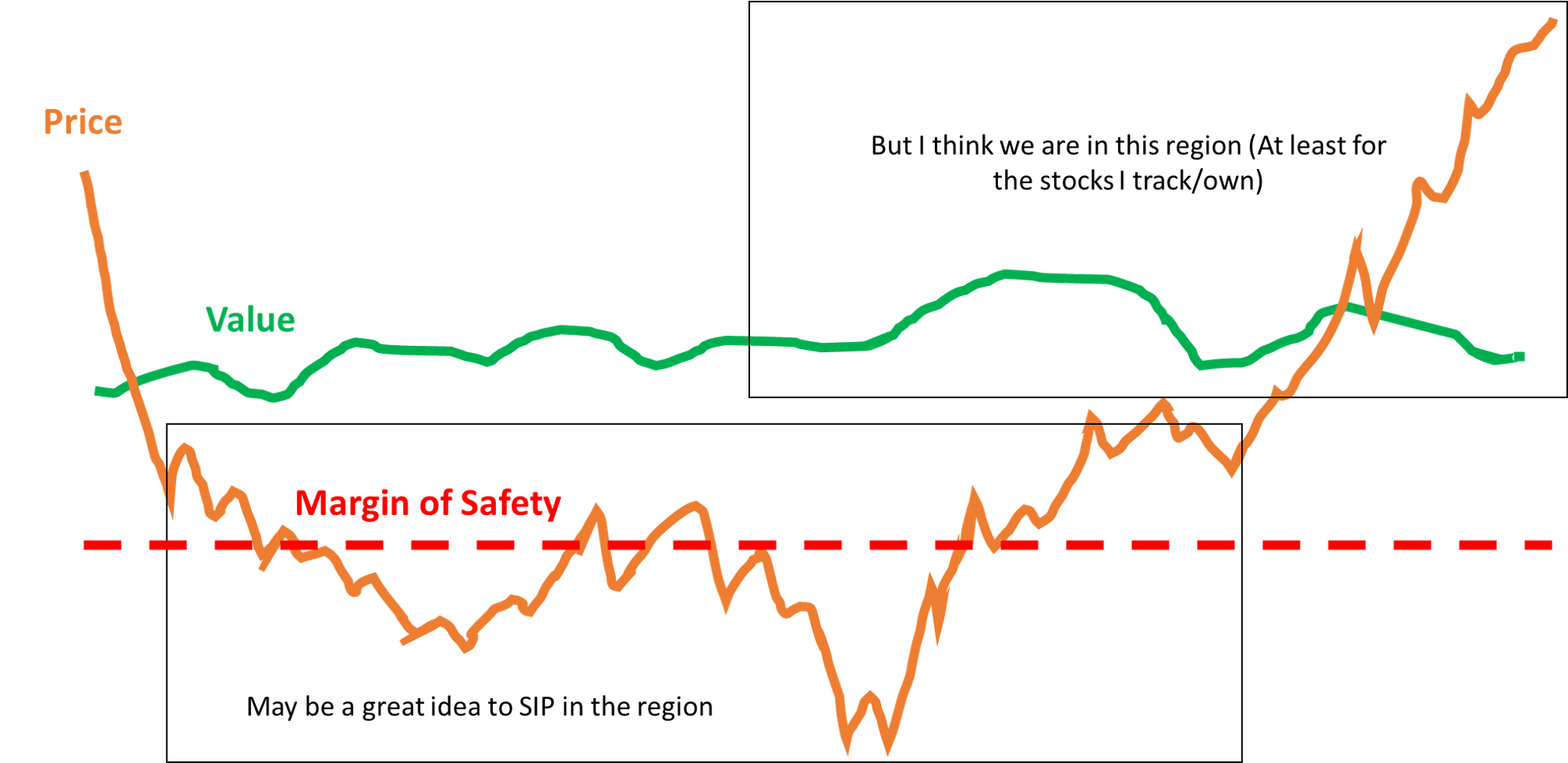

Portfolio has not changed much. But this is the first time I am holding a lot of Cash and so, it’s been a learning on its own. I had to fight FOMO in the past 3-4 months. But even as the market rolls down, I am fighting a different kind of FOMO, where I’m questioning whether I should invest the money before markets recover again. I am constantly reminding myself that market movements change the Price and not the Value. If not for anything else, 2020 will go down as an important year for me in terms of understanding my own behavior as an investor.

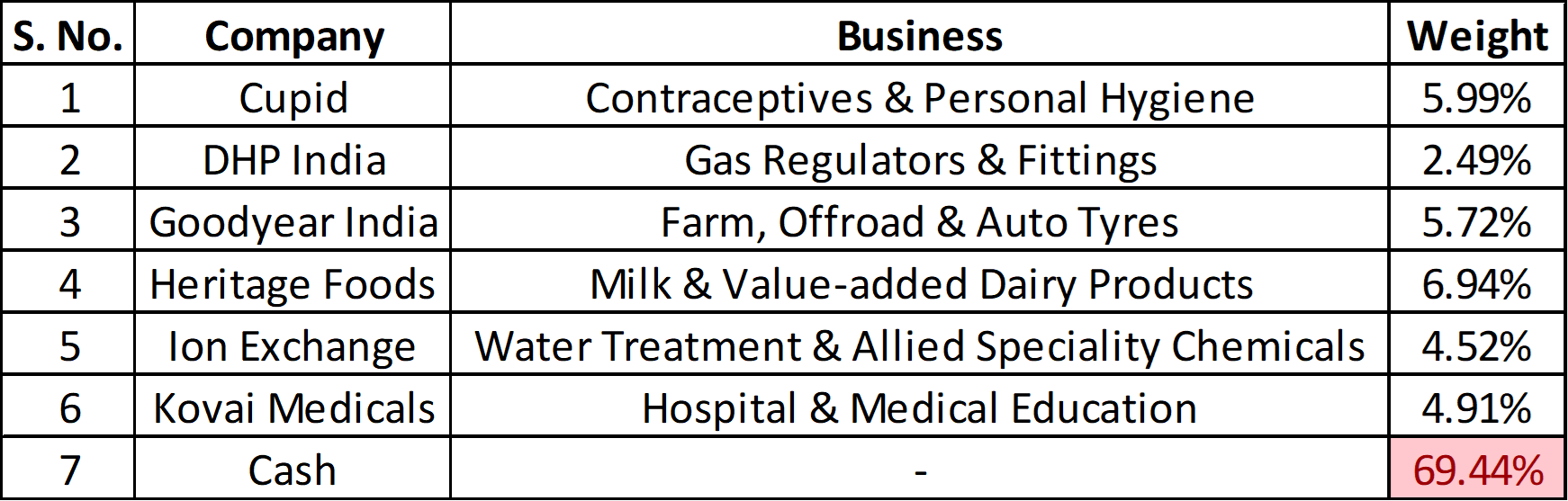

The only thing I can confidently say I’d buy more of right away is DHP India. But I’m waiting to look at the B/S once (Q2 Results) before making a decision. Or maybe a better bargain here will take away the need to look at the B/S - whichever comes first, I guess.

Heritage seems to have embraced the digital side of things. They’ve started to sell on some online platforms and through their own Heritage TUCH App (Which as of now is receiving bad reviews, but still - a start is a start). They also got rid of the FRL and Praxis holdings. Good riddance, as I personally considered them to be a distraction to the core business.

A little worried about KMCH. Hospitals are getting the worst of it from this pandemic and it’s quite apparent from the results. This especially comes off the back of a massive Capex, which is producing little Revenues as of now. I remain positive on the long term prospects of both the Hospital and the Medical College. On a related sad note, the MD/CEO has contracted COVID-19 and I’m hoping for his swift recovery. At the same time I am assuming his son is taking care of the day-to-day business. Maybe this period will offer a good feedback on how capable the next generation of Management is in running the business.

If you’ve been following the VP thread of Cupid Limited, you’ll know that I have been sending the Management questions over the past 2-3 months. Each time, they came up with a satisfactory response and promptly too. This has increased by conviction in Cupid substantially. I still don’t think the CMP offers any bargain. But when it does, I would not hesitate to double down.

Wall Street has started trading on Water (Source). Yes, water. I hope this brings about more focus on conserving and using water the right way. This issue has been ignored for far too long, in India too, but globally as well.

Watchlist

Cera Sanitaryware, City Union Bank, Inox Leisure, NESCO, Orient Refractories, Rajratan Global Wires, Solar Industries, Swaraj Engines, United Breweries, VIP Industries and VST Industries.

Very few changes.

Rajratan Global Wires is a new addition. I was not really sure about which Tyre stock I should track (I mean on the PV / CV side of things, not including Goodyear India), since large Capex seems to in place by almost every player. Rajratan seems to be a perfect replacement - instead of splitting my head over a specific Tyre player to track, I can track a company which benefits from the Growth in every Tyre company more or less. Besides, as I started researching the company, I realized there’s very little coverage on this and only a single fund holds the Stock (SBI Smallcap Fund). This has me more excited to understand the business.

Inox and VIP Industries fall under the same bucket for me, where I think they will definitely bounce back, but at the same time worried that every quarter of low to no business will significantly worsen the B/S. I don’t want to turn out ‘penny-wise and pound-foolish’ by taking a decision too early before the impact on B/S become more apparent.

There seems to be no respite for City Union Bank or Banks in general. Each passing day of lockdown / semi-lockdown increases the Risk of Delinquencies/Defaults further. Although going by recent releases, the Management communicates very well and lays out the Risks for the Shareholders to understand easily. I like that a lot about them.

Cera Sanitaryware Management has come out with positive guidance to my surprise. I continue to maintain that I paid too much initially and would wait for better Valuations to enter again.

Still split on NESCO. Based on scuttlebutt, the trend strongly seems in favor of at least a partial Work From Home kind of culture for most services-based industries, more so for the IT/ITES industry. But specific to Mumbai, given how cramped and congested it is, I doubt WFH is a viable long term option for most residents.

ORL, UBL, Swaraj, Solar Ind - No major changes in opinion. Just looking out for better Valuations. On Swaraj, assuming it becomes a bargain (If at all), I’ve begun to wonder if I should keep both Goodyear India and Swaraj Engines. Just seems a little bit redundant, if you ask me. I don’t have to answer this question immediately, but it’s still a question I have as of now.

why cera sir not kajaria , kajaria had same OPM margin,sales growth, FCF,debt free, in my opinion kajaria is available very high p/e than cera , please

share your opinion about this sir, i lm already also bias for cera this is also in my watch list

I’d suggest you look at the last few Analyst / Concall Meet notes from Cera Sanitaryware.

Cera Sanitaryware is into both Sanitaryware products and Tiles (Via Anjani Tiles and others). The management’s opinion is that over time, it will be easier for Cera to expand their footprint in Tiles, but it will be difficult for pure Tiles players to get into their market (Sanitaryware). So far, this seems to be true.

Besides, I don’t mind tracking Kajaria too. It’s also a good company. But like you mentioned, it’s not comfortably Valued and hence there’s no point tracking it anyway until it moderates a little.

Thanks Dinesh for your feedbacks and time. Appreciate the way you try to help others by providing your inputs! I agree on your points and myself a big follower of Peter Lynch. While I do think of businesses as babies but am very ruthless the moment something puts me off for example when Bajaj corp promoters pledged shares for no need of funds in business, I sold a business in one shot in an overnight decision. It was my biggest holding then and I was lucky to have sold it at its all time highs till date. I had bought it with intention to hold that baby till decades and watch it grow. Was not so lucky, but equally ruthless with another top holding L&T finance. Sold it completely at decent cagr but at significant below levels than all time highs when I saw the story faltering.

Why I gave above examples is that although I treat businesses as babies but not in love with them. I am very critical and ruthless with them if my metrics are not met. There is no romance, pure business. Also, I have more than 80% allocation to top 10 holdings with 60% to top 5.

Problem is that there are many such businesses which will do well in long term and you want a piece of them. Top investors invest in them in rotation depending on sector tailwinds. I am not able to do that as for that you need to sell some for no fault of theirs…small example is say an HDFC Bank today compared to say a Cipla…both are excellent businesses and in long term would do well…in medium term a Cipla may do better than an HDFC Bank because of sector tailwinds…with limited resources you need to sell HDFC Bank to buy a Cipla but has HDFC Bank done anything wrong? No…is it’s long term story in question, no? Then does it make it a candidate to add more in this stagnation? probably yes…but doing that you miss the upcoming Cipla story. I know if you open an excel we can calculate the best bet at different time frames and allocations but point is if you see growth, specially long term and your vision is long term…such dilemmas and resource adjustment is something I need to learn and develop a methodology around it…would be good to know your thoughts…Thanks.

I think this right here is the crux of the problem. I think it will be much better if we stop thinking what “top investors” are doing and comparing ourselves with them.

Further many of these “top investors” are just momentum traders, some of them are honest and upfront, they would admit it themselves as that style perhaps suits them best. Others only make a lot of noise.

Lastly, momentum trading can itself be very rewarding on occassions. Though other experienced members will guide you better on this but my suggestion would be to park a small amount of money (maybe 10-25% of your cash) on liquid funds, as this will discourage the temptations to chase hot stocks, and allocate them to play momentum only when you have strong convictions.

Hi, I’m not an expert, but just sharing what I know. Many investors follow a core and satellite portfolio approach to address your dilemma.

Core portfolio would comprise of your long term bets in which you have the strongest conviction. These are the stocks that you will continue to hold as long as your conviction in them remains allowing compounding to work.

Satellite portfolio would on the other hand be the momentum bets like what we see with pharma now.

Ofcourse for this to work, you need to set aside some part of your total cash for the satellite and use it only when you see an opportunity. What percentage should be core and satellite would be based on your investment framework. HTH.

Is there any reason for not SIPing money into markets? Just wondering as you have watchlist and money and not interested in timing the market, don’t you think deploying x% every month would help to normalise price fluctuation in the next 10 months.

This is apart from things like DHP India, Inox, VIP Industries etc., where I am explicitly choosing not to Value them until I get further clarity on the impact of COVID19 on their business.

Besides, as mentioned before, I have some trading and compliance restrictions in office. Doing an SIP is not that easy for me (Although I can put in the work and do it properly if I wanted to anyway).

@dineshssairam

I have been looking at cupid after it appeared in one 9f my screen filters.

i know you mentioned in one of recent posts that you like Cupid but price is not a good bargain at CMP. But I looked at long term median PE of it and found that current PE is almost half of long term median PE. So why do you feel that valuation is not good enough for current price?

I don’t consider P/E to be a good proxy for Value. Actually, any single measure isn’t. Value is a function of at least 5-6 key components like Growth, Margins, Reinvestment, Risk, Assets held and Competitive Advantage Period. P/E masks too many of these assumptions in order to be useful.

Specific to Cupid, I’d buy it close to 150 or below. I think it is fairly valued at 220. My views about the company are collated in the below blog:

Not just Coffee Can. If you’re following any method of investing that doesn’t involve actively researching and picking stocks, you’re automatically accepting lower returns. This includes SIP and Magic Formula type Investments.

Of course, the major benefit of these types of Investments is that you’re not influenced by your emotions as much. It’s a process and you’re following it religiously. This takes away a lot of Behavioral mistakes you can do in picking and analyzing stocks individually.

Ultimately, if someone with a good process and control over the emotions invests, they will be better off doing individual stock picking. They can also do rules based investing, but at the cost of possible lower returns.

Mr. Buffett never had a 5-25 rule. It was false information. He clarified it during an annual meeting. On capital allocation both Munger and Buffett agree that modern portfolio theory is BS and they are always thinking of opportunity cost while minimising risk via taking out the probability of loss times the possible capital loss from the probability of profit times the possible upside. Mathematically its not precise, but, precision is not what they look for. They are ready to wait for years if they have to, to buy something, but they will never buy at a higher price and without a margin of safety.

I have read the Kelly criterion, but I have not got, how to apply the theory in the real world. If you can explain with couple of practical examples, would be grateful. Thank you.

You need to decide 5 components per investment for the Kelley Criterion:

A time period

Expected returns over that time period

Probability of earning those returns over that time period

Expected loss over that time period

Probability of making that loss over that time period (100% - Percentage you chose in 3)

Now, deciding No. 3 would be the most difficult thing here. So what I do is I stick with a very conservative estimate for No. 2 and keep No. 3 as 90%.

Example

I expect to make at least 15% over 5 years in Cupid. But over those 5 years, if they don’t capture enough market share in the US Prescription market, my Valuation of Cupid may reduce by 30%. So the Kelley Criterion for Cupid will be (15% * 90%) - (30% * 10%) = 10.50%.

Of course, this 10.50% makes little sense as a standalone number. You should calculate this for all your holdings, sum it up and make a ratio out of them. Say, like below:

Whatever that Ratio is, will be your suggested allocation. You can include Cash as well into the mix, as shown above. Ultimately, don’t let it dictate your allocation but only guide it.

I haven’t tracked Vesuvius and Morganite as much. But ORL continues to be in my watchlist.

As I have mentioned in this thread before, Steel prices may not impact the Sales of ORL whether it is in an uptrend or downtrend. There is a high correlation with the Volume of Steel produced and the Sales of ORL. So if you’re tracking ORL, you should look into whether Steel production volumes will go up over a period of time in India and what might be the potential the factors contributing to it.