Hi Dinesh, wanted to ask you 2 things on Ion Exchange… margins are less perennially in this business and last 10 year OPM also proves the same. Also how do you reckon competition in this pace. Xylem is taking up lot of projects nowadays and also presence of biggies like LnT, GE in this space. what is the growth projection you have considered for next 10 years

2 Likes

First, Ion Exchange is really 3 different businesses: Chemicals, Engineering and Consumer. Here’s the Margin and Sales breakdown for all of them:

I believe you are talking about the Engineering business, which is the competitive one and of course, the largest piece of the pie for Ion Exchange. Margins here are fickle, based on the type and durtion of projection. The management has promised time and again that they will always consider Margins and RoCE before picking up any project for execution.

But if the investment promise from Nal se Jal is any indication, the market size here is going to be very big, enough to incorporate all the existing players and more. Here’s a quote from my presentation on Ion Exchange which I did a year or so back:

GOI has made a historical step by instituting a new Ministry for Water. Among their first announcements is a budget of a whooping Rs. 6,30,000 Crores to be spent over several years for water management in India. The Missions titled ‘Nal se Jal’ and ‘Jal Jivan’ offer almost 50% of the budget towards water treatment and EPC projects, around Rs. 3,15,000 Crores. Even if we assume that only 10% of the budget ultimately transpires, that’s still 26 times the TTM Sales of Ion Exchange India Limited (At ~Rs. 1200 Crores).

Now, the Chemicals business also has two sides: Low margin, high volume cheap chemicals and high margin, lower volume premium chemicals. Ion Exchange has chosen to produce premium chemicals in this space. They have talked about this in many of their concalls and even otherwise, it should be evident from the numbers in Chemicals business. In fact, the management has indicated that the Margins may expand a little more as they try to export more and involved in production of more premium chemicals (I believe they even opened a brand new research facility at Patancheru recently for innovating new chemicals).

They are trying their best to turn around the Consumer business. I consider this to be an optionality at best. It doesn’t take up a lot of resources, but promises good fortune if executed well. So I’m okay with this.

I actually bought it with the assumption that even a 15% Growth in Revenue over the long term will be good enough. Of course, my purchase price is considerably low because of this (Let’s just say it’s fairly close to the 3-year low).

Would I buy Ion Exchange at CMP? I doubt it.

3 Likes

thanks for the detailed response Dinesh…I agree with you on the opportunity side…its could be huge for them in next 10 years…I am also not comfortable with the CMP hence waiting on sideline…

1 Like

Hi Dinesh

Had some questions on Goodyear India. Would be nice to know your views

- In their newly released Annual report, Goodyear mentions that they expect the tractor industry to de-grow by 8-10% in the coming year (Future outlook section). But we know that the tractor industry has been growing extremely well. What am I missing here?

- If we assume the tractor industry to grow at x, what is the direct increase in demand of farm tires in relation to x

- Will Goodyear benefit from the ban of certain Chinese made tires in India?

- Since most commodity prices have crashed recently, will Goodyear use their cash pile to procure cheap raw material and hence their margins in the future could be higher than their current margins?

- Any opinion on Sandeep Mahajan and what he wants to do with the company?

- How are the demand supply dynamics in the farm tire space currently. In other words, if the tractor demand increases, will Goodyear be able to increase prices or is it a situation of over supply?

Thanks

1 Like

The Annual Report would have been prepared around February - March. But a large part of the growth we saw in agriculture recently is because of the labor migration, which happened in later months. But I don’t care about 1-2 years misses on Growth / Profits. I worry about long term Fundamentals and the Balance Sheet strength, both of which are good here.

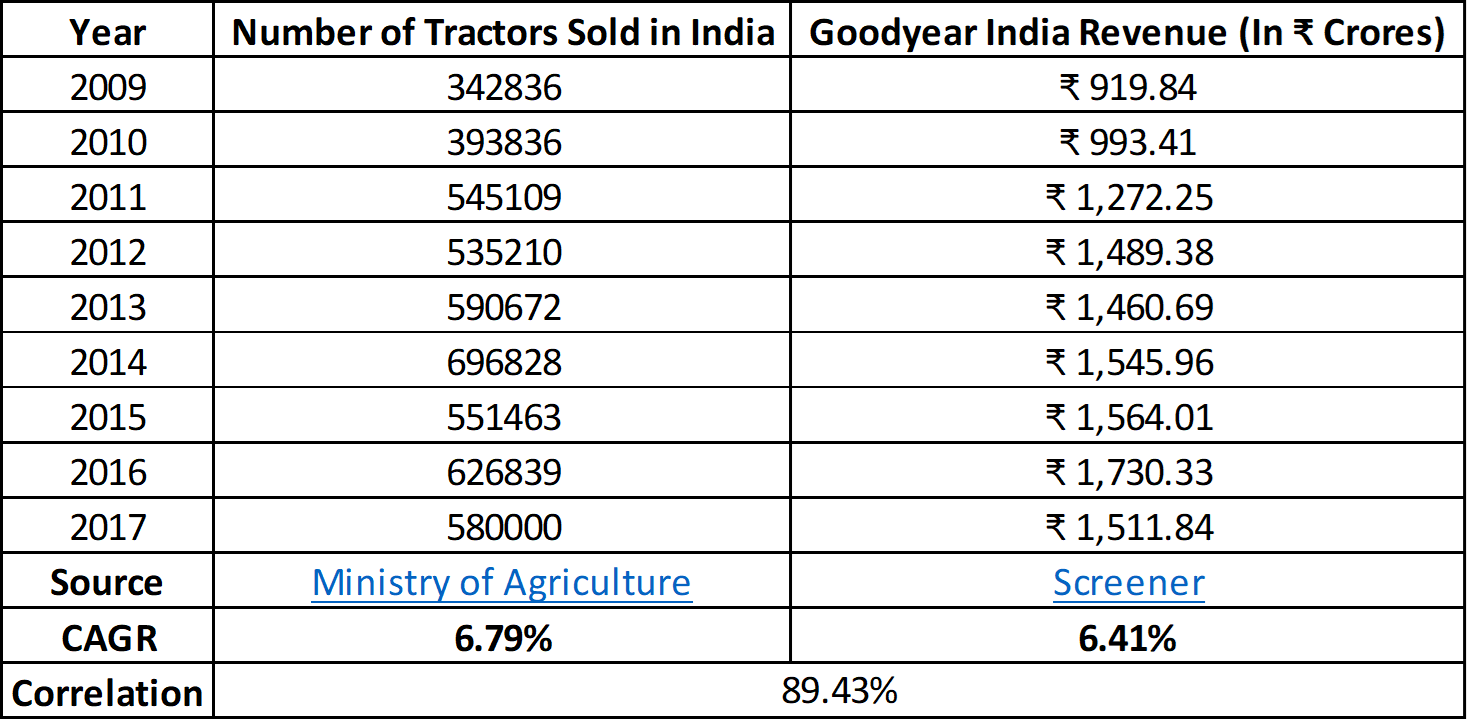

This is what I did when I “valued” Goodyear India for my blog. There is a undeniably strong correlation between Number of Tractors Sold and the Revenues of Goodyear India:

Goodyear India is also strong OEM player, so this shouldn’t come as a surprise.

Yes, to an extent. China is a strong player in cheap tyres. India, being a cost-conscious country, fits right into their chain. So a ban will definitely help (Although it will help players like MRF more, who are stronger in Replacement tyres).

Yes, again, most likely.

Mr. Sandeep seems to be a Sales guy and I think he can help Goodyear India a lot. His profile / work experience is impressive:

https://www.linkedin.com/in/sandeep-mahajan-a2684319

In any case, Goodyear India is the kind of business Warren Buffett would call “a business even an idiot can run” (Meaning, a business with strong fundamentals). So even a small contribution from the management side will go far.

Not worried about Economics. Demand and supply take care of themselves (Well, most of the time). But I don’t think Goodyear India has Pricing Power beyond a point. They have Pricing Power in the sense that customers cannot undercut them. But in retrospect, GIL also cannot increase Margins beyond an extent owing to competition. This generally applies for all players, including the likes of MRF. Value is created mostly because of brand recall and customer relationship.

3 Likes

-

(The Annual Report would have been prepared around February - March. But a large part of the growth we saw in agriculture recently is because of the labor migration, which happened in later months. But I don’t care about 1-2 years misses on Growth / Profits. I worry about long term Fundamentals and the Balance Sheet strength, both of which are good here )

= I was thinking the same thing but then I saw dates like March 31st, Apr 10th 2020 etc included in the annual report. This would mean that the AR has been prepared sometime after that. Think good tractor sales numbers were in by then. Hence the confusion -

(This is what I did when I “valued” Goodyear India for my blog. There is a undeniably strong correlation between Number of Tractors Sold and the Revenues of Goodyear India)

= Thanks, this is very telling -

Would you have any data or even anecdotal evidence which claims that they are benefiting from the China ban and the procuring of raw materials?

-

(Not worried about Economics. Demand and supply take care of themselves (Well, most of the time). But I don’t think Goodyear India has Pricing Power beyond a point. They have Pricing Power in the sense that customers cannot undercut them. But in retrospect, GIL also cannot increase Margins beyond an extent owing to competition. This generally applies for all players, including the likes of MRF. Value is created mostly because of brand recall and customer relationship.)

= I agree with the low pricing power point. But in many industries, including commodities, there is a tipping point of capacity utilization beyond which for the medium term, the industry enjoys temporary pricing power due to demand supply dynamics. Was wondering if you had any idea on the current capacity utilization of GIL and its trend in the recent few years

Thanks again

GOI reimposed ADD on some Chinese Tyres during 2016-17. You can clearly see that the Margins of all Tyre players jumped for a couple of years during this time. Of course, it is not black and white, because many other factors (Like RM Prices) also impact the Margins.

Unfortunately, no. They don’t reveal those statistics. But going by the fact that there has been higher than normal investment in Fixed Assets for the last couple of years, I’d guess they are operating at high utilization levels (A part of this could be for their latest experiments with the CV market though).

2 Likes

Can be off topic but good time to know this as well

Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks, and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.

Stanley Druckenmiller

This is something Im learning during this run. Very tough to get wrap your head around it, since it confuses a new investor as to whether he should play for the momentum or value pie.

Of course, Liquidity moves the market. But Liquidity doesn’t exist in a vacuum. Someone has to own that Liquidity and there’s a reason why they’re converting that liquid cash into a stock or set of stocks.

If that reason is overt (Which most of the times it is not), you can “play” the market. But if it isn’t (Which is the more likely case), your energy is best spent studying only the businesses you track or own and whether they are cheap or dear.

Liquidity was also moving the markets in 2000 and 2008.

7 Likes

Hi Dinesh,

Can you please throw some more light on Orient Refracrories. As per my limited understanding Refracrories are usually a proxy play to the steel industry and that’s what makes them cyclical. Cycle goes up and down with the steel cycle usually. So I would like to understand how Orient is different and not cyclical in nature. Looking at the EBITDA margins of Orient refractories we can see that they are better than its peers like IFGL and Vesuvius and in line with Morganite Crucible. I am more keen on understanding business per se. What are the things that make it non cyclical and hence different from its peers.

Please pardon my ignorance on these topics and also feel free to ignore the question if you think it is not relevant.

Thanks.

2 Likes

I owe my understanding of ORL’s business to @Chandragupta. He answered some of my important queries regarding its business.

The Steel industry is cyclical because supply/demand moves the prices a lot. But Steel producers cannot magically reduce capacity at will. It’s a capital-heavy business after all. They keep producing Steel and try to manage the inventory in order to make profits. In effect, crucibles / refractory products are more or less continuously used regardless of volatility in steel prices.

India’s total steel production (Volumes) has grown at about 7% in 2011-2019. ORL’s Revenue has also grown at about ~8%, while that of Morganite is ~6% during the same time. There is also a strong correlation between steel production and the Revenues of these companies (You can check the numbers and see if you wish to). Also yes, there is almost no cyclicality in the production of steel itself in India. In fact, we overtook China a year or so back and became the second largest producer of steel in the world. In any case, a growing country like India needs a lot of investment in infrastructure. Investment in infrastructure means investment in steel as well.

To me, ORL and Morganite are interesting ways to explore the growth of infrastructure in India, without taking on a risk in cylicality. Both are great companies in my opinion. ORL seems to have a lot of “triggers” in place, like a pending acquisition and support from a global parent. Morganite, on the other hand, has a slightly better cashflow profile and B/S strength. Scuttlebutt tells me Morganite products are of very good quality.

I need to do more research, obviously. But this is what I have as of now.

8 Likes

Thanks @dineshssairam… This indeed helps as a starting point to understand the refractory business in India. These are some great insights provided by you. Thanks Again!

1 Like

Late update, but I exited Cera Sanitaryware a couple of weeks ago. I still believe in the management and the company has a long way to go. But I think I under-estimated the length of the Real Estate slowdown in India. COVID19 has only increased it. So, selling is admitting that I overpaid. Luckily, I was only in single digit (percentage) losses. Even now, Cera has just moved into the top spot in my watchlist. I will be quite interested in buying it at lower levels (I haven’t re-valued it yet however).

In other news, Cash is closing in on 70% of the portfolio.

Watchlist has grown a bit. I am trying to catch up on some reading, since it is Annual Reports season.

Cera Sanitaryware, City Union Bank, DFM Foods, Inox Leisure, Jamna Auto, KPR Mill, NESCO, Navneet Education, Orient Refractories, SIS, Suprajit Engineering, Swaraj Engines, VIP Industries and VST Industries.

2 Likes

Hello Dinesh Sairam,

I have one question for you.

Regarding investment style do you read any company quarter balance sheet and then invest onto it the next day.

For eg- on Thursday laurus lab posted very good results and it was obvious that stock would rise the next day and it did around 18% and still can do good next week.

Similarly kilpest posted good quarter. Since you have a good percentage of cash, do you use or recommend these type of strategies to invest.

1 Like

hello dinesh sai ram sir ,

thought process behind choosing heritage not hatsun ? please tell your decision ,happy value investing.

1 Like

I think that’s a dangerous practice. It takes at least 1-2 weeks of regular 3-4 hours of reading every day just to familiarize myself with a new company. If it’s an industry I already know, maybe it will be a little easier.

The simplest and most effective practice is just to start with two things:

- Time Series Analysis (Compare your own company numbers with its historical numbers)

- Competitive Analysis (Compare your company’s numbers with the closest competitors)

While doing these, you should make note of areas you do not understand fully (Ex: “Why is my company earning less Margins than the industry’s average Margins?”). Once you’ve got all your questions, you can try to find answers from the Annual Report, Concall Transcripts, Management interviews and so on. If you can get an insider from the industry to answer some of your more generic questions about the inner workings of the industry, that would round it up nicely.

I don’t see any way in which this will take just a couple of days. This will take weeks, if not months.

Hatsun is an excellent company with a vast array of familiar brands. But they have levered themselves up to the neck and ruined their Balance Sheet. Even now, after a recent massive round of equity dilution, their D/E is still above 1.25. On top of this, their Interest Payments are almost equal to their PAT.

If they have poor business for even 1-2 years (Not saying they will), their B/S will further worsen. This means that Hatsun’s managers are very interested in short term profits to keep the treadmill running. They cannot afford to take even small risks in terms of innovating new products or capturing new markets (Again not saying they won’t - but the leverage is an inherent discouragement).

Hatsun would have been my first choice had it not been for the leverage.

6 Likes

Dinesh, it’s good to see your portfolio. Will you be able to add a price range which would reflect fair value after considering the MoS? Would help members to make a buy or sell decision based on your valuation.

P.S - Only if you’re ok with it and if it makes sense.

1 Like

I don’t think it makes sense as of today. I am very young in the markets. I might potentially reveal my returns 5 or so years down the line (So that I complete at least 7 years in the markets). Let’s see.

Besides, I don’t mind telling people at which price I would buy a certain business I am interested in (Given I am sure about the business prospects myself). I do all the time when they DM me here or on Twitter. I simply don’t want to post my average purchase price on a public forum just yet.

Even if I say so myself, I am fairly confident in my ability to value companies. I am here on this forum to discuss about the underlying businesses themselves, which you can never learn enough about.

4 Likes

We have talked before about your cash allocation in liquid funds and want to explore this further.

In times of uncertainty & crisis, would you recommend moving a portion of cash to gold mutual funds or ETFs? Is there anything you have against this avenue of allocation? Please share your thoughts!