I valued it about 2 years ago. But this was one of my earliest valuations and I would have to admit that I may not have put in enough work to research the company. I was more interested in testing out my model.

After that, I stopped tracking the company because I wasn’t interested in it. I don’t think they have a strong Competitive Advantage. I also was not very fond of their Cashflow cycle. They have to hold large amounts of Inventory at any given time. What they do have going on for them is a good brand and a location advantage. Some aromatic Basmati variety can only be grown well in specific regions of India and Pakistan. But even locally, there are very little barriers to entry.

Corporate Governance is also not a strong suite. You may want to read through the VP KRBL thread to know more.

Parag milk foods is actually a great candidate and I would argue that it is a much better bet. They have more value added products and are way more innovative than either heritage or hatsun. These two are basically commodity companies and none of their products seem to be innovative value-added products. All these three players are very strong in their respective zones and will not be able to disrupt each other. A 75% procurement os not too far from 95%. I would rather see the amount of growth and innovation and Parag beats the two based on this criteria.

IT/ITES is not within my Circle of Competence. I invested in 1-2 of them over the years, but I was constantly worried or looking over my shoulder. Not my cup of tea, unfortunately.

Sonata is down for a reason. They have heavy exposure to the travel sector… All IT companies are not the same. I am invested in Sonata for the long term.

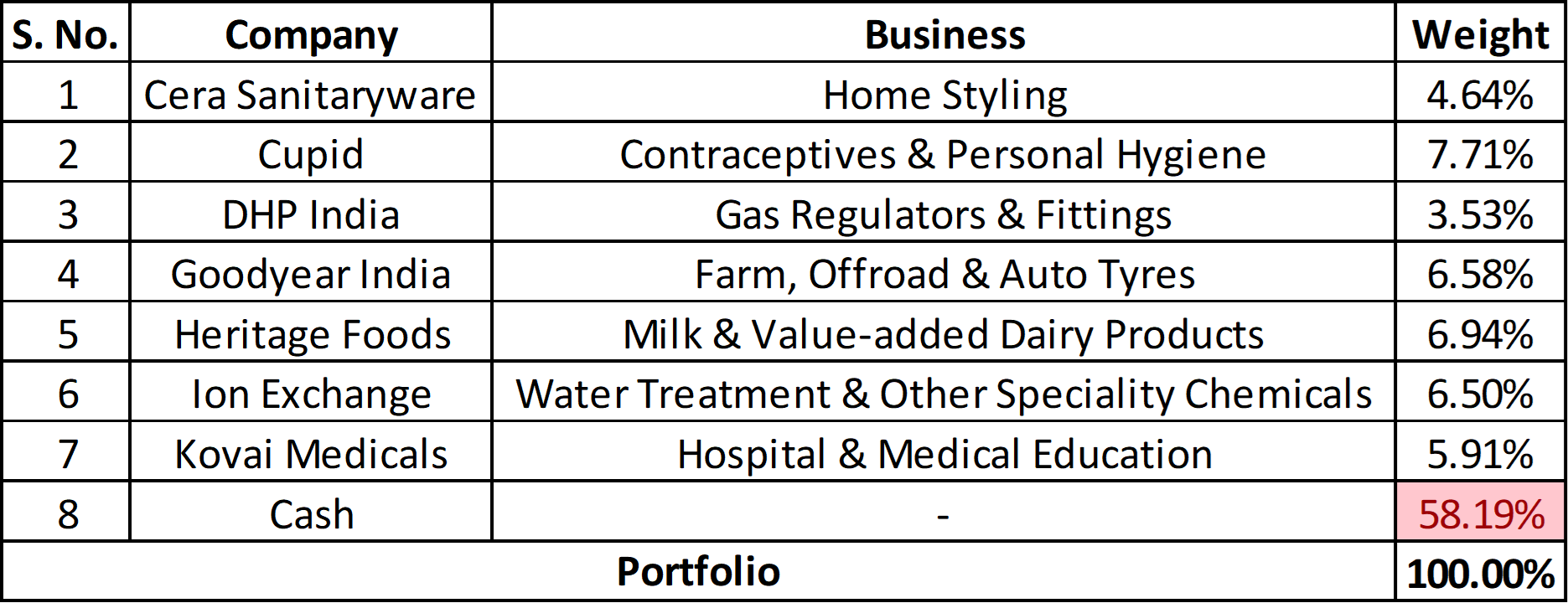

Not much to update per se, except to say that Cash has become a substantial position. I did invest in KMCH and Heritage a little bit, but Cash is closing in on 60% of the Portfolio.

Watchlist: City Union Bank, Eicher Motors, Inox Leisure, JK Paper, Jamna Auto, NESCO, Orient Refractories, Swaraj Engines, VIP Industries and VST Industries.

Read up about Orient Refractories over the last 1-2 weeks. Interesting business in the sense that it serves a cyclical industry, but it is not cyclical in itself. Seems like there are a lot of “triggers” lying in wait for the company.

VST Industries is back to the watchlist after the MD resigned. I tried to understand if there was a specific reason behind the act, but couldn’t come up with anything.

JK Paper / Jamna Auto were things I have been tracking on-and-off since long. Not interested in them too much at the point though.

COVID 19 Impact

I have to admit, I over-estimated my knowledge about this crisis and the impact of it on the companies I own / track. My biggest surprise came with Inox Leisure’s Q4 Result. I assumed profitability will take a hit and B/S may worsen a little. But Debt has jumped 5x, which was way more than what I had anticipated. I am okay with poor profitability on the short term. But a worsening B/S is a different story altogether. On a related note, PVR is also raising Equity, because they are already levered up to the neck. Things are becoming worse, when I though they would be bad at best.

There has been very little material communication from any company I track / own regarding the impact of the lockdown / virus. The ‘COVID19 impact’ releases mandated by SEBI are generic and hardly useful. But I suppose even the managements are unsure when things may get back to normal.

For the time being, I am not in a hurry to invest. I will invest if:

I understand, to some extent, the impact of COVID19 on the businesses I track / own (AND)

There is a bargain

(OR)

There is a massive bargain

On #3: For instance, I am still on the fence about whether WFH will become widely adopted or not. This directly impacts my understanding of NESCO’s business for the long term. But if there is such a large bargain that will even cover for my lack of understanding of NESCO’s IT business, then I would have no problem investing in the stock. The same goes for pretty much everything I track / own.

Dinesh, sitting with 60% cash means you are anticiapting a big March like fall! Seems you are betting a sure fall post the Q1 results if not before… but what if the markets are already discounting the bad Q1 in the current prices?

If WFH were to become the norm, wont’ Cera also be impacted to a certain degree. Plus RE being down does seem to impact Cera i believe…

I see no Pharma names in your PF or watchlist, while the street seems to agree that Pharma is coming out of a long downturn/consolidation and is ready to lead the next rally!

Also what makes you consider a small pvt sector bank in the banking space? should’nt the large players have an edge in this space? And if interested in small pvt bank, why not look at DCB? Both NNPA% and GNPA% are lower for DCB as compared to CUB…

I am not expecting anything. I am not invested because I don’t understand the impact of COVID19 on the businesses I track/own. I initially thought there will likely be a 2-3 Quarter impact (So, bad P/L or Cashflow for the short term). But the more I research, the more I am unsure if it is only going be an impact on the P/L alone. This could potentially be a bit longer term impact, which is what I am trying to understand. I am guessing even the management themselves are clawing in the dark and I don’t blame them.

Any rally fueled by anything apart from a genuine improvement on the ground will likely come to an end quickly, as history has taught us. But I am not sitting in judgement here. If the stocks I own/track continue to rise without the underlying fundamentals becoming better/clearer, then I will keep my cash intact.

Yes. To be honest, I am on the fence about Cera. I bought it with the assumption that the slowdown in RE was done and recovery would begin. But COVID19 has potentially further extended the slowdown. I am not too confident about my current position. But I guess if I get some Margin of Safety (Say, a price of 1500-1700), I wouldn’t mind investing more.

Pharma is not within my Circle of Competence. There are lot of layers to understanding Pharma and I have to admit I don’t know much about it. I can understand smaller and simpler businesses like Amrutanjan Healthcare, but that’s about it.

I added CUB in the anticipation that a bulk of their loans will go bad. I wanted to see how they will react / recover. They have one of the largest exposure to MSME/Small loans among listed peers. Otherwise, not particularly interested in any BFSI company at this point. The whole space, in my opinion, is going to be in distress for at least a year or two.

As it should be apparent from my terrible investments in DHFL and IndusInd Bank, leverage and bad times don’t go hand-in-hand.

Thanks Dinesh! much appreciate your clear thinking and articulation!

Agree, to the part of being comfortable in sitting in cash even then you see stock prices rising, similar to continuiing with ones SIPs even when we see the stock prices falling. Investing is as much about Psychology as about number crunching or business strategy. And its tougher than learning accounting!

How do you handle situations when you are sitting on a lot of cash in hand waiting for the next investment opportunity? Do you simply park them in your savings bank account which pays negligible interests or short term fixed deposits which offer slightly better interest rates or do you manage it more efficiently by moving it to short term liquid funds? Please share your thoughts!

I usually put it in Liquid Funds (Direct - Growth). By that I mean funds that are more than 80%+ plus in Money Market Instrument and/or Government Securities.

Parag Parikh Liquid Fund is a good example. But any fund following this criteria is good enough.

The aim here is Capital Protection, not necessarily Appreciation.

Thanks for your reply Dinesh. I have not come across any good site for liquid funds. Can you point me to a good public site, if you are aware, to select liquid funds based on these criteria?

Apart from my Portfolio and Watchlist, I may have studied maybe 7-10 more companies well. So my total tracking list (Historical + Current) is very limited.

Unfortunately, I’m not experienced enough to have opinions on several different companies.

@dineshssairam What are your views on iON exchange growth and valuation considering current situation? Do you see any positive/negative impact on the company?

I’m positive on the long term prospects of Ion Exchange, that’s for sure. India formed a Ministry for Water very recently. We have long way to go for awareness in the sanity of water that’s being used and disposed by the industry.

As far as the short term is concerned, I’m sure Covid-19 will have its impact. Tenders may be delayed and projects will take longer to get executed (Stretched WC and Revenue cycles). I’m okay with this, as long as the Balance Sheet does not take too much damage in the form of increasing Debt or other such measures.