Ideally there should be no impact. The company has hedged the entire position. So the fall in FRL’s price should not change Heritage’s Value at all. But let’s wait for management commentary anyway since the lock-in should be ending soon.

2 Likes

Any specific reason to chose Inox over pvr in watchlist?

Why did you remove ITC, Petronet, VST from watchlist?

Any particular reason choosing TVS over Hero motocorp? Is it because of their recent deal with norton or better product portfolio which includes auto bikes and Ev as well ?

No financial services ( banks AMC’s insurance companies ) in the watchlist?

Debt. As such, there’s a fair chance that PVR and Inox will have to take additional Debt to manage Opex until things normalize. So the fact that PVR already has 1.18x Debt-Equity isn’t good in my book. High Operating Leverage + High Financial Leverage is never a good combination.

I removed ITC because I felt VST Industries is better in comparison. I guess you could say VST Industries is still in my mind, but I would like a much lower price (2000-2200) for it to become somewhat attractive.

I keep going back and forth with Petronet. I believe it’s got a great future ahead. But the Risks are the PSU-nature of the business and the ownership structure (50% owned by their sole Customers aka India’s 4 largest Oil & Gas giants). Once Gas demand increases in India, I’m afraid Petronet’s coffers will be raided.

Yes, mostly because TVS has been innovating / at least trying out new things. I like companies that aren’t afraid to experiment. I think Hero can be a decent investment too for someone looking to earn Dividends.

City Union Bank

3 Likes

Hi Dinesh,

Are you considering VST now that it’s come to 2900. It did touch 2700 types on March 23rd but with lockdown reducing there should be a hoarding of cigarettes with the fear of stock + Future lockdown situation

No, I would want it to be below 2000-2200 for it be somewhat attractive.

Just curious TVS motors d/e is 2.3 vs bajaj/hero cash rich cos . And if bajaj/hero resort to heavy discounts post the lockdown to gain market share in the domestic market, this could be a potential risk for TVS Motor as it does not have the balance sheet to reciprocate the aggression of its competitors.

A large portion of TVSM’s “Debt” is with TVS Credit Services, its NBFC/Financing Subsidiary. The Standalone D/E of TVS Motors is only about 40%.

I used to have a similar confusion too. But essentially companies like TVSM, M&M and AL have captive NBFCs who fund the vehicles sold by the parents. This “Debt” is different from the Debt taken by the parent for their Operations, in the sense that the former has Default Risk (Protected by the law) and the latter has Business Risk (Not protected by the law).

Imagine you hold an Auto Stock and a Bank Stock in your portfolio. If someone says “Well, the combined Debt in your Portfolio is very high, your Portfolio is Risky”, does that make any sense? In a similar fashion, TVSCS is a different entity from TVSM - it just happens so that TVSM holds a stake in TVSCS. Even if something terrible were to happen and TVSCS goes bankrupt (Unlikely, because these type of NBFCs have very low leverage), TVSM will not be liable to bail it out (Of course, they’ll have to write down their entire stake in the company though).

6 Likes

Thanks for the reply from above you cleared that TVS does not have default risk but still has weaker balance sheet than Hero/Bajaj if price discount/ price war happen in market. Nonetheless if you think thats priced in completely your decision to invest though I still find other options in auto sector better as investment personally.

Disclosure: Have Eicher in portfolio

1 Like

Hi Dinesh, Are you waiting for this pullback rally to cool a bit to buy these watchlist stocks. The number of cases are still increasing, but the market is not listening to it. Is it better to wait till June quarter results which has major effect of lock down, if we miss to invest in March.

I know that few of the stocks are still corrected 40-50% from their Jan-Feb highs but the feeling that the stock prices may further fall either because of further increase in positive cases or poor next few quarter results is stopping us to invest right now.

It is only a physiological issue.Can you please give some guidance as we don’t have much experience in these type of situations?

Even I don’t have a lot of experience in these type of situations. But I generally don’t try to time the market. Nobody knows which way the market is going and even if they did, they wouldn’t know which way individual stocks are going.

So my advice would be to be very conservative in estimating a Purchase Price (This is regardless of a pandemic or not). Once that Purchase Price is reached, invest regardless of market trend. That’s what I’ve been doing. Only time will tell if this is acceptable or not.

3 Likes

@dineshssairam could you please tell estimated entry price of Eicher. Because I’m actively looking for lower price blow to 12.k

I think below 12,000 is a good price to enter too on an absolute basis. But on a relative basis (Opportunity Cost), I think there are better options available (At least for me).

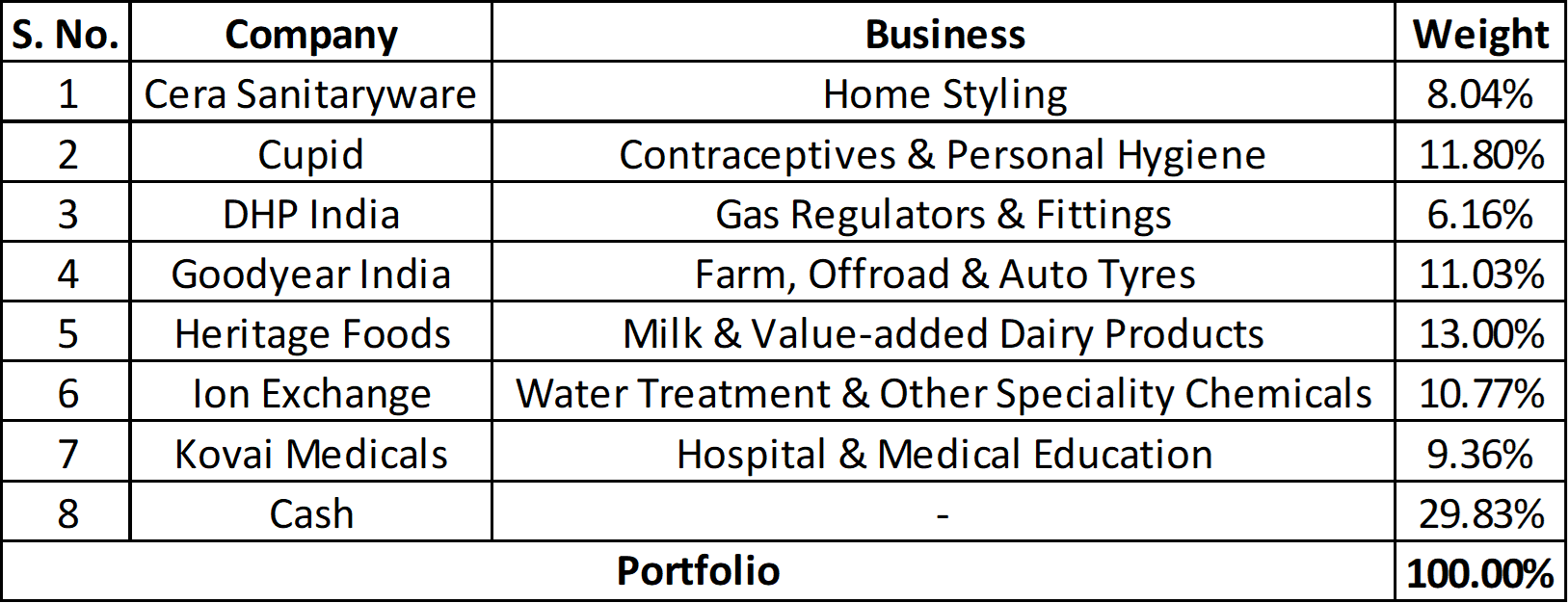

For instance, I would much rather invest in Goodyear India, DHP India, Heritage Foods etc from my own Portfolio rather than a fresh entry in Eicher Motors (Just an example - not indicative of anything). I would be happy to invest in just 1-2 companies from my watchlist. I don’t want to diversify for the sake of diversification.

4 Likes

Hi Dinesh,

What prompts you to incline towards Goodyear India vis-a-vis Balkrishna Industries? Though not a direct competition in India, but globally BKT has been gaining ground in OHT industry over other competitors.

I’m sure you must have compared both to come up with a preference towards Goodyear. Can you let us know your logic for the same? Is it due to Goodyear’s financial strength?

I have written about Goodyear India when I made a thread for it:

When I research it initially, I remember comparing it with only MRF. Even MRF isn’t a comparable competitor. Nevertheless, my thesis was centered around the fact that Indian Agriculture could do with a lot more mechanization. Goodyear India had an ample role is that Value Chain (Similar to Swaraj Engines too, which is in my watchlist).

I haven’t shortlisted or analyzed BKT so far.

2 Likes

Portfolio update 1: I have sold IndusInd Bank a week or so back. I took a 55% loss from the Average Price. There were primarily 3 reasons for it:

-

I didn’t like the way the management kept me in the dark during these testing times. Well, they have always been like this (At least Sobti was - up until a few months back). But these are extraordinary times. I would want to at least know the potential risks in their portfolio, like the possibilities of an ALM Mismatch, SMA1/SMA2 Assets blowing up and so on. But nothing of the sort was communicated in detail. In recent times, Kotak Mahindra Bank did a good job of explaining their position to their shareholders.

-

Continued selling and pledging by insiders, when actually the opposite was promised. The Hindujas have not exercised their Option to increase stake in IndusInd Bank (Because why would they - it is after all Out of the Money).

-

The final nail in the coffin - a very casual stance towards COVID19-related stress. A 200-crore Provision is next to nothing. Ironically, I bought IndusInd Bank because they provided fully for DHFL and I had to sell because they didn’t provide nearly enough for COVID19.

Portfolio update 2: Received the Cash I was talking about earlier, so Portfolio is Cash-heavy at the moment. I still have some pending obligations for which I may need to take out Cash. Once the amount I can definitely save is clearer, I will start deploying it - most likely in my own Portfolio first. There’s a small chance of 1-2 new additions from the watchlist too.

Here is the Latest Portfolio:

Latest Watchlist

Nilkamal is the only “new” addition. I say that because have been tracking it on-and-off for almost 2 or so years now. I am skeptical of their ability to scale in the Furniture division (@home), although they have been addressing some issues by closing down stores that are dragging and changing the product mix a little. But there is some comfort in lower valuations, is what I feel.

City Union Bank, Eicher Motors, Hester Biosciences, Inox Leisure, KPR Mill, NESCO, Nilkamal, Solar Industries, Swaraj Engines, TVS Motors, VIP Industries.

5 Likes

Hi @dineshssairam good see a plastic stock in watchlist. My only question is why not Cello i.e. Wimplast ? It’s doing much better than Nilkamal and has better diversification in terms of products plus market leader

Just a opinion Dinesh…on a lighter side, I feel in the name of valuation and numbers you are missing out excellent stocks in this time…

3 Likes

Interesting point. I think in companies with iffy management, you need to calculate very very low terminal value (as they will probably be competed away in the long run), PLUS you need a high discount rate, as the value of money in the management’s hand is much less than that in your hand.

Wonder how you think about these aspect, Dinesh.