I have been getting a LOT of requests along the lines of how to get started with investing in equities. Here’s my humble attempt at putting together resources that will help someone interested in investing to take their first steps.

Step 1: Devise an Investing Framework

“To invest successfully, one doesn’t need a stratospheric IQ… What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework.” — Warren Buffett .

We start with something that’s inherently redundant. The first step in the process of figuring out how to invest effectively, is to have an effective framework of how to invest. Confused? Let me provide you with a couple of examples:

A framework is essentially a set of rules stating, “In my investing life, I will do certain things and I will not do certain things.” The framework should tell you how to react to any situation you may come across in the market. You need not adhere to any of the frameworks I provided as an example above, but make sure you create your own. You may start with a compact, rule-of-thumb sort of framework and develop it to a full-fledged model later on. Don’t worry if you can’t get a complete picture immediately. Rome was not built in a day.

The most difficult part is not creating the framework itself, but actually sticking to it. Investment failure comes from changing your mind far too often. A framework keeps it in one place.

Step 2: Read. Read. Read.

“ Read 500 pages like this every day. That’s how knowledge works. It builds up, like compound interest .”— Warren Buffett .

The importance of constant learning cannot be overstated. You must become a learning machine. Like Steve Jobs said, you can only connect the dots looking backward. You never know when a specific knowledge you picked up will help you. Along the way, it mostly definitely will and you’ll be grateful that you read about it all those years back. Here are a few resources to help you get started with that:

Of course, by ‘read’, I actually mean ‘learn’. If you are able to read magazines, blogs or watch videos on YouTube, that would do quite well too. Get your hands on anything that adds to your knowledge and just read, read, read.

Step 3: Understand the basics of Accounting, Finance and (preferably) Economics

" You have to understand accounting and you have to understand the nuances of accounting. It’s the language of business and it’s an imperfect language, but unless you are willing to put in the effort to learn accounting - how to read and interpret financial statements - you really shouldn’t select stocks yourself. "— Warren Buffett .

They say Accounting is the language of business and Finance is the life-blood of business. Without understanding the basics of these, you are not going to get far on the road of successful investing. I will go far to say that an understanding of Economics is also necessary. Use the following references to slowly ease into the general Accounting, Finance and Economics concepts:

Once you are done with the basics, try looking at the Annual Reports of the companies you like. Look at their Statement of Accounts and try to understand every number. Everyone likes to read differently, but this primer of reading a 10-K (Annual Report) lays out a DIY.

Note down any doubts you have and see if you can get them clarified from someone who’s an expert. Remember, practice makes it easier.

Step 4: Define your Circle of Competence

“ Everybody’s got a different circle of competence. The important thing is not how big the circle is. The important thing is staying inside the circle. ”— Warren Buffett .

The quote above is everything you need to know for establishing this very important step.

Time is limited. You cannot dedicate your energy to every opportunity you come across. So when you first hear about a company, admit to yourself honestly if you are competent enough to understand the company’s business. If you don’t know enough, move on. Just move on. There are plenty of other first left in the sea. This is easier said than done. Information overload is a big problem in this age of abundant data. Try to avoid the clutter by drawing a boundary and vowing to never step out of it.

Of course, it would be ill-advised that you remain within the same Circle of Competence forever. You can try to expand your knowledge of things over the years and the Circle will grow right along. The idea is always being honest with yourself and always knowing the boundary.

Step 5: Scout for Investment Opportunities

“ You do things when the opportunities come along. I’ve had periods in my life when I’ve had a bundle of ideas come along, and I’ve had long dry spells. If I get an idea next week, I’ll do something. If not, I won’t do a damn thing .”— Warren Buffett .

Investment opportunities do not appear out of thin air. You have to constantly (Not obsessively) be on the lookout for them. You may not have to invest in 25 ideas a year, but there’s nothing wrong in shortlisting so many. Even if you end up rejecting the majority of them for whatever reason, the process is definitely going to help you in the future.

- Regularly read business magazines or at the least, the business section of newspapers. Watch out for business-related news items or content on social media.

- Subscribe to business/finance/investment blogs, YouTube channels and podcasts.

- Whenever you purchase a product or use a service, try to find out the company behind it. Read a little about their background. Do this as a compulsive habit.

- Make meticulous use of websites that help you shortlist investment ideas. Screening can be particularly effective if you know what you’re doing (Screener is useful for Indian companies). Here’s a few more of them:

- Join online communities on investing if possible. These days, there are also WhatsApp groups on investing. Make sure you stay put in only those groups that add value to you as an investor.

Step 5: Research a Company

“ You’re neither right nor wrong because other people agree with you. You’re right because your facts are right and your reasoning is right – that’s the only thing that makes you right. And if your facts and reasoning are right, you don’t have to worry about anybody else. ”— Warren Buffett .

Once you’re equipped with basic financial knowledge and a handful of companies you are interested in, you will be ready to look at a live case. Unfortunately, there are no straight-forward guidelines to researching a company.

Start with the company’s website, Annual Reports and Concall notes. If you are able to talk with someone in the company’s value chain (A customer, a supplier) and an insider (An employee), that would round it up. If this is not possible, at least talk with someone working in the same industry. Your aim, at the end of the ordeal, should be to understand the company and its transactions enough to rival an insider’s knowledge.

Once you are done, you should be able to write down 10 distinct, well-defined paragraphs on why you should invest in the company and a few more points on how the company could be taken for a ride. Some would call it an ‘Investment Thesis’—short notes on what excites you about the company and what are the potential risks.

The book “Common Stocks and Uncommon Profits” by Philip A. Fisher could help nudge you in the right direction. Once again, don’t let the book constrain you. Feel free to follow any process you want. Let the book be a guide, not a blueprint.

Step 6: Perform a Financial Analysis

“Beware the investment activity that produces applause; the great moves are usually greeted by yawns.”— Warren Buffett .

In the earlier step, you understood the story behind a specific set of companies. In this step, you will look at the numbers of those specific set of companies. After all, a company is nothing but a bunch of stories and a set of numbers that keep the stories grounded in reality. The following resources may help you in this regard:

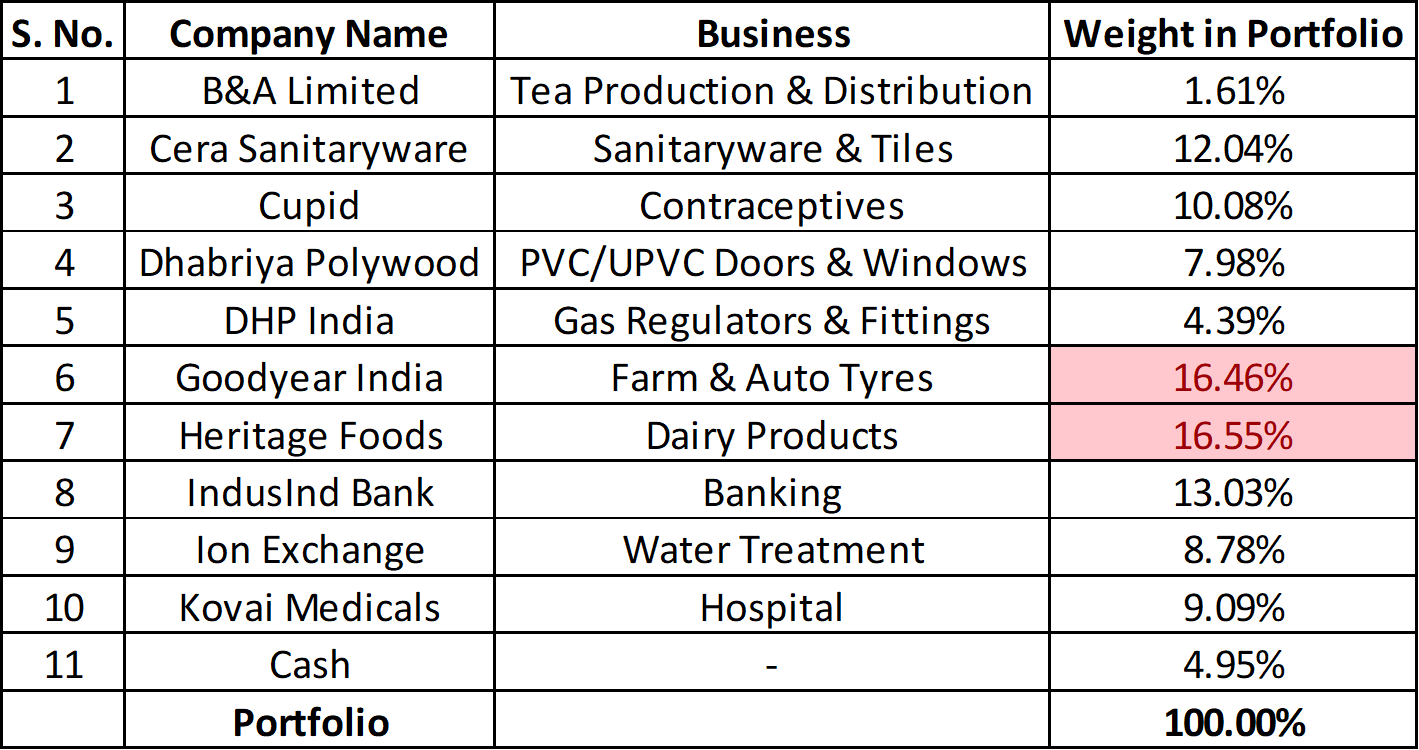

Please do note that it is not only vital that you perform this for the company in question, but also for comparable competitors. For instance, if you find that the company you are interested in has a Profit Margin of 10%, while their competitors have 12% or above, it helps you ask the question “Why does my company have lesser Margins than the industry?” The aim of this very exercise is that you ask successive questions like this and find out the answers.

In fact, you can also cross-verify your stories about a specific company using the numbers reported by them. In your research, if you found out that the management have claimed that they are cost-leaders, then it holds to logic that their Margins should be higher than the industry or at the least—their current Margins should be higher than their previous Margins. You can do several fact-checks like this. This is how you build the conviction about a company.

At the end of this long and draining exercise, you will have looked at both the sides of the prism—the stories and the numbers of a company. The next logical step, then, is to put them both together.

Step 7: Value a Company

“ Price is what you pay. Value is what you get. ”— Warren Buffett .

Regardless of how good a company is that you have identified for investment purposes, you can still screw up by overpaying for it. It is of utmost importance that you understand, roughly, how much a company is worth and then pay even lesser. That is the sure shot way to investment success.

As for as Valuation itself is concerned, I will not pretend that it is in fact easy to understand. I personally believe that either a Discounted Cash Flow or a Dividend Discount Model is the best way to value a company. However, the ‘Multiples Valuation’ is the most often (ab)used mode of Valuation of companies. I will leave links to both and allow you to decide which one suits you the best.

Remember, even after you find out the rough worth of a company, it is advisable that you pay a lot lesser than that to acquire it. Here’s why:

Step 8: Maintain a ‘Not-to-do’ Checklist

“ It’s good to learn from your mistakes. It’s better to learn from other people’s mistakes .”— Warren Buffett .

Even after you’ve performed even single step meticulously, it helps to tick off things in a checklist to make sure you are most definitely not at any sort of fault before pulling the trigger. The list, at its simplest form, should be a collection of all the mistakes ever done in the investing world—ranging from the mistakes you did yourself, to that of your fellow investors, to that of the investing giants around the world.

The list will grow continuously through your investing life, that’s for sure. But be warned that nothing can satisfy 100% of your checklist. Set a nominal limit—like 70%—and proceed from there. Make sure that every single investment decision of yours passes this checklist—whether it’s 60% or 80% is immaterial. The idea is to put a hard stop to impulsive investment decisions.

If you have this framework down to the last detail, you’ve already got a one-up over most of the investing crowd—which is still working off of stock tips and market momentum. But as Benjamin Graham put it, it’s easy to earn more-than-average returns, but very difficult to earn superior returns.

If you attempt to earn big returns, you will fail at first. And that’s okay . Really. Failure is the best teacher and that philosophy is no different in the world of investment. If you want to be an extremely successful investor, you will have to invest and fail—fail again—fail better. All the best.